Questions of Value — Do expectations for employment, interest rates, and the stock market add up?

Questions of Value is a series of memos addressing common questions from our clients about the Partners Fund and Value investing. We welcome your feedback!

Differences of opinion are what make a market and recent commentary from investors, corporate management teams, and the Federal Reserve would, on the surface, suggest a wide range of views exist around the outlook for the economy and stock market over the next 12-18 months. With two-thirds of economists polled by Bloomberg now expecting a recession in the next 12 months, talk of an imminent slowdown in the economy is increasingly common among investors and business executives[1]. It is open to debate, however, whether these concerns are being acted upon by market participants since the S&P 500 Index is up over 8% through April and valued at an above average valuation multiple of 19x consensus earnings estimates for 2023. While first quarter data in 2023 would suggest economic growth is slowing relative to 2022, persistent wage inflation and unemployment rates near historical lows suggests that the rhetoric around a slowdown in 2023 may quickly need to become a reality if the Federal Reserve is going to achieve its 2% inflation target. In this memo, we explore some of the conflicting narratives around trends in employment, interest rates, and the stock market and address potential implications for long-term value investors.

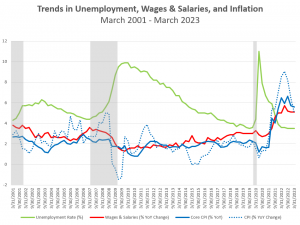

On the topic of slowing economic growth, the common narrative we hear from bullish equity investors is that a soft landing, which avoids a profits recession, is still most likely. Advocates for the soft landing scenario argue that inflation is already declining and labor markets are gradually softening due to the lagged effects of rate increases last year and, more recently, the increased tightening of lending standards due to various bank failures. Imminent declines in inflation mean interest rates have peaked and should be flat-to-falling which will likely boost valuations for stocks and more than offset any weakness from slowing economic growth. As shown in the chart below, however, the trends in wages and salaries, the unemployment rate, and the Core Consumer Price Index (CPI) aren’t yet showing clear signs of easing. While the headline CPI appears to have rolled over, that is largely attributed to declines in volatile energy and food prices. The Federal Reserve tends to emphasize trends in Core CPI when evaluating interest rate policies.

[1] Bloomberg News survey of economists April 21-26 (Economists were asked if the U.S. would have a recession in the next 12 months).

Recessions are shaded. YoY = Year over year

Sources: U.S. Bureau of Labor Statistics (BLS), Intrinsic Research, Poplar Forest Capital

Declines in various leading indicators of economic growth offer credible reasons to think Core CPI will trend lower but the pace and magnitude of the decline is open to debate. Bullish investors appear to be assuming a “just right” goldilocks scenario in which Core CPI steadily contracts to the Fed’s 2% target in concert with a progressive weakening in wage growth and employment. Such a scenario is certainly possible but history would suggest complex systems like the economy and stock market often respond in unpredictable ways to major environmental changes like the dramatic increases in inflation and interest rates over the last 12-18 months. We don’t have high conviction around how fast wages and labor markets will cool or how quickly interest rates and interest expense may decline. As a result, we continue to take a conservative stance on expectations for our portfolio companies’ profit margins in 2023. We also wonder whether the soft landing logic calling for unemployment to trend gradually higher implies that consumer spending will trend lower as people lose their jobs or become fearful of unemployment. If consumer spending weakens, it will become harder for many businesses to grow their earnings in 2023 or 2024. A rising risk of earnings disappointments in 2023-24, to our eyes, doesn’t appear to be factored into the stock market’s current valuation.

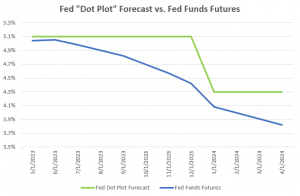

On the topic of interest rates, a relatively large gap continues to persist between the Federal Reserve’s forecast or “dot plot” and market expectations as measured by the Fed Funds future rate. As shown in the chart below, the Fed’s most recent forecast assumes interest rates stay elevated at over 5% throughout 2023 whereas the fixed income market is now pricing in an expectation for interest rate cuts this summer and a Fed Funds rate closer to 4% by year-end. A stock market bull might argue the bond markets are telling us that inflation is last year’s problem and growth enhancing interest rate cuts are just around the corner. Many fixed income investors, however, would assert that the inverted yield curve and these same market implied expectations for rate cuts reflect–not a benign outlook for the economy–but rather, a view that the Federal Reserve has hiked interest rates too aggressively, a recession is now all but guaranteed, and the Fed will have to cut rates in response to worse than expected economic trends.

Fed Dot Plot Forecast represents the median forecast from the last FOMC projection (3/22/23).

Fed Fund Futures data as of 5/5/2023.

Sources: Federal Reserve, Jones Trading, Bloomberg, Poplar Forest Capital

In trying to reconcile the conflicting narratives about the economy, equity markets, and bond markets our sense is that prices for the majority of stocks assume the soft landing scenario is most likely, labor markets will gradually weaken, a recession will be avoided, and corporate earnings will continue to grow in 2023-24. In contrast, fixed income markets may be signaling an increased likelihood of a recession and earnings pressures in 2023-24. We continue to advocate a conservative approach to underwriting our investments and embed a mild recession into our multi-year earnings forecasts.

While the stock market as a whole may not be compensating investors for the risk of a potential recessionary decline in earnings during 2023-24, there are many individual companies that do. For instance, a small but growing list of industries including Semiconductors, Advertising, Freight Services, Home Goods, and Building Products (to name a few) are experiencing sales, orders, and/or earnings trends consistent with an economic downturn. In some cases, the stock prices of companies within these industries have fallen to levels which offer an attractive risk vs. return ratio for long-term investors. One way to mitigate the risk of a recession in 2023-24 may be to focus on companies that never experienced a strong upcycle in demand or have already been revalued lower to reflect an imminent decline in sales and earnings. Among this cohort of companies, we continue to be most interested in the select few that have compelling idiosyncratic plans underway to meaningfully improve their earnings power over the next 3-5 years.

DISCLOSURES

The Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. The summary and statutory prospectuses contain this and other important information and can be obtained by calling 1-877-522-8860 or by visiting www.poplarforestfunds.com .Read it carefully before investing.

Mutual fund investing involves risk. Principal loss is possible. The funds may invest in debt securities which typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. The funds may invest in foreign securities which involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks are greater in emerging markets. Investing in medium sized companies may involve greater risk than investing in larger, more established companies because medium capitalization companies can be subject to greater share price volatility. The funds may invest in options, which may be subject to greater fluctuations in value than an investment in the underlying securities. When the Funds invest in other funds and ETFs an investor will indirectly bear the principal risks and its share of the fees and expenses of the underlying funds. Investments in asset-backed and mortgage-backed securities involve additional risks such as credit risk, prepayment risk, possible illiquidity and default, and increased susceptibility to adverse economic developments.

Diversification does not assure a profit, nor does it protect against a loss in a declining market.

Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Fund holdings and sector allocations are subject to change and should not be considered recommendations to buy or sell any security.

Past performance does not guarantee future results. Index performance is not indicative of fund performance. To obtain fund performance, visit www.poplarforestfunds.com or call 1-877-522-8860.

Consensus Earnings Estimate: A forecast of a public company’s projected earnings based on the combined estimates of all equity analysts that cover the stock.

Core Consumer Price Index (CPI): Measures the average change in prices paid by consumers over a period of time for a basket of goods and services, not including those from the food and energy sectors.

Earnings Growth: The annual rate of growth of earnings typically measured as Earnings Per Share Growth.

Fed Funds Future Rate: This rate represents the general market consensus of where the daily official Fed Funds rate will be at the time a specific Fed Funds futures contract expires.

Inflation: Is a quantitative measure of the rate at which the average price level of a basket of selected goods and services in an economy increases over a period of time. Often expressed as a percentage, inflation indicates a decrease in the purchasing power of a nation’s currency.

Price/Earnings (P/E) Ratio: Is a common tool for comparing the prices of different common stocks and is calculated by dividing the earnings per share into the current market price of a stock.

S&P 500 Index: Is a market value weighted index consisting of 500 stocks chosen for market size, liquidity and industry group representation. The Index is unmanaged, and one cannot invest directly in the Index.

Valuation Multiple: Ratios, such as price/earnings (P/E) and price-to-book (P/B), that describe financial factors of a company, providing clear and easily comparable data.

Yield Curve: Is a line that compares the yield of bonds of equal quality but different maturity dates. In general, bonds with longer maturity dates offer higher yields than bonds with shorter maturity dates, thus producing an upward sloping yield curve.

Poplar Forest Capital, LLC, is the adviser to the Poplar Forest Funds, which are distributed by Quasar Distributors, LLC.

Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.