")

Dear Shareholders,

“Do you want cheese on it?” I was new to L.A. when I was asked that question that I’ll never forget. A recent acquaintance had invited me to his house for a barbecue, and I was excited! I have long loved BBQ, which to me means meat cooked low and slow on a smoker. Adding cheese was unheard of where I come from.

“Cheese on what?” I responded. Which is when my new friend gestured to a hamburger and revealed to me that in California, “barbecue” refers to the grilling of meat. As I reached for a bun, I was polite enough not to yell, “This isn’t BBQ!” But inside my head, I was certainly thinking it.

Don’t get me wrong – I love grilling meat over charcoal. During the week, you’ll often find me right before dinner, hovering over my beloved Weber Kettle. But on the weekend, there are few things I like more than patiently cooking a low-priced cut of meat (beef brisket or pork shoulder, for example) for hours in the smoke from an oak or hickory fire. I’ve spent a couple decades perfecting my own rubs and sauces, and while I may not be as accomplished as Aaron Franklin, my kids, friends and neighbors all give my “Cue” high marks.

For the uninitiated, Aaron Franklin is one of America’s most famous pitmasters and a past winner of a prestigious James Beard Foundation award for best chef in the Southwest. For me, his book, “Franklin Barbecue – a Meat-smoking Manifesto” is as fundamental to the craft of barbeque as Graham & Dodd’s famous treatise “The Intelligent Investor” is to value investing. As Bon Appetit writer Andrew Knowlton put it:

“I used to think of Aaron Franklin as a genius: There was the rise from backyard dabbler to king of the Texas pitmasters: his mind-altering brisket that made normally rational people (myself included) wait hours for the chance to eat it: and his insistence that game-changing barbecue doesn’t come from miracles but rather from elbow grease. Then he wrote this book and gave all his secrets away. Now everyone – from me to you to your neighbor who can’t grill a chicken breast – will be able to make award-winning barbecue. He’s not a genius anymore; he’s a god.”

An expert pitmaster can transform an otherwise cheap and tough hunk of meat into a tender, tasty bite of heaven. Likewise, I believe that Poplar Forest’s experienced investment team can seek to transform inexpensive stocks into market-beating, long term investment results. While investors currently seem more interested in paying a premium for the stock market equivalent of Wagyu Beef, my colleagues and I are still following a time-tested recipe to cook up what we believe is mouth-watering value-stock barbecue. Why? Because we continue to believe that Contrarian Value investing offers a long-term, risk/reward ratio that is superior to that of the S&P 500.

For example, our portfolio is currently trading at a price-to-forward-earnings (P/E) ratio of 12.8x while the S&P is valued at 21.7x. Normally, one would expect the more highly valued S&P to offer better growth, but the consensus opinion of Wall Street’s analysts is that our portfolio can produce 13.8% earnings growth over the next three years while the S&P is expected to grow 13.2%. In addition to offering potential for better growth, the companies that we have paid dividends and have produced more than 1% more income each year as compared to the S&P 500. At a time when the S&P 500 seems to embed lofty expectations for the future, we’ve identified a collection of thirty business that we believe offer better fundamentals at a highly discounted valuation. Doesn’t that sound delicious?

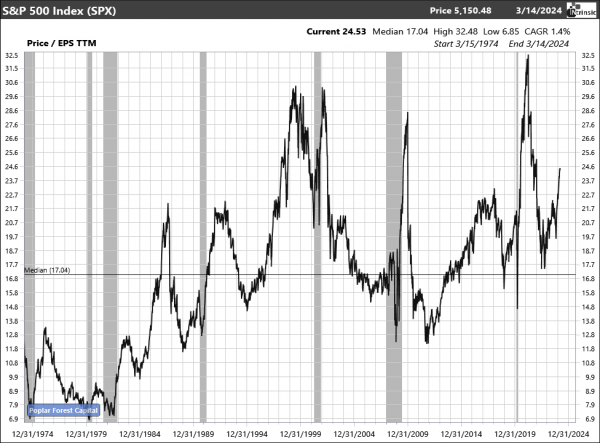

S&P 500 – Investor Enthusiasm Only Higher During the Tech Bubble

I agree with the oft-repeated observation that valuation is a terrible market timing tool, but I believe it can be informative in assessing risk and reward. Expensive stocks can keep rising, but the higher they go, the more they may fall when conditions worsen. As you can see in the chart below, on a price-to-trailing-earnings basis, the S&P is currently valued at 24.5x. Absent recessionary periods when earnings were depressed, this valuation measure rarely exceeds 20x. In March 1998, the S&P first breached 24.5x during the inflating of the Tech Bubble. Admittedly, stocks kept going up and the trailing P/E ultimately expanded to more than 30x in 1999 just before the market peak, so perhaps there is more upside ahead, but I believe the S&P 500 has become an un-appetizing long-term investment. From March 1998 when 24.5x was first breached, the S&P 500 produced a 10-year return of 3.6% per year (less than investors can currently get on a low risk 10-year Treasury bond); Value stocks beat the S&P by roughly 2% a year over that decade.

(Source: Intrinsic Research)

While many market commentators credit the stock market’s recent heady gains to euphoria about Artificial Intelligence, I believe the cause may be the strength of a U.S. economy that has grown more than twice as fast as major developed markets in Japan and Europe since the end of 2019. Unemployment has been below 4% for 25 straight months, the longest such streak in more than five decades. At a time when many economies in Asia and Europe are either in (or on the verge of being in) recession, the U.S economy continues to look surprisingly robust. Non-U.S. investors may look at our seeming prosperity and technological advantages and conclude that paying up for U.S. stocks is a better deal than what they find available in their home markets. Foreigners looking to escape stagnation and/or recessionary downside may view the biggest and most well-known companies in the U.S. as the easiest place to stash their cash. Foreign interest in the biggest U.S companies may help explain the massive valuation differential between Megacap (the biggest 200) and Midcap (the next 800) and Smallcap stocks.

As long as the U.S. economy is the strongest in the world, the popular stocks currently driving the market may keep rising. The evidence suggests a couple key variables that have driven our relative prosperity: the response to COVID and immigration. According to a recent article in The Economist, U.S. COVID stimulus payments equaled 26% of GDP – more than double the developed world average. The article goes on to suggest that the U.S. workforce is 4% higher now than it was in 2019, largely due to legal and illegal immigration – and the illegal part of that influx may well be underreported. With U.S. Government spending getting increased attention now that interest payments exceed defense outlays, and with both of the leading presidential candidates promising a crackdown on illegal immigration, the underlying sources of our superior growth may be in question. With so much riding on upcoming elections, it is hard to know how things may look in 2025, so for now, investors are simply focused on AI-led productivity gains, current economic strength, and reductions in interest rates that are expected to continue fueling that growth.

Momentum is a powerful force in investing. Many people feel most comfortable owning what’s currently “working” in the market while ignoring what’s not. Megacap Growth stocks (like Prime steaks sizzling on the grill) are getting all the attention while Value stocks (the BBQ meat of the investing world) seem to be stuck in neutral. But in my opinion, this performance differential has set us up for what I believe will be market-beating results in coming years. At a time when stocks, as measured by the S&P 500, seem expensive, our portfolio appears to offer great value.

A Value Stock “Stall” May Offer Opportunity

After advancing at a better than 36% annualized rate from the COVID market low in March 2020 to the end of 2021, Value stocks, as measured by the Russell 1000 Value Index, have produced a more tepid annualized return of 5.3% since then. This reminds me of my early days smoking brisket. I remember one particular afternoon when everything seemed to be going according to plan. Then, after something like six hours in the smoker, the meat seemed to have stopped cooking – the readings on my meat thermometer didn’t budge. I started to panic because I had people coming over to eat and the meat wasn’t cooperating! I took a deep breath and reached for Aaron Franklin’s book for a refresher on something pitmasters call the “stall.”

“What is the stall? … a big piece of meat cooking in the smoker hits a patch in its progress where cooking appears to stop… At first, the temperature goes up and up, just as anything we cook always does. And then, gosh darn it, it levels off. This usually occurs at 160 or 170 degrees. And it stays leveled off. And it stays. And it stays at the same temperature until you think it’s not going to get any higher. This freaks people out. It sure did me when I first encountered it.

What do freaked-out people do with meat that’s stuck at the same temperature for hours? They’re not stupid – they pull it off… And then they cut into it only to find the brisket is as tough as a sneaker.

Anyone can be forgiven for doing this, because the stall defies logic. Not only does the meat hold the same temperature for hours in an oven-like environment, sometimes it can actually be observed dropping in temperature. So what gives?” –From Franklin Barbecue

I’ve learned that as a brisket cooks, it reaches a point when surface moisture evaporates – it’s as if the meat is sweating the way we humans do – and that evaporation cools the meat. This continues until the surface of the meat has no more moisture to give and resembles something like the bark on a tree. Once sealed by the bark, the internal temperature can start rising again until reaching perfection somewhere between 200 to 210 degrees. The moral of the story is this – while a meat thermometer may suggest that the meat’s not cooking, it still is! And once it gets through the awkward stall, the magic really happens. Staying the course is critical to producing perfect brisket.

A similar process has been going on in our portfolio. It may have looked like nothing was happening, but below the surface, conditions appeared optimal. Despite the low P/E ratio, we believe our portfolio’s 13% expected annual earnings growth and attractive first quarter gains show that the portfolio is cooking!

We Don’t Skimp on Ingredients

Making good brisket takes time – not just for the cooking, but also for the prep. While I could just run down to the local bargain grocer to get whatever is on special, I take the time to visit my favorite butcher who carries organically raised, grass-fed beef. I bring the meat home, trim off the excess fat, and then coat it with my proprietary rub of salt, pepper and spices. I also prepare my own brisket sauce – a tomato-based recipe much different than the vinegar-based sauce I use on ribs or pulled pork. All this takes place well before I rise before dawn to build an oak fire in the Lyfe Tyme smoker I’ve had for 20 years. In the late 1970’s, Charles Davenport, of Uvalde, Texas, began building Lyfe Tyme cookers by welding together pieces of ¼ inch steel pipe left over from the installation of oil pipelines (yet another example of turning inexpensive materials into BBQ gold) and I’ve produced countless feasts in my custom built, seven foot long rig.

In the same way that I am particular about my barbecue ingredients and cooking tools, we at Poplar Forest are very picky about the stocks that go into our portfolio. We don’t simply buy the cheapest stocks we can find; we look for bargain-priced companies that have the pedigree of prime, grass-fed beef. If a company can’t grow, has an over-levered balance sheet, or a poor history of free cash flow generation, we’ll generally look elsewhere. Even then, our research process is much like the extensive pre-cooking prep required for a good brisket.

Yes, I’m going to see if I can beat this metaphor to death, as if tenderizing a thick chuck steak: Once a stock makes its way into the Poplar Forest smoker/portfolio, we tend the fire carefully, while monitoring quarterly earnings and checking in with management to see if their business is going to plan. Importantly, we don’t panic when the portfolio stalls – we know that’s part of the process. Just as good brisket takes time and effort, building a great contrarian value portfolio is a lot of work, but I love the work and believe the extra effort produces better results.

Because we are choosey about what we cook, we didn’t add any new stocks to the portfolio over the last three months. We have a number of companies that we’d be excited to buy if prices drop a bit, but we don’t feel any pressure to act because we feel great about the risk/reward ratios of the stocks we currently own. At a time when investors seem focused on trading cryptocurrencies and finding the next AI winner, we’re going to keep doing what we’ve done from day one at Poplar Forest: seek out market-beating, long-term investments in underappreciated companies and industries by focusing on their normalized earnings, free cash flow, financial strength, and sustainable organic growth.

I’ve been picking stocks and smoking meat for decades and I agree with Andrew Knowlton’s observations about pit-master Aaron Franklin. To paraphrase: we believe game-changing barbecue and market-beating value investments don’t come from miracles but rather from elbow grease and patience. At Poplar Forest, we’ve got both. I believe that our investment process works well in the long run, and that it is particularly compelling now with the S&P 500 at all-time high levels. Prime steaks may currently be expensive, but brisket is on sale!

I greatly appreciate the partnership we have with all of you; I’m going to continue to pursue my passions for barbecue and value stocks with the confidence that we’re cooking up a great meal. Bon appetit!

Sincerely,

March 31, 2024

Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.