Questions of Value — Are investors being compensated for the risk of a weakening U.S. consumer?

Questions of Value is a series of memos addressing common questions from our clients about the Partners Fund and Value investing. We welcome your feedback!

As we head into the holiday shopping season, the health of the U.S. consumer is top of mind. The debate among most market observers isn’t whether consumer spending will weaken in 2024 but by what magnitude. Since we can’t consistently predict macroeconomic trends like consumer spending our approach to thinking through these economic questions involves stress-testing our investments against a diverse set of future economic scenarios. In so doing, we are able to better define each investment’s risk and reward potential and develop some insight into which economic scenario a company’s stock price and valuation reflect. Our analysis suggests that most stocks are being valued under the assumption that growth in consumer spending will slow a little in 2024 and then reaccelerate in 2025 and beyond. This scenario is commonly referred to as a “soft landing” from above-average growth trends during the last few years. As we evaluate businesses, we are drawn to companies whose stock prices reflect a more cautious outlook for the economy in order to ensure an adequate margin of safety. While we hope the economy positively surprises relative to our expectations, we are currently employing conservative assumptions in our investment analysis. In this memo, we discuss how our search for a margin of safety has led to a shift away from companies with high sensitivity to negative surprises in consumer spending and towards companies selling less discretionary products or services.

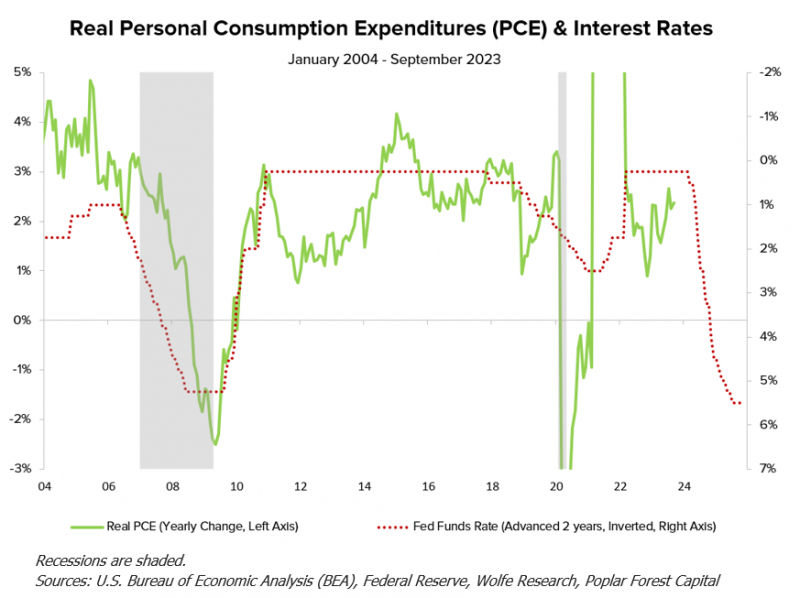

U.S. economic history indicates that rising interest rates tend to restrict corporate and consumer spending while falling interest rates can have the opposite effect. Over the last 20 years, trends in interest rates have impacted consumer spending with a lag of 18-24 months. While the lags between rising or falling interest rates and consumer spending can vary over time, an inverse relationship between these two variables makes sense. If this relationship holds true in the future, then the increase in the Fed Funds rate from 0.25% in March 2022 to 5.50% in September 2023 will start to negatively impact consumer spending sometime in 2024. This point can be visualized in the chart below where we have advanced the Fed Funds rate by 24 months (red dotted line, inverted) and plotted it against the annual change in real personal consumer spending (green line), a monthly government measure of consumer spending. The historical relationship between interest rates and consumer spending is one reason why we believe, in the interest of conservatism, it is prudent to assume a consumer slowdown in 2024 when evaluating the risk and reward profiles of our investments.

The Consumer and Financial Services sectors of the economy are often particularly sensitive to trends in consumer spending and financial health. For many consumer businesses selling discretionary products or services, like clothing and cruises, there can be an immediate decline in sales when consumers start to experience financial stress. Financial services businesses that lend money to consumers can also see their earnings and stock prices take a hit if job losses or financial pressures cause consumers to default on loan payments. With these points in mind, our portfolios’ exposure to the Consumer Discretionary sector is near the low end of our historical range. Conversely, our investments in the less economically sensitive Consumer Staples sector are near the high end of historical levels. Within the Financial Services sector, our overall weighting is in-line with historical averages. The mix of our Financial Services investments, however, has shifted towards companies selling non-discretionary products and services, such as insurance and banking software, and away from more credit-sensitive product lines, like consumer credit cards and loans. While the list is short, we continue to find a select few Consumer Discretionary and credit-sensitive Financial Services investments where the stock prices already embed a meaningful deterioration in business trends in 2024. For these companies, the management teams are already planning for a weaker 2024 while also executing on company specific self-help initiatives to increase long-term earnings power. Over the long run, we believe each of these companies offers highly attractive return potential and, if a recessionary slowdown in consumer spending is avoided, those returns are likely to be front-end loaded.

Our Financial Services and Consumer investments span a diverse set of business models with varying sensitivities to consumer spending and consumer balance sheets. We also have a well-developed shopping list of companies in these end markets that we’d be quick to own whenever valuations reflect an adequate margin of safety. Our ability to be highly selective with our investments means we can limit our investments to only those pursuing idiosyncratic self-help strategies that can improve long-term earnings power, irrespective of the near-term economic environment.

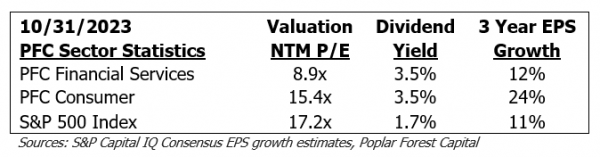

As the table below highlights, compared to the S&P 500 Index (a proxy for the broader stock market), our Financial Services and Consumer investments are trading at significantly lower valuations while offering better dividend yields and comparable-to-better earnings per share (EPS) growth potential. If the consensus EPS growth estimates for our companies are roughly right, then the combination of earnings growth and dividend yields suggests double-digit fundamental returns for this part of our portfolio. Regardless of whether there is a mild recession or a soft landing, we believe the multi-year outlook for our Financial Services and Consumer investments is bright.

DISCLOSURES

The Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. The summary and statutory prospectuses contain this and other important information and can be obtained by calling 1-877-522-8860 or by visiting www.poplarforestfunds.com .Read it carefully before investing.

Partners fund investing involves risk. Principal loss is possible. The funds may invest in debt securities which typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. The funds may invest in foreign securities which involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks are greater in emerging markets. Investing in small and medium sized companies may involve greater risk than investing in larger, more established companies because small and medium capitalization companies can be subject to greater share price volatility. The funds may invest in options, which may be subject to greater fluctuations in value than an investment in the underlying securities. When the Cornerstone Fund invests in other funds and ETFs an investor will indirectly bear the principal risks and its share of the fees and expenses of the underlying funds. Investments in asset-backed and mortgage-backed securities involve additional risks such as credit risk, prepayment risk, possible illiquidity and default, and increased susceptibility to adverse economic developments. Diversification does not assure a profit, nor does it protect against a loss in a declining market.

Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Fund holdings and sector allocations are subject to change and should not be considered recommendations to buy or sell any security. Past performance does not guarantee future results. Index performance is not indictive of fund performance. To obtain fund performance, visit www.poplarforestfunds.com or call 1-877-522-8860.

Earnings growth is not a measure of the Fund’s future performance.

Basis points (BPS): A unit of measurement that denotes a change in the interest rate of a financial instrument and is equal to 1/100th of 1%.

Dividend Yield: Represents the trailing 12-month dividend yield aggregating all income distributions per share over the past year, divided by the period ending fund or stock share price. It does not reflect capital gains distributions.

Earnings Growth: The annual rate of growth of earnings typically measured as Earnings Per Share Growth.

Earnings Per Share (EPS): The net income of a company divided by the total number of shares it has outstanding.

Forward P/E: A version of the ratio of price-to-earnings (P/E) that uses forecasted earnings for the P/E calculation.

Inflation: Is a quantitative measure of the rate at which the average price level of a basket of selected goods and services in an economy increases over a period of time. Often expressed as a percentage, inflation indicates a decrease in the purchasing power of a nation’s currency.

Next Twelve Months (NTM): The selected metric is based on the project’s performance in the coming twelve months.

Price/Earnings (P/E) Ratio: Is a common tool for comparing the prices of different common stocks and is calculated by dividing the earnings per share into the current market price of a stock.

S&P 500 Index: Is a market value weighted index consisting of 500 stocks chosen for market size, liquidity and industry group representation. The Index is unmanaged, and one cannot invest directly in the Index.

Yield Curve: Is a line that compares the yield of bonds of equal quality but different maturity dates. In general, bonds with longer maturity dates offer higher yields than bonds with shorter maturity dates, thus producing an upward sloping yield curve.

Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.