Poplar Forest Analyst Insights: Coronavirus Update & Healthcare Overview

Coronavirus update – investor sentiment may shift once an effective therapy is approved.

The global spread of the Coronavirus (COVID-19) is creating panic in financial markets. We appear to be in a period of maximum uncertainty characterized by a rapidly expanding list of questions, but few, if any, answers. Over the coming weeks, it seems likely that patient counts may dramatically increase in the U.S. and create some short-term pressure on economic activity. As patient counts rise, the American media will predictably stoke public fears of an intractable pandemic. Contrary to these fears, we see encouraging reasons to believe that an effective therapy could be approved within the next few months. We also believe the fatality rate in the U.S. could be much lower than in China, where smoking is more prevalent.

If, similar to many other respiratory viruses, the transmission of Coronavirus is reduced by heat and humidity, patient counts may also show a seasonal decline during the summer. By this time next year, it is quite possible that the Coronavirus is viewed as just a new strain of flu with a low fatality rate. The historical pattern of using human ingenuity to solve novel problems is already unfolding as the best and brightest minds in the Healthcare sector work to quickly develop new vaccines and therapies. While we proclaim no edge in predicting the spread of a novel virus, we would simply observe that a reasonable fact pattern exists for believing that the current economic expansion won’t be completely derailed by the Coronavirus.

Our research into the Coronavirus outbreak suggests true patient counts in China and elsewhere have been dramatically understated due to faulty diagnostic tests which suffer from high rates of “false negatives” or missed patients. Since Coronavirus symptoms are hard to distinguish from the seasonal flu, many people infected with the virus have likely been misdiagnosed as having the seasonal flu. These misdiagnosed patients are likely to have transmitted the virus to people with whom they have had close contact. While better diagnostics will soon be available, the virus has already spread around the world. The silver lining of the actual patient count being higher than the reported patient count is that the risk of death from the virus is likely to be much lower than the estimated 2-3% fatality rate disclosed by China. The Chinese government appears to be making a good faith effort to share as much accurate information with the world as possible. For instance, in mid-February, China’s Center for Disease Control (CDC) published data on over 70,000 patients thought to have been infected1. The data showed a clear correlation between age and death rates, with no fatalities among children aged 0-9, a .2-.4% fatality rate among 10-49 year olds, and a 1-15% fatality rate among people aged 50-80+. The virus appears to be particularly problematic for elderly patients with respiratory problems. The data also showed a much higher fatality rate among men than women which is likely explained by different prevalence rates of smoking. China has the largest adult smoking population in the world with 52% of men estimated to smoke but only 2.7% of women, resulting in an overall prevalence of 28%2. In the U.S., the latest estimate from the Centers for Disease Control (CDC) is that roughly 14% of the adult population smokes with a modestly higher prevalence rate among men than women. The combination of a much lower prevalence of smokers and a vastly superior healthcare system suggests to us that death rates in the U.S., and many other countries, are likely to be significantly lower than in China.

The most important development for patients and market sentiment will be news of an effective therapy. On this front, there is cause for optimism. In February, Gilead Sciences moved a promising anti-viral agent, Remdesivir, into two large placebo-controlled trials in China with data expected in April. If favorable, the product could be immediately approved and likely become broadly available. Remdesivir interferes with a virus’ ability to replicate itself and showed favorable results treating the Ebola virus. The first confirmed Coronavirus patient in the U.S. was given Remdesivir in January. After treatment, his symptoms immediately improved and he was subsequently discharged. The prior development of functional cures for nasty viruses such as HIV and Hepatis C suggests humanity’s ability to understand and rapidly develop antivirals has never been better. Gilead’s Remdesivir is just one of 80 products currently in clinical trials in China and elsewhere. Vaccines are also in development but will take longer to validate. The current negative news cycle may persist in the short run, but announcements around effective therapies may only be a few months away.

Another Healthcare related concern for investors is the impact of Democratic candidates like Bernie Sanders winning the 2020 Presidential election. As we discuss below, we believe fears of dramatic regulatory changes to the Healthcare sector are creating attractive long-term investment opportunities.

The Healthcare sector offers attractive growth potential at below average valuations.

Healthcare is our second largest sector weighting and comprised 16% of year-end assets in the Partners Fund. During 2019, fears of negative regulatory changes caused the Healthcare sector to underperform the S&P 500 Index by over 1,000 bps and relative valuations for many Healthcare companies compressed towards ten year lows. Some investors are scared that policy proposals from Democratic Presidential candidates like Bernie Sanders could broadly impair the pricing power and profitability of Healthcare companies. We believe these regulatory concerns are overstated and create an opportunity to selectively invest in businesses with attractive growth potential that are trading at below average valuations. In the following discussion, we analyze key trends impacting the Healthcare sector and outline our approach to finding investments capable of offering attractive returns relative to the market and relative to other defensive sectors.

Favorable demographics and a new innovation cycle suggest the “trend is your friend.”

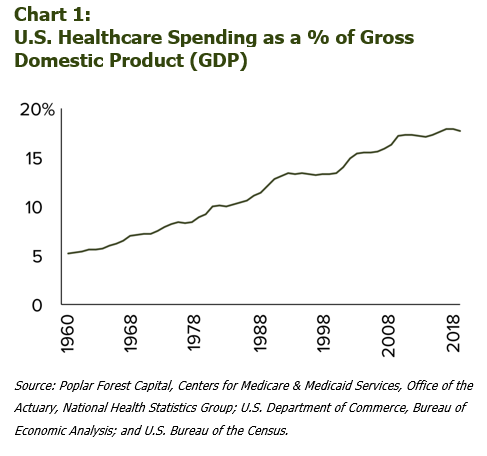

As the chart to the right highlights, in 1960, Healthcare spending in the U.S. consumed 5% of gross domestic product (GDP), a broad measure of economic activity. If we fast forward to 2019, Healthcare spending is estimated to have grown to 18% of GDP. While the growth rate in Healthcare spending has slowed over time, trends in demographics and technology suggest it will continue to grow faster than the overall economy. In fact, according to the Centers for Medicare and Medicaid Services (CMS), which oversees Healthcare initiatives for the government, Healthcare expenditures are forecasted to annually grow 6% and reach $6 trillion by 20273.

Healthcare spending patterns change as people age which explains why demographic trends can influence the Healthcare sector’s growth rate. Data from a 2016 Kaiser Family Foundation (KFF) analysis suggested that when Americans transition from the 55-64 year age range to the 65+ cohort their Healthcare expenditures increased by almost 50%4. This helps explain why Americans aged 65+ account for 36% of national Healthcare spending but only 16% of the U.S. population. Over the next ten years, as the Baby Boomer generation ages, the number of Americans in this higher-spending age group is expected to grow 3% per year which is more than three times faster than the expected growth in Americans under the age of 65.

Healthcare spending patterns change as people age which explains why demographic trends can influence the Healthcare sector’s growth rate. Data from a 2016 Kaiser Family Foundation (KFF) analysis suggested that when Americans transition from the 55-64 year age range to the 65+ cohort their Healthcare expenditures increased by almost 50%4. This helps explain why Americans aged 65+ account for 36% of national Healthcare spending but only 16% of the U.S. population. Over the next ten years, as the Baby Boomer generation ages, the number of Americans in this higher-spending age group is expected to grow 3% per year which is more than three times faster than the expected growth in Americans under the age of 65.

Growth in Healthcare spending from demographics is being amplified by recent breakthroughs in technology. As shown in the graph below, during the last few years, there has been a meaningful increase in new drug approvals. Many of these new drugs are dramatically improving the lives of patients and garnering significantly higher prices than prior therapies. While the rate of new drug approvals can be volatile in any given year, the uptrend in approvals is likely to continue as new technologies permeate the sector. The cost to analyze genetic information in people, cancer cells, viruses, etc. continues to plummet and is yielding new insights about how to treat and cure human diseases. These new insights into human disease are dovetailing with breakthroughs in our ability to genetically edit and manipulate human cells. While one can debate whether the average American is getting healthier, many new drug therapies are unequivocally improving the quality of life and survival rates for Americans with severe diseases. Some readers may recall a recent Wall Street Journal article entitled, “US. Cancer Death Rate Drops by Largest Amount on Record” that highlights the positive impact of some of these new products5. The combination of favorable demographics and accelerating innovation leads us to view CMS’ forecast for 6% annual growth in Healthcare spending as a likely outcome.

Regulatory risks – just a cough or pneumonia?

While everyone is in favor of medical breakthroughs, few want to pay for it. Since most Americans of voting age have experienced rising Healthcare costs, Healthcare is a particularly popular political topic. Democratic Presidential candidates like Bernie Sanders and Elizabeth Warren have proposed implementing dramatic changes to the Healthcare sector and advocate replacing private insurance with a public “Medicare for All” type of system. Taken at face value, their proposals would impair the pricing power and profitability of many Healthcare companies. Not to be outdone, the Republicans also want to claim Healthcare reform as their issue but are proposing less onerous policy changes. This whirlwind of competing Healthcare proposals creates an intellectual tug-of-war for investors. On the one hand, the sector offers investors attractive long-term growth potential; on the other hand, a President Sanders or President Warren could implement policies that pressure Healthcare profitability.

We believe that fears of dramatic regulatory change are overstated and create an opportunity for long-term investors to selectively invest in Healthcare businesses with attractive growth prospects that are trading at below average valuations. History suggests that many of the policies a Presidential candidate advocates in order to win an election are never implemented and, for the few that are, substantial revisions are usually required. Prior attempts at major reform, such as the “HillaryCare” proposals during the Clinton Presidency of the 1990’s or the more recent changes stemming from “Obamacare,” have either failed outright or, over time, been attenuated to palatable levels by industry lobbyists.

While we do have opinions on the upcoming Presidential and Congressional elections, we don’t have an advantage in predicting their outcome. This fact creates a conundrum since, if Sanders or Warren were to become President and the Democrats were to take control of Congress, then the odds of onerous reforms would rise and the valuations of many Healthcare companies would fall. Political betting markets such as PredictIt.org suggest the conditional probability of this sort of election outcome is somewhere between 5-20%. While many Healthcare investors may find solace in a 5-20% chance of losing money, we believe downside risks can be further mitigated by only investing in companies that create clear value for society.

Companies “saving lives” or “saving dollars” are best positioned to navigate regulatory change.

Healthcare companies with strong value propositions that are focused on saving lives or saving dollars offer investors a bridge over the chasm of potential regulatory risks. For instance, the two drug companies we own in the Partners Fund, Merck (MRK) and Eli Lilly (LLY), have both successfully built their businesses around developing best-in-class therapies for severe diseases. Whatever the shape of future regulations, we believe these sorts of high-impact products will get reimbursed in developed markets. The same likely can’t be said for drug therapies offering marginal improvements in efficacy, safety, or convenience. We believe companies focused on making Healthcare spending more efficient, such as pharmacy and insurer CVS Health (CVS) and distributor AmerisourceBergen (ABC), are also well positioned to navigate potential regulatory change. Our investment thesis for both CVS and ABC is rooted in the significant cost savings these businesses deliver to the Healthcare system.

Healthcare companies can grow even when the economy doesn’t.

In addition to regulatory change, many investors are also fearful of an economic slowdown. While we don’t know when the next recession will come, we believe the Healthcare companies we own can grow even if the economy doesn’t. Healthcare was one of the few parts of the economy that grew during the Great Recession of 2008-2009. The sector’s steady growth makes sense since most Healthcare expenditures are non-discretionary and most Americans have health insurance. This ability to consistently grow, even when the economy doesn’t, leads many investors to label the Healthcare sector as “defensive.” Utilities, Real Estate Investment Trusts (REITs), and Consumer Staples are examples of other sectors in the S&P 500 Index that investors consider defensive.

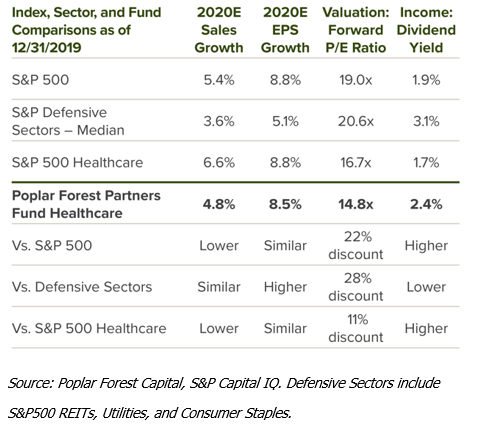

Compared to these other defensive sectors, Healthcare offers investors better growth prospects for sales and earnings per share (EPS) and can be bought at a 19% lower valuation. While the Healthcare sector currently pays a lower dividend yield than other defensive sectors, we don’t think that justifies the current valuation discount. As detailed in the table below, the Healthcare investments in the Poplar Forest Partners Fund trade at an 11% discount to the broader Healthcare sector, a 28% discount to other defensive sectors, and a 22% discount to the S&P 500. For all of these reasons, we believe our investments in the Healthcare sector can continue to generate favorable risk adjusted returns for our clients.

Let’s Discuss

We’d love to continue the conversation. Please contact Patty Shields (pshields@poplarforestllc.com or (626) 304-6045) if you’re interested in scheduling a call to discuss this or any other topic of interest.

1 http://weekly.chinacdc.cn/en/article/id/e53946e2-c6c4-41e9-9a9b-fea8db1a8f51

2 https://www.ncbi.nlm.nih.gov/pmc/articles/PMC6546632/

3https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/NationalHealthExpendData/Downloads/ForecastSummary.pdf.

4https://www.healthsystemtracker.org/chart-collection/health-expenditures-vary-across-population/#item-family-spending-also-is-concentrated-with-10-of-families-accounting-for-half-of-spending_2016.

5https://www.wsj.com/articles/u-s-cancer-death-rate-drops-by-largest-amount-on-record-11578484809?shareToken=st2da805be8e2844909a29688515dc0f2a&reflink=article_email_share.

Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.