")

I’ve been a music nut since I was in middle school. As soon as my savings allowed, I bought a stereo system that provided hours of listening pleasure all through high school and college. By graduation, L.P.s were giving way to compact discs. Then came MP3s and streaming. I’ve been a Spotify devotee for more than a decade and I find it is simply amazing that my phone can access over 100 million songs virtually anywhere, anytime.

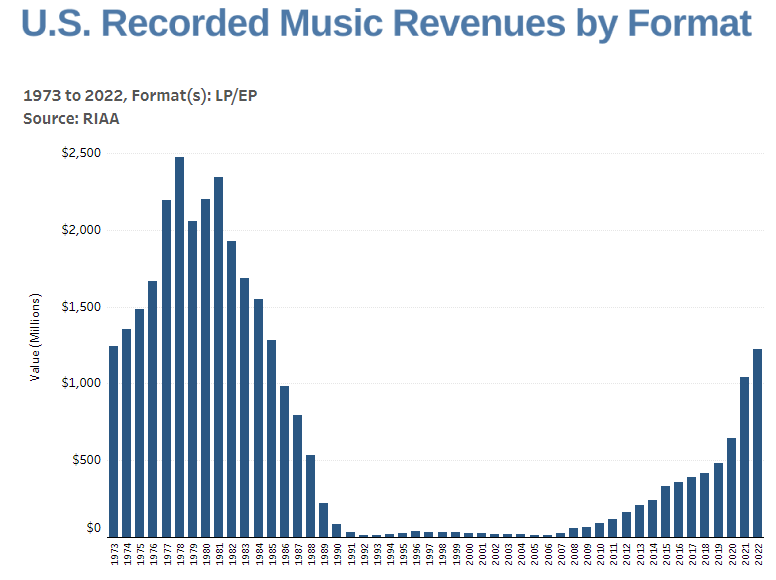

As mind-boggling as Spotify is, I found myself missing the sound quality and physical interaction with my carefully curated album collection. I still had more than a hundred of my beloved LPs – from The Clash, to B.B. King, Tom Petty, Stevie Ray Vaughn, and so many more – in a crate in the closet, but nothing to play them on. So I sprung for a new turntable and speakers, and started buying vinyl again. I’m not alone. As you can see below, after almost disappearing in the 1990s, album sales are on the rise again. What to make of this resurgence of old, analog technology in our increasingly digital world? I think it is more than sound quality and appreciating the cover art and liner notes. Listening to an album also reveals its “deep cuts” — tracks you might not discover on a hit-driven streaming service.

One album for which I’ve recently gained a new appreciation is Brothers and Sisters, which was released in 1973 by The Allman Brothers Band. As a teen, I didn’t have enough life experience to appreciate the lyrics, keyboard solos, and blues riffs the band laid down, but today, at 58, I find that the music speaks to me. While this record includes one of the band’s biggest hits, “Ramblin’ Man,” I’m particularly drawn to three lesser-known tunes: “Pony Boy,” “Jelly Jelly,” and “Southbound.” These songs have existed for fifty years, but I suspect few people know them well – like I didn’t until I looked past the hits and dug a little deeper.

When picking stocks for Poplar Forest’s portfolio, my colleagues and I do much the same thing. While we pursue Value stocks of all sizes, of course, we often find particularly compelling opportunities in the investment world’s equivalent of the music industry’s deep cuts: out-of-favor, unappreciated, or undiscovered medium-sized companies, or “Midcaps.” My thinking about Midcaps is that because fewer people are paying attention to them, there may be more opportunity to uncover values that others don’t see. In addition, Midcap companies may have scale advantages over their smaller competitors and more growth potential than their largest competitors.

In recent years, investors overall have been enthralled by the performance of the biggest companies while they’ve increasingly ignored just about everything else. It hasn’t always been this way; historically, the stocks that you may not have heard about are often the ones that may get your portfolio grooving.

“Band is jumping and so am I

I’m just groovin’, can’t stop moving…

When morning comes and it’s time to go

Pony Boy, carry me home.”

From “Pony Boy”

I have long believed that having the flexibility to invest in Midcaps was critical to long-term investment success. In my Capital Group days, when I was managing portfolios with $20 billion of assets, I realized that I had lost that flexibility and that realization was part of the reason I started Poplar Forest in 2007. Early in my career, before the market was sliced and diced the way it is now, the importance of Midcaps was harder to prove, but now, more than 25 years later, we have the data.

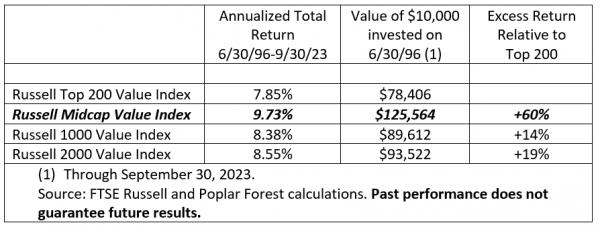

Well-known index provider FTSE Russell splits the U.S market into two groups: the largest thousand companies (the “Large Cap” Index) and the next 2,000 (the “Small Cap” Index). The largest thousand are further segregated into the Top 200 (generally at least $40 billion market cap) and Midcaps (the next 800). As you can see below, from June 30, 1996, when I first became a diversified portfolio manager, through Sept. 30, 2023, Midcap Value stocks have beaten their larger peers by almost 2% a year and Small Cap Value stocks by more than 1% per year. While 1-2% a year may not sound like much, over 25 years, it makes a huge difference. History suggests that Midcaps make more money in the long-term, and Poplar Forest was specifically designed to take advantage of this potential for outperformance.

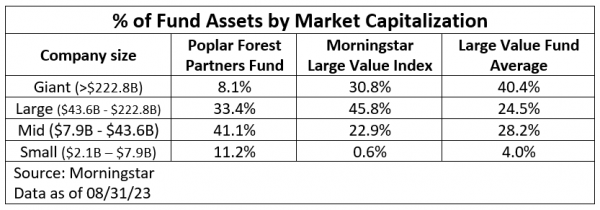

Poplar Forest owns stock in plenty of big companies, like Merck, Intel, Chevron and Wells Fargo, but the size of our portfolios doesn’t limit us to investing in only the biggest. When you compare the market cap distribution of our portfolio to the stocks owned by other Value managers, you can see that we offer a differentiated Value strategy with above average exposure to what has historically been a sweet spot in markets. In market environments in which investors favor the biggest companies, our exposure to midcap companies may be a hindrance, but over time, we believe that our investment flexibility will prove to be advantageous. Much like Allman Brothers guitarist Dickey Betts sings in the chorus to “Pony Boy,” the final song on the Brothers and Sisters album, I believe that Midcaps will help carry us home.

So far this year, we’ve made five new investments – almost all Midcaps: Tyson Foods ($20 billion market cap) in the first quarter, Oshkosh ($6 billion) in the second, and three new investments in the most recent quarter. Of the three newest stocks, two are economically-sensitive companies ($5-7 billion each) that we believe are under-earning and whose P/E multiples are depressed because of investors’ fear of recession. Both businesses consistently generate free cash flow and offer, in our assessment, above average earnings growth potential over the next few years, yet they are both valued at just 9x Wall Street’s best guess for 2024 earnings. The third new investment is a nearly $40 billion market cap, historically recession-resistant business with an above average dividend yield, a strong balance sheet and a valuation of slightly more than 13x expected 2024 earnings. In short, we have invested in: two cyclical stocks that we believe offer attractive upside potential with limited downside in a recession given their valuations; and one defensive business with limited earnings risk in a recession and a well-covered dividend that produces a substantial yield premium relative to the company’s peers.

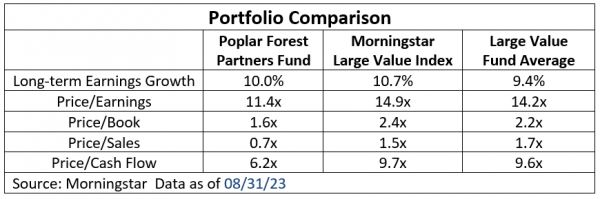

Having the market cap flexibility to pursue bargains in any of the thousand largest companies in the U.S. has allowed us to build a portfolio that we believe offers very compelling value on both an absolute basis and relative to other Large Value funds. As you can see below, based on Morningstar’s assessment, our portfolio companies offer comparable long-term earnings growth at a close to 25% P/E discount as compared to other Large Value portfolios

“You’re my blue sky, you’re my sunny day

Lord you know it makes me high

When you turn your love my way.”

From “Blue Sky” on the Allman’s 1972 Album Eat a Peach

For the last 18 months, investors have understandably been living with fears of recession as the Fed set about normalizing monetary policy after COVID. Short-term interest rates have increased from near zero to more than 5.25% and the yield on 10-year Treasury bonds almost tripled from around 1.5% to more than 4.25%. History suggests that such a dramatic tightening of monetary policy will cause a recession, but so far, investors mostly see blue skies. Monthly payments for new home and auto loans have soared due to higher prices and higher interest rates and historically, that leads to a weakening economy. Yet employment is still strong and consumer spending has remained resilient while inflation has moderated.

The emerging opinion is that inflation has been defeated without a recession, and as a result, the Fed can soon stop raising interest rates. Economic resilience has allowed companies to maintain margins and corporate earnings estimates have been trending higher in recent months. Stocks, as measured by the S&P 500, have been quite strong this year, though that strength has been concentrated in the biggest growth companies.

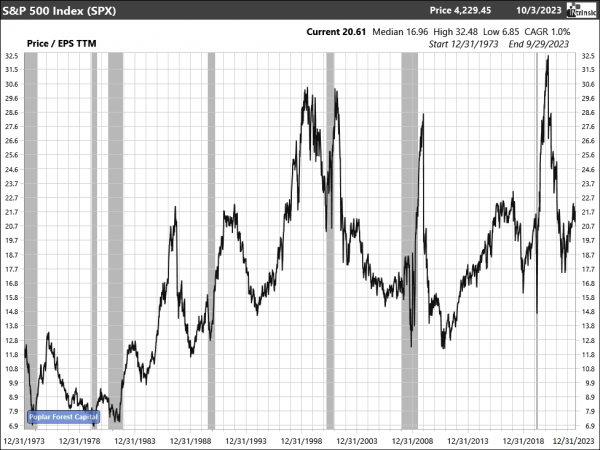

P/E ratios can be a helpful tool for judging investors’ attitudes. When the outlook is optimistic, buyers are willing to assign a high multiple for stocks, while pessimism is reflected in low multiples. As you can see in the chart below, outside of recessionary periods when earnings are depressed, the price/earnings ratio of the S&P 500 has rarely exceeded 21-22x trailing earnings – the S&P is currently valued at 22.2x.

Source: Intrinsic Research. TTM = trailing 12 months

In the half-century since the release of Brothers and Sisters, the only non-recessionary period in which investors were more optimistic, as reflected in P/E ratios, was during the late-1990s Tech Bubble – and we know how badly that ended. High valuations, in and of themselves, don’t mean that stocks can’t keep moving higher if earnings grow, but they may help gauge downside potential. With current valuations — and implied investor expectations — about as high as they get, the S&P 500 would appear to offer a mediocre tradeoff between risk and reward. In contrast, the low valuation of Poplar Forest Partners portfolio suggests a much more attractive risk/reward ratio.

The companies in our portfolio are currently being valued at roughly 10x Wall Street’s best guess for earnings in 2024 – a valuation that offers very attractive upside should a recession be avoided. Our risk-adjusted fair value analysis for the companies we own suggests they deserve to be valued at 14.5-15.0x 2024 earnings – a 45-50% premium to their current valuation. With the S&P 500 currently valued at roughly 19x expected 2024 earnings, our companies look like particularly good value.

“Oh, it’s stormin’, stormin’ rain and I’m as lonesome as a man can be…

it’s a down-right rotten, low down dirty shame, the way that you treated me.”

From “Jelly Jelly”

At a time when other investors are focused on blue economic skies, we think it is prudent to plan more conservatively. To help us avoid the “Jelly Jelly” blues at Poplar Forest, our financial forecasts continue to assume a recession will hit sometime in the next 12 months. I sincerely hope that assumption is too conservative, but given restrictive monetary policy and exuberant investor attitudes, it seems especially prudent right now to emphasize risk management in our portfolio management decisions. Monetary policy is purported to work with long and variable lags, and history suggests that it could start storming soon.

In a recession, we believe that our companies’ earnings may get hit by about 20%. If that is correct, then our portfolio would be valued at just 12.5x – still a very low multiple in an absolute sense, and even more so considering those would be depressed earnings. The upside potential weighted against what appears to be limited recessionary downside is one of the best risk/reward ratios I can remember.

“I got that old lonesome feelin’ that’s sometimes called the blues

Well I been workin’ every night, travelin’ every day…

You can tell your other man, sweet daddy’s on his way…

Well I’m going to make it on up to you

For all the things you should have had before.”

from Southbound

When I first started Poplar Forest, album sales were just starting to emerge from a 16-year drought in sales. I realize that collecting, storing, and listening to records isn’t as easy as streaming digital music, but I find it to be more than worth the trouble. As I’ve said, the sound is richer and there is something viscerally satisfying about pulling a treasured album out of its sleeve, placing it on the platter and dropping the needle. In a way, it’s almost like I can “touch” the music when playing an LP – something that doesn’t happen when I stream a digital recording.

In the same way that an album can be a physical manifestation of music, “free cash flow” – the amount of money left over after a company has paid its bills and invested for future growth – may be a similar expression of business success. When the free cash flow that our companies produce is divided by the value of those companies, the result is what we call the “free cash yield.” Based on results over the last 12 months, our portfolio is valued at a 6.4% free cash yield (a substantial premium to the S&P 500’s 4.0% free cash yield) and we see prospects for double-digit annual growth in those cash flows in the next three to five years. While the short-term may be volatile as bulls and bears debate the likelihood of recession, our portfolio’s combination of free cash yield and growth point to substantial long-term appreciation potential.

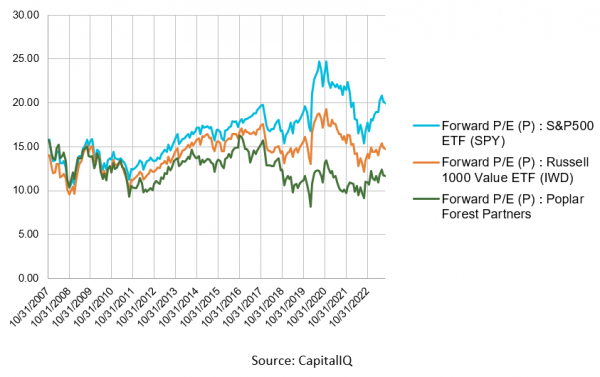

As you can see below, in late 2007 when we started Poplar Forest, and after a multi-year run starting in 2000 that saw the Russell 1000 Value Index beat the S&P by a cumulative 50%, there was not much value left in Value stocks, at least as compared to the S&P 500. Today, the tables have turned and our opportunity set is about as robust as I can remember it. Interest rates are roughly back to where they were in 2007 while the P/E ratio for the S&P 500 is roughly 25% higher; yet, we’ve been able to assemble a portfolio that has a 25% lower valuation as compared to the companies we owned back then.

I started Poplar Forest with the goal of providing like-minded clients with market beating long-term investment results through a high conviction, disciplined, absolute value investment strategy. Then, as now, I was focused on finding out-of-favor and underappreciated stocks with idiosyncratic return characteristics and I believe we’ve done a good job of that. However, the decade-long compression in Value stocks’ relative valuations has certainly been an unexpected headwind to our results. That said, those headwinds have created an environment that in our view positions Value investing for a renaissance similar to that experienced by album sales over the last decade.

We remain committed to an investment process that seeks to uncover what we believe are bargains with above average long-term potential and below average risk. In a market environment in which investors are enamored with the leading Growth stocks, it might be easy for us to get those old lonesome blues were it not for the support of a fantastic group of client partners on whose behalf we work each day. I don’t know when the current Growth stock infatuation will end, but when it does, I believe that our portfolio has the potential to produce chart-topping results – to quote Gregg Allman in “Southbound”: “Sweet Daddy’s on his way!”

Sincerely,

September 30, 2023

Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.