J. Dale Harvey

Lead Portfolio Manager

Dear Shareholder,

Trust. I’ve been thinking about it a lot lately. My gears started turning in early summer, at a one-hundred-year-old pizzeria in Perugia, Italy. We were seated outside, at a table in a public courtyard that was far from the cash register. Once we’d finished our meal, the waiter didn’t give us a bill; he simply suggested that, whenever we were ready, we go inside to pay. I was struck by the fact that patrons could easily “dine and dash.” And yet: restaurant staff trusted everyone to do the right thing. That same mentality was evident everywhere we went in Perugia and it was refreshing.

Here at home, high-end restaurants often demand a non-refundable deposit because they don’t trust diners to show up for their reservation. Gallup polling suggests that only 10% of the public has a lot of confidence in Congress – barely ahead of Television News at 11%. Sadly, trust in institutions has been eroding for years and that has led to polarization and insularity. Gallup found only 15% confidence in Big Business while Small Business was the most trusted cohort in society (see Appendix for more detail).

This last observation, that the public feels best about small businesses as compared to their bigger competitors, may not be surprising given the U.S.’s entrepreneurial culture. But paradoxically, we don’t see the same sentiment in the stock market, where the biggest companies get much higher valuations as compared to small companies. We continue to be in a two-tier market where the largest companies dominate stock market indices like the S&P 500, where the top ten companies account for more than 38% of the index – you won’t find any of them in our Poplar Forest Partners portfolio.

We know that you trust us to carefully steward your investment funds for your long-term benefit and we take that responsibility seriously. In doing so, we try to avoid areas where potential rewards seem to be outweighed by potential risks. In building truly benchmark-agnostic portfolios of our best ideas, we have avoided the biggest companies because we believe we’ve found plenty of bargains throughout the rest of the 1,000 largest companies in the U.S. At a time when so many investor dollars have been deployed into a concentrated bet on technology, we feel we offer a compelling alternative that may also offer downside protection if something were to disrupt investors’ current love affair with all things AI.

Equity Investing – Trust Matters

Equity investing is inherently uncertain. The value of any given stock ultimately depends on the future cash flows that its underlying business generates. Predicting those cash flows, however, is much harder than cooking a pizza. Valuation measures, like the Price-to-Earnings (or PE) ratio, are one way of expressing how much confidence investors have in the future. If investors trust that future earnings growth will be high, then they assign a higher valuation to stocks. Likewise, if the future seems bleak, the PE ratio may be low.

Given the many measurable aspects of investing, it can at times feel akin to a hard science like physics – complete with ratios, moving averages, exponential equations, and highly precise quantitative models. In my experience, investing is more of a social science. Understanding investor psychology may be more important than the math behind forecasting free cash flows.

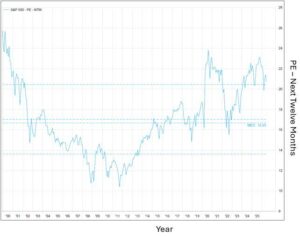

As you can see on the chart below, in late 1999/early 2000, investors were overwhelmingly bullish. The new century was going to be better than ever, powered by the emerging promise of the internet. This blind faith in the future resulted in the S&P 500 being valued at more than 25x year-ahead earnings. In contrast, by 2008, the internet wasn’t the topic du jour anymore, it was the collapse of the housing market and the toxic loans that had supported it. Financial institutions were failing and the government had to bail them out.

As faith in the future devolved into distrust of banks, valuations collapsed and those who owned the S&P 500 suffered losses of nearly 4% per year over the nine years from the end of 1999 to the end of 2008. Conversely, for those contrarians willing to buy in 2008 when the crowd was selling, the next nine years produced gains of more than 15% a year. Seeing countless examples of this same type of behavior at the individual company level — excessive optimism leading to losses and excessive pessimism setting up attractive gains — solidified my commitment to the contrarian value philosophy I have long pursued.

Trust in the Fed – There’s a New Chef Manning the Pizza Oven

Over the last couple of years, stock valuations have returned to levels that signal great trust in the future driven by a belief that artificial intelligence can be a great productivity enhancer for society. I tend to believe this will be true, but even as the internet changed our lives for the better, many of the companies that delivered that change faced massive stock price declines in 2000-2003 as ebullient expectations gave way to the realities of the marketplace.

Investors also currently believe that the so called “Fed Put” will stay in place. The idea is that government will again save the day if anything goes wrong as was the case in the ’08-’09 Financial Crisis and the more recent COVID Crash. With growing public distrust of Congress and the White House, and with Federal budget deficits and outstanding debt at seemingly unsustainably high levels, investors appear to have placed all their trust in the U.S. Federal Reserve (the “Fed”). I suspect this belief will get tested in coming months and years now that the Fed has a new Chairman.

Over the last 20 years, the Fed has always stepped in to support markets during times of crisis by lowering interest rates and/or buying bonds to provide liquidity support for the economy. When the Fed is viewed as the buyer of last resort, there is a feeling that investing outcomes will never be that bad. This can create a problem referred to as moral hazard when risk and reward aren’t symmetrical. Think of it as getting all the pizza if everything goes right, with someone else paying the bill if something goes wrong.

I am a big fan of new Fed Chairman Warsh, not because I believe that he will seek to drastically cut interest rates, as President Trump wants, but because his past statements suggest that he plans to tackle moral hazard head on:

“A permanently large balance sheet… can distort asset prices and weaken market discipline. It entrenches financial dependence on central-bank liquidity.”

“Moral hazard in the financial system is higher than any of us should countenance… Market discipline only works if governments can demonstrably and credibly commit to allow firms to fail.”

The adage that the market “tests” a new Federal Reserve Chair is a favorite among financial historians and value investors alike. Looking at the last five Chairs, there is indeed a recurring pattern of significant volatility (or “baptism by fire”) events occurring within their first year. The biggest of these were the 1987 stock market crash that occurred two months into Alan Greenspan’s tenure and a 19.8% decline in the S&P 500 early in Jay Powell’s term.

I doubt we will see a bear market in the near future, but Wall Street will be closely watching to see how the new Fed Chair responds to whatever market disruption comes his way. Perhaps the massive data center buildout that is driving the economy today will prove disappointing, or perhaps that growth will be so strong that it produces stubbornly high inflation. The market has cheered the purported end of hostilities in the Middle East, but what if this seemingly fragile truce fails to hold?

Say/Do Ratio

“Trust is like the air we breathe — when it’s present, nobody really notices. When it’s absent, everybody notices.” — Warren Buffett

In my experience, trust isn’t given, it is earned over time. And one of the best ways of earning trust is to do what you say you are going to do. Some call this the Say/Do Ratio. If we are to take Chairman Warsh at his word, then downside risks may increase in the short term as the Fed more seriously approaches its mandate for price stability while also bringing more symmetry back into financial markets (in short, the “Fed Put” may expire worthless). I think these potential short-term costs are well worth strengthening the underlying foundation of the Federal Reserve and I’m very pleased to see how Chairman Warsh is approaching his job so far.

We apply the ‘Say/Do Ratio’ directly to the management teams of the companies we consider for investment. When a stock is out of favor, Wall Street is highly skeptical. My colleagues and I try to look past the headlines and evaluate management’s historical track record: Do they hit their stated operational targets? Do they protect the balance sheet? Do they take a conservative approach when talking about the future or are they highly promotional? When a management team has a favorable Say/Do Ratio, it gives us the trust required to buy their stock when the rest of the market is selling.

One person who has seemed to be rewarded for saying outrageous things while not always delivering is Elon Musk – the world’s first trillionaire. While Tesla and SpaceX have certainly achieved great things and proved countless doubters wrong, I remain amazed with how much trust investors have placed in someone who dreams so audaciously. SpaceX isn’t profitable and it is burning massive amounts of cash as it pursues Elon’s dreams of datacenters in space and ultimately colonizing Mars. Investors are willing to pay more than 100x revenues in hopes that all these visions materialize. If you ask me, price matters and at its current valuation, the odds of SpaceX producing outstanding results for its shareholders don’t seem to be tilted in investors’ favor. We prefer a slice of pizza in the hand to two on Mars and while we may miss out on big gains if everything Musk imagines comes true, speculating on bleeding edge technology isn’t the type of endeavor we pursue.

As contrarian value investors, we prefer businesses that are currently generating growing streams of free cash flow. We focus on identifying companies where expectations for the future are unduly low. While none of our companies will colonize Mars, we believe that they can grow earnings in line with the broad market while paying us above average dividends. At a time when the S&P 500 is valued at more than 20x earnings, our companies trade for less than 13x. We think that is a recipe for success.

Since starting Poplar Forest back in 2007, I have said that we will build our benchmark-agnostic portfolios from the bottom up with a focus on normalized earnings and free cash flow. By sticking to a repeatable process, we have said that we believe that our contrarian value strategy will do particularly well when value stocks beat growth stocks. And that is exactly what we’ve seen so far this year. Through June 30, the Russell 1000 Growth Index has produced about a 4% total return while the Value Index has gained close to 16% — Value has beaten Growth and we’ve beaten both. While AI and Space companies may continue to get all the headlines, I believe our portfolio of carefully selected Value stocks will continue to quietly deliver market-beating results.

Back in Perugia, my wife and I got up – full to bursting with incredible pizza – and went inside to pay our bill. In this analogy, you – our clients – are the equivalent of the pizza parlor owner, who trusted us to do the right thing. We recognize the trust that all of you have placed in us. We strive to steward your money in a way that generates market-beating long-term returns. As fiduciaries, we work in a manner intended to earn your continued trust, and we plan to do our best on your behalf for many more years to come.

J. Dale Harvey

June 30, 2026

Click here for Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.