J. Dale Harvey

Lead Portfolio Manager

Dear Partners,

The first nine months of the year were very rewarding for our team. The benefits of joining Tocqueville have exceeded expectations and we love working with our new colleagues. The stock market has been strong and our investment results have exceeded the performance of all relevant benchmarks. What’s more, the future looks bright: our portfolio is currently valued at less than 15x earnings with prospects for 15% annual earnings growth over the next few years. I believe that our selective, bottom-up, value-based, fundamentals-driven investment process is particularly well suited for the current investment environment in which heady stock market gains may be signaling widespread investor complacency.

Investor sentiment is a bit like a pendulum slowly swinging from a focus on potential rewards to one concerned with perceived risk. As stewards of your money, we try to stay balanced amid the swings. When evaluating investments, we don’t just ask, “What could go right?” but also, “What can go wrong?” I believe that the relatively low expectations the market has embedded in the stocks we own provide handsome compensation for the risks our companies face. It’s quite a different picture when I look at investing markets more broadly. For many of the largest companies that dominate the stock indices, and the headlines on the financial pages, the pendulum seems to have swung to a rather extreme focus on reward with little concern for risk. It seems as though investors are only imagining what could go right while ignoring what could go wrong. The image that keeps coming to mind is that of Mad Magazine’s mascot Alfred E. Neuman and his famous tag line: “What, me worry?”

I see worrisome signs of investor complacency and speculation in crypto trading, meme stocks and AI enthusiasm; in historically low spreads on corporate bonds as compared to Treasury securities; and in the lofty valuations of most stock indices. The S&P 500 is trading at all time high levels despite strained international relations, challenges to the independence of the Federal Reserve, a macroeconomic headwind from tariffs, and the impact on labor markets from the deportation of undocumented workers. The job market has weakened, but earnings growth has been solid and investors are counting on profligate government spending, reduced regulatory burdens, and falling interest rates to keep the party going. What, me worry?

There is precedent for this optimistic outlook. Historically, when interest rate reductions aren’t in response to recession but are more of a normalization of monetary policy, the stock market has often produced higher-than-average returns. That has certainly been the case over the last year. In 2022 and 2023, the Federal Reserve raised interest rates to “Restrictive” levels in hopes of slowing the economy to combat inflation. Then, beginning in September 2024, the Federal Reserve started cutting short-term interest rates to more “Neutral” levels. The S&P 500 responded to falling short-term rates with a gain of more than 15%. As long as the Fed is cutting rates, and provided we avoid recession, investors are apt to stay bullish.

As contrarians, we tend to worry when others don’t. And, importantly for you: we do the worrying so you don’t have to. We will continue to stick to our absolute value discipline and work from the bottom up to identify companies whose prospects may be underappreciated by other investors — where the rewards from what may go right far outweigh the downside if things go wrong. We will continue to focus on normalized free cash flow as we believe that is what drives long-term investment value. In a two-tier market in which the market-cap weighted stock indices appear very richly valued, we continue to find bargains in companies that may not be household names.

At more than 24x earnings, the S&P 500 is currently trading at 33% premium to its valuation over the last 25 years. Valuation won’t be a problem, provided that earnings grow at an above average rate, but there is little room for error if growth slows. Still, there are hundreds of stocks trading at more reasonable valuations that reflect a more balanced view of the future. I have long subscribed to the Value Line investment service, and I’ve dutifully recorded the weekly P/E ratio for their universe of 1700 stocks since January 1999. Value Line’s P/E isn’t “cheap” at a little more than 18x, but at a mere 7% premium to history, it doesn’t look particularly expensive either. With hundreds of stocks trading at mid-teens multiples, we at Tocqueville’s Poplar Forest Team have had plenty of opportunities to choose from.

Bargain Hunting in Healthcare

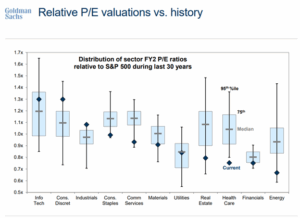

Healthcare has been an area of investment focus for us this year. A new investment in Humana in the first quarter plus gains in Cencora, CVS and United Therapeutics has pushed our healthcare exposure to more than 20% of our portfolio as compared to 14% at the beginning of the year. Healthcare is our now largest exposure. While the industry historically enjoyed a premium P/E ratio, investors have applied discounted valuations given the pressure from reduced Medicaid spending, falling NIH funding, and Health and Human Services head Robert F. Kennedy Jr.’s more combative stance. As you can see in the graph below, healthcare stocks are as cheap as they’ve been in at least 30 years.

At the end of the day, we believe that people will continue to get sick and that they will seek treatment for their ailments. A growing population of uninsured patients may create headwinds for the providers of healthcare services if bills go unpaid, but we have no direct exposure to the hospital business. What has historically been a recession-resistant sector is now trading at discounted valuations. As contrarians, we tend to lean into controversy like this when we can find companies with idiosyncratic characteristics that can help them navigate the noise.

We did just that in the third quarter by making a new investment in Alexandria Real Estate. Alexandria established the industry of building (or buying) and then leasing out specialized real estate for the life science sector. It is the largest and most well-established player in the field and the developer of a “megacampus” model in key healthcare research areas including Boston, the San Francisco Bay Area, and San Diego. This expertise provides a competitive advantage, as life science companies require highly specialized lab and office spaces. The leading companies want the best campuses to attract talent and that is what Alexandria offers.

With cuts to Federal support of life sciences and a dearth of new private funding and biotech IPOs, investors have grown concerned about potential excess real estate capacity in this space — too many new buildings chasing too few new tenants. After peaking at more than $200 a share in late 2021, Alexandria’s stock fell more than 65% — a level that we believed offered tremendous value. The company has a very stable tenant base and only about 7-8% of their leases come up for renewal each year. This provides consistent cash flows which are used to pay dividends to the company’s shareholders. The stock currently offers a better than 6% dividend yield as compared to an historical median of less than 3%. Over time, the company’s dividend payments have grown at a rate of 4-5% per year, and we expect that pace to resume after a brief pause this year. If market turbulence should pick up in the future, we believe this defensive business serving an out-of-favor sector may hold up well.

What, Me Worry?

As I mentioned at the top of this letter, our focus on risk-adjusted returns has helped us identify a portfolio of companies with both compelling earnings growth opportunities and heavily discounted valuations. In addition to trading at just 14x earnings for companies Wall Street expects to grow 15% a year; our companies are generating free cash flow equal to 4.8% of their market value (“free cash yield”) at a time when 10-year Treasury bonds yield barely more than 4%. We expect our companies to grow their free cash flow in line with earnings. With that as a starting point, we feel great about what we own, but we are always on the lookout for new investments that can further improve the portfolio’s risk/reward ratio. Just as we ask what might go wrong with an individual investment, we also ask ourselves what might go wrong at the macroeconomic level. Fewer and fewer investors seem to be worried about risks that seem very real to me.

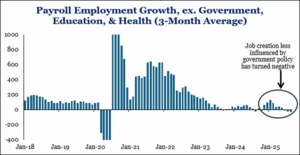

First among my list of worries is the employment outlook. As I stated at the beginning of this letter, the market may keep powering ahead provided the U.S. economy stays out of recession. We continue to watch carefully for signs that indicate rising recession potential. Foremost among those indicators are declines in job creation and layoff announcements. Job growth has slowed over the last six months, and new unemployment claims have started to increase. I’m not saying that a recession is right around the corner, but at a time when many investors seem optimistic about the outlook, we see more value in less economically sensitive businesses.

We aren’t alone in worrying about the job market. As Federal Reserve chair Jerome Powell put it in August, “The balance of risks appears to be shifting.” He added that the current “unusual situation suggests that downside risks to employment are rising. And if those risks materialize, they can do so quickly in the form of sharply higher layoffs and rising unemployment.”

This all argues for additional reductions in interest rates in the coming months and that’s what investors are counting on, but one challenge for the Fed is that inflation, at roughly 3%, has stayed stubbornly above the Fed’s own 2% inflation target. And with tariff-driven price increases now starting to hit store shelves, inflation readings may continue to trend higher. A falling U.S. dollar doesn’t help. Investors appear to expect another five cuts to short-term interest rates between now and the end of 2026; if stubborn inflation readings prevent the Fed from cutting rates as aggressively as investors expect, stocks may give back some of their recent gains.

I also worry that both things can be true – what if there are job losses AND persistent inflation? This “stagflation” risk may be higher than people think.

The interest rate outlook is also complicated by growing government debt balances. With the Federal budget projected to produce deficits equal to 6% of GDP annually for the next decade, debt relative to the size of the economy should be expected to grow. This problem could be even worse if the Supreme Court affirms recent lower court rulings that many of the President’s tariff actions are illegal. That could result in the U.S. Treasury having to return hundreds of billions of dollars of tariff collections. As debt grows relative to the size of the U.S. economy, long-term interest rates — critical for the buyers of homes and cars –may increase, as bond buyers demand a growing premium for growing risks. We’ve seen this happen in the U.K., France, and Japan this year and are mindful of something similar happening in U.S.

We Worry So You Don’t Have To

As stewards of your investments, you pay us to not just grow your wealth over time, but to also help minimize the impact of the potholes that occasionally appear in the road ahead. While continued gains are the most likely path forward for the market, risks are starting to grow and we are taking actions to help defend against them. We continue to invest side by side with you and continue, as always, to put our money where our mouth is.

The companies in which we are invested are financially strong and generate healthy free cash flows which can be used to improve their respective competitive positions in times of economic stress. At a time when many stocks look expensive, our portfolio is trading at a 25% discount to our assessment of fair value. If the future develops as we expect, we may ultimately see investors sell their highfliers to buy the type of value stocks we favor. The leading growth companies are certainly delivering superior revenue and earnings growth, but they are also investing hundreds of billions of dollars to build data centers to support their artificial intelligence models. The companies involved may be hard pressed to deliver the revenues needed to justify their spending and if they disappoint, the downside could be material. That is exactly what happened 25 years ago when investors were last enamored with new technology – then it was the Internet, today it is AI.

As we all know, the Internet was a momentous development, and I believe that Artificial Intelligence will be as well. Still, while the Internet changed so many things, many of the stocks related to it — remember America Online (AOL)? — didn’t live up to the hype. From 2000-2006, Value stocks handily beat Growth stocks as inflated expectations for the late-‘90s market darlings proved excessive relative to the reality that ultimately prevailed. They say that history never repeats, but that it often rhymes. If that’s the case, the Poplar Forest Team and our clients may be very well positioned for what may come our way.

Thank you for your continued trust and confidence,

J. Dale Harvey

June 30, 2025

Click here for Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.