")

Dear Partners,

On May 10, 1965, Warren Buffett’s investment fund, Buffett Partnership Ltd, took control of a struggling textile company called Berkshire Hathaway. Six decades later, on May 3, 2025, Buffett announced plans to retire as CEO. In the intervening 60 years, Berkshire’s stock price increased from roughly $19 per share to $809,350 for annualized returns of more than 19% per year as compared to the 8.5% return of the S&P 500. In my book, Buffet is the greatest investor of all time. I doubt that anyone will ever outshine him.

When I was buying my first stocks back in the spring of 1980, Warren Buffett was already famous. I remember reading (and re-reading) the Graham & Dodd texts that inspired Buffett as well as his annual shareholder letters. His approach made intuitive sense to me, and I incorporated many of his teachings into an investment philosophy and practice that I have followed for more than 30 years now. If you ask me, the most important of those foundational principles are these three:

- Think like an owner

- Be selective

- Spend lots of time on business fundamentals and little time on macroeconomics

In this letter, I want to share my interpretation of Buffet’s lessons and how they apply to the current investment environment.

Maintain An Owner’s Mentality

“We don’t think of ourselves as buying and selling pieces of paper but rather investing in businesses.” – Warren Buffett

These days stocks are often referred to as “names” and identified by their stock symbols — mere pieces of electronic paper. This has been accompanied by seemingly ever shorter investment time horizons – it’s as if investors are merely renting stocks. At a time when so many others are ignoring the wisdom of the world’s greatest investor, the Poplar Forest Team at Tocqueville is going to continue to think like long term owners of businesses.

I don’t know of business owners who concern themselves with valuing their companies every day, much less minute-to-minute. There is far too much else to do: trying to grow while managing costs, delighting customers while keeping competitors at bay, and striving to ensure there is more money in the bank at the end of the year. When we evaluate a business, we pay attention to the company’s underlying business. For example, is the company taking market share? Does it have astute management? Does it generate an attractive return on investment? How’s the balance sheet, and how much money can the enterprise earn in the long term?

“Only buy something that you’d be perfectly happy to hold if the market shut down for 10 years.” – Warren Buffett

In evaluating businesses, our team continues to focus on normalized earnings power and free cash flow after considering the company’s growth potential. Many investors talk about their focus on “cash flow” and by that they mean Earnings Before Interest, Taxes, Depreciation and Amortization (EBITDA). I am not a fan of this measure, which I consider “gross” cash flow. Like business owners, we care about “free” cash flow – how much money is left over after paying all the company’s bills and investing for growth.

For a business owner, interest and taxes are real expenses. Not only does EBITDA ignore those expenses, it also fails to account for the expenditures required to maintain and grow the business. And unlike an increasing number of investors, our team also considers stock-based compensation to be a real expense and exclude it from our calculations of free cash flow. While our approach to calculating free cash flow may be more conservative than others, we believe it is prudent and consistent with an owner’s mentality.

Choose Carefully

“The stock market is a no-called-strike game. You don’t have to swing at everything — you can wait for your pitch.” – Warren Buffett

With a process that focuses on our highest conviction ideas, and a three-to-five year holding period, we typically make just a handful of new investments each year. Before joining Tocqueville in April, Poplar Forest’s four-person analyst team reviewed more than 60 ideas a year and we ultimately invested in fewer than 15% of them. As part of Tocqueville, we now have access to a larger analyst pool and to the ideas generated by other portfolio managers. In short, we have even more ideas to choose from, and that will allow us to be even more selective. As we’ve gotten to know our new colleagues, I’ve been very impressed with the quality of their work. In just ten short weeks of collaboration, they have already started to have an impact on our portfolios. In the second quarter, for example, we made two new investments – Nucor and Stanley Black & Decker. One was a Poplar Forest Team sourced idea and one was surfaced by a legacy Tocqueville analyst.

Nucor is one of the leading steel producers in the U.S. While steel-making is a capital intensive, cyclical business, Nucor has developed an enviable position as a low-cost producer that has taken market share for many decades. The business has a conservative balance sheet and has consistently generated free cash flow. Management is shareholder focused, and the company has a 52-year record of annual increases in the dividend. Many of you will have heard of the term “Dividend Aristocrat” (a stock market index composed of the companies in the S&P 500 that have increased their dividends in each of the past 25 consecutive years). Well, Nucor leaves that index in the dust. It is one of only 55 companies that have increased their dividend annually for at least 50 years, making it a “Dividend King”!

Because of the cyclical nature of the business, we have gotten an opportunity to invest in this great company at what we believe is a very attractive price. Over the last 30 years, the company has been valued at a 100% premium to its book value (the value of its assets less the value of all its liabilities) and we’ve acquired shares at a premium of just 32%. On this basis, the stock has only been cheaper one time: during the depths of the COVID Crisis.

One reason the stock is trading at a discounted level is that Nucor is currently investing heavily for growth while margins are cyclically depressed. While earnings this year may come in below $8 a share, as we look out a few years, we believe that earnings can recover to a more normalized $16 per share with free cash flow of $12 per share. At current prices, the stock appears very attractively valued at a normalized P/E ratio of just 8x and at roughly 10x our estimate of normalized free cash flow. Nucor has historically traded at 14x earnings.

Stanley Black & Decker is a leading producer of hand tools that has been suffering from post-pandemic weakness in the home construction and remodeling markets. Despite softness in its end markets, the company has an enviable long-term track record, and — like Nucor — it is a Dividend King.

More recently, the stock has also been penalized, we believe inappropriately, by concerns about the potential impact of tariffs on the company’s business. Stanley produces roughly 50% of its products in the U.S., with another 15% coming from China, and 35% from other countries. As President Trump ratcheted up tariffs on our trading partners, especially China, investors sold the shares of companies they perceived to be a tariff “losers,” and Stanley was among them. The company reduced its earnings guidance for 2025 by roughly 15% due to tariff impacts and the company’s stock fell by twice that amount as investors feared that management wasn’t being cautious enough in their assessment of potential demand destruction. But we smelled opportunity; we believe the company is not a tariff loser, but more likely a tariff winner. What investors failed to appreciate, in our opinion, is Stanley’s advantaged position relative to its major competitors who get two-to-three times more of their products from China. In effect, all of Stanley’s competitors will have to increase prices far more than Stanley will and we believe that may allow for substantial market share gains.

In addition, Stanley’s management team has laid out a plan to drive their gross margins to 35% by 2027. Investors have been skeptical that the company can achieve these gains, but if they were to do so, their earnings could reach $9 per share in 2027 as compared to a depressed $4.50 this year. We believe management has a good shot at achieving their goals, but we assume it will take another year or two to get there. For a stock that has historically traded at 17x earnings, we see substantial upside from current prices. On our estimates, the stock is trading at less than 8x our normalized earnings estimate and 10x our assessment of normalized free cash flow.

Understand the Big Picture, but Don’t Let it Distract You

“I don’t pay any attention to what economists say, frankly. Well, think about it. You have all these economists with 160 IQs that spend their life studying it, can you name me one super-wealthy economist that’s ever made money out of securities? No.” – Warren Buffett

Given all that is going on in the world today, it is easy to get distracted by macroeconomics and geopolitics. These issues can’t be ignored, but they aren’t areas in which we have a competitive advantage. Our team tries to stay cognizant of big picture risks and opportunities, while at the same time continuing to build our high-conviction portfolios from the bottom up and with the mindset of owners (not renters) of securities. Macroeconomic conditions are cyclical; the longer the time horizon, the less one needs to worry about the ups and downs of the business cycle.

For those investors attempting to make money by betting on macroeconomic variables, the current environment seems particularly challenging. There are so many moving parts, from the potential lagged impact of tariffs to war in the Middle East, to more generalized uncertainty that may dampen business appetites for expansion. I found it interesting that when the Federal Reserve recently released its expectations for the expected path of interest rates for the next six months, after two days of deliberations, the nineteen participants (seven Fed Governors and 12 regional Federal Reserve Bank presidents) couldn’t agree: 10 expected two or more rate reductions, two saw a single cut, while seven projected no cuts at all. If the supposed experts at the Fed can’t even agree on the short-term outlook, what is an investor to do?

“If we’re right about the business, macroeconomic factors won’t matter. And if we’re wrong about the business, macroeconomic factors won’t save us.” – Warren Buffett

For the Poplar Forest Team at Tocqueville, our typical investment holding period spans three to five years. That means we try to stay cognizant of the macroeconomic backdrop while staying firmly focused on business fundamentals. That said, the Big Picture issues to which we’re paying closest attention are the situation in the Middle East, and the budget machinations in D.C, as we believe these two factors could have the greatest impact on long-term economic fundamentals. The budget picture, in particular, is one macroeconomic variable that could have a significant negative impact on long-term investments, though in the short run, the picture may look quite different.

For the short-term trader, elevated government spending may support a strong and growing economy with more jobs, healthy consumer spending, and rising earnings. What’s not to like? For the long-term investor, however, persistently high deficits and growing debt relative to GDP raise the risks of higher interest rates and the potential for elevated inflation if the government tries to devalue its debt obligations to ease its financial burden. While I worry about the long-term implication of consistently elevated deficits, concerns over government debt have existed for many years now, and trouble has yet to arrive. This may be one of those subjects that isn’t a problem until it is, but once it becomes a problem, it could be a big one. I’m reminded of this exchange in Ernest Hemingway’s 1926 novel, The Sun Also Rises:

“How did you go bankrupt?” Bill asked.

“Two ways,” Mike said. “Gradually and then suddenly.”

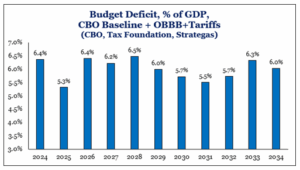

While all the details aren’t yet final, current estimates of the impact of President Trump’s One Big Beautiful Bill suggest worrisome levels of deficit spending. As you can see in the chart below, we may be in for a decade of deficits equal to 6% of GDP. Historically, deficits of this magnitude only occurred in times of crisis, like wars, pandemics or deep recessions. To believe that we can comfortably live with this level of profligate spending, relative to income, without engendering a crisis down the road seems naive to me.

From 1980 through 2020, long-term interest rates dropped from more than 10% to less than 2%. Falling interest expenses helped companies grow their earnings while falling interest rates justified higher P/E ratios. Growing amounts of Government debt relative to the size of the economy could result in some reversal of those four decades of benefit. We’ve already seen 10-year Treasury yields rise to 4.0-4.5%. As companies refinance existing debt at higher interest rates, their interest expenses may grow, thus reducing their earnings growth rate. Stock valuations have been relatively immune to higher rates and perhaps that will continue, but as I look at the next ten years, stock market returns may be disappointingly muted. In that sort of environment, companies with substantial free cash flow generation, discounted valuations, and idiosyncratic profit drivers may be particularly rewarded. Because our portfolio trades at a 40% discount to the S&P 500 on both free cash flow and earnings, despite comparable expected earnings growth, we feel particularly well situated to generate market-beating, long-term investment results.

Closing Thoughts

“Charlie Munger and I happily acknowledge that much of Berkshire’s success has simply been a product of what I think should be called The American Tailwind. It is beyond arrogance for American businesses or individuals to boast that they have ‘done it alone.’” – Warren Buffett

I have long considered myself blessed by the opportunities that have come my way. Investing is a profession of caring for other people’s money that requires continuous learning and the solving of puzzles – two activities that I greatly enjoy. Discovering this calling in my teens has been the proverbial gift that keeps on giving — I love picking stocks and working with clients. For the last 17 years, I also had a business to run. Now that Poplar Forest is part of Tocqueville, those “running the business” tasks have fallen away and I can spend more of my time doing what I love to do.

I have also been blessed to have a large group of mentors and role models to show me the way. Many of those mentors are current clients to whom I’m doubly grateful, while some of my role models, like Warren Buffett, are people I’ve never met, but who have been generous in sharing their wisdom with others. I’m grateful for all the guidance that was embedded in all those carefully written Berkshire Hathaway annual reports. I will do my best to make the most of wisdom I have gleaned from Buffett, and my many mentors and role models, over the years.

“My wealth has come from a combination of living in America, some lucky genes, and compound interest. Both my children and I won what I call the ovarian lottery.” – Warren Buffett

I just turned 60 in June. While I’d love to still be managing money well into my 90s, like Buffett, I won’t tempt fate by attempting to predict the future. What I do know is that I’ve been blessed with good genes, and I love doing what I do. And now that the Poplar Forest Team is part of Tocqueville, I am able to spend more time doing the parts of the job I love most. I’ve been blessed to work with talented and inherently “good” colleagues as we have strived to deliver market-beating long-term results for our many clients. Thank you for giving us the opportunity to serve you.

With tremendous gratitude,

J. Dale Harvey

June 30, 2025

Click here for Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.