")

Dear Partner,

Barbecue means different things to different people: in Texas, it means brisket; in Kansas City, ribs; in North Carolina, pork shoulder. I remember my first taste of Carolina barbecue like it was yesterday. I was 11 or 12 years old. We’d been living in Virginia for several years, and on the drive south to Myrtle Beach for vacation, we stopped at Bridges BBQ in Shelby, North Carolina, the small town of my birth. That lunch blew me away and kindled a love affair with pit-smoked meat that continues to this day.

In this, the second in my series comparing barbecue to investing, I turn to the Carolinas. When a North Carolinian says BBQ, they are generally referring not just to the cut of meat, but to the way it’s cooked: slowly over the coals of burned hickory. Pulled or chopped, these tender bites of heaven are finished with a sauce that balances out the fattiness of the meat. The sauce is largely comprised of vinegar and pepper in the Eastern parts of the state; but, in the Piedmont, the rolling hills that separate the coast from the Blue Ridge Mountains, the sauce includes ketchup. While the difference of a single ingredient may seem unimportant to folks outside of the Carolinas, for locals it’s a big deal.

Just as good barbecue requires the application of the right sauce to carefully smoked meat, equity investing requires the application of the right valuation metrics to forecasted earnings and free cash flow. And just as the story of North Carolina barbecue is a tale of two tastes, value investing could be said to be a story of two distinct disciplines: Absolute Value and Relative Value. Absolute Value practitioners, like Poplar Forest, generally use valuation metrics that aren’t influenced by changing investor tastes, while Relative Value managers tie valuation to broad market measures like the S&P 500 or the Russell 1000 Value Index. With stock indices looking very richly valued today, Relative Value strategies may leave you invested in less expensive, but still expensive stocks.

I saw the dangers of Relative Value investing first hand in the late 1990s. Tech stocks were all the rage and I remember a colleague trying to convince me to add at least a few of what he considered “cheap” tech stocks to my portfolio to help alleviate the chance of lagging the market. I told him I was sticking to my process of applying absolute valuation metrics to normalized earnings and free cash flow.

Because while a stock trading at 40x earnings may have looked less expensive than its competitor trading at 80x, it was still absolutely expensive. And those valuation multiples proved even more distorted when earnings failed to live up to expectations – in my experience, the sustainability of earnings may be even more important than a stock’s valuation. Back then, I just didn’t see a way to justify the gaudy multiples of the day given the long-term fundamentals of the businesses in question. Especially when, as is the case today, there were ample opportunities to invest in good companies with solid prospects and whose stocks were very reasonably valued in an absolute sense. When the Tech Bubble burst, my approach proved its worth. I was an Absolute Value investor then and I am an Absolute Value investor now. I believe that the Poplar Forest valuation philosophy (the same one I used back then) is particularly compelling in the current environment in which the biggest Growth stocks appear to be distorting many stock indices.

The S&P May be Near an All-time High, But the News Isn’t all Good

With the S&P 500 near all-time high levels, equity investors seem to believe that the Fed has engineered an economic miracle – a recession-avoiding soft landing despite historically aggressive increases in interest rates. There is certainly plenty of data on which the bulls can rest their hopes. For example, the U.S. Bureau of Labor Statistics recently reported that the U.S. economy added a surprisingly robust 272,000 new jobs in May. At just 4.0%, the unemployment rate is still at an historically low level. Consumer spending is generally healthy and consumer credit is behaving well. With inflation coming down, the Fed may soon be cutting interest rates. Equity investors seem to believe that rate cuts will propel stocks higher still.

While I hope the optimistic narrative is correct, I think this is a time for caution, not wanton bullishness. I continue to worry that we are only now starting to see the lagged effect of the Federal Reserve’s interest rate policies. While the unemployment rate is low, it is rising. The number of new job openings is falling. The robust new jobs report for May seems to have been driven by workers taking on second jobs – not a good sign. Initial unemployment claims are low, but also slowly rising. Long-term bond yields have been coming down in recent weeks which suggests that fixed income investors see a slowing economy.

Discrepancies in the economic data make life difficult for all economic forecasters, including those at the Federal Reserve. At this point, the Fed seems most focused on defeating inflation and in my view, its current wait and see approach risks leaving monetary policy too restrictive for too long. The Fed’s most recent statement seems to indicate that it is on hold until at least September. And even when they do get around to cutting rates, it is important to remember that they will likely start slowly and that monetary policy works with a lag. Furthermore, lower rates don’t always propel stocks higher. In seven of the last 12 Fed rate-cutting cycles, stocks fell at least 10% within a year of the first rate cut (four of those declines exceeded 20%). Be careful what you wish for!

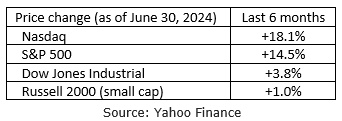

While seemingly daily new record-high closing prices for the S&P 500 and Nasdaq suggest that all is well, prosperity is not widespread. In particular, the big companies in the Dow Jones Index and the small companies captured in the Russell 2000 have struggled this year. This is not what a classic bull market – when stocks of all sizes and shape advance – looks like. Instead, it looks increasingly like a narrow market that could be setting bullish investors up for disappointment. Discrepancies of this magnitude won’t matter as long as the roaring bull market in the shares of companies involved with the buildout of Artificial Intelligence products and services continue, but if they falter, the broad market indices, like the S&P 500, could be in trouble.

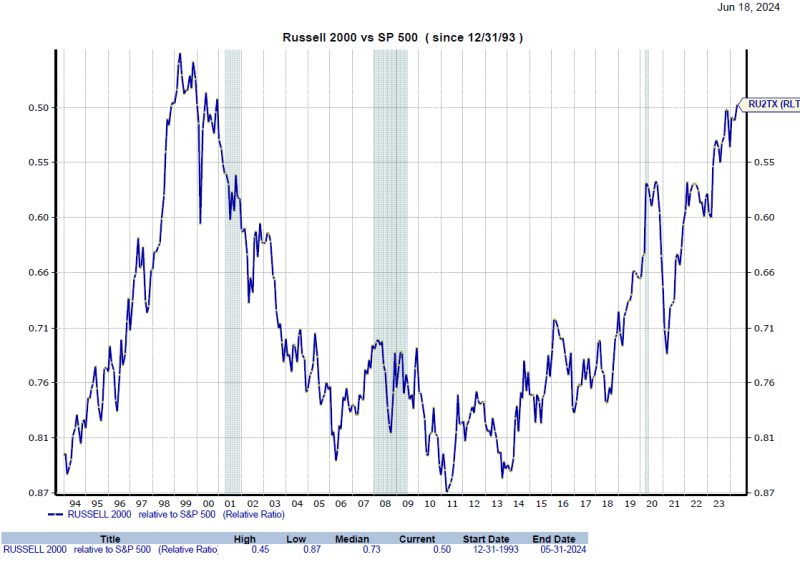

The trend of the biggest companies outperforming small businesses has been in place for close to a decade now. I wonder how much longer this degree of out-performance can continue now that the ratio of Big (the S&P 500) versus Small (Russell 2000) is back to Tech Bubble levels, as you can see below.

Source: Zacks Investment Research

One challenge of the narrow leadership of the biggest Growth companies is that as the Big get bigger, they squeeze what were formally deemed Growth stocks into the Russell 1000 Value index in order to keep the market cap of the two indices equal. While I will save you a detailed explanation of Russell index construction, you may be surprised to learn that when Russell’s index creators divvy up the 1000 largest stocks in the U.S., they include 846 of them in the Russell 1000 Value Index while saying that just 439 deserve a place in the Growth index. And yes, for those of you doing the math in your head, almost 300 companies are in both indices. That means Relative Value managers trying to keep up with Russell’s index may feel forced to own what might have traditionally been deemed Growth stocks. I believe this has the potential to create disappointing outcomes for their clients when the current Growth fever breaks. As Absolute Value managers, we at Poplar Forest believe that we are well positioned for a turning of the tech tide. Evidence in support of this belief would include our performance in 2022, the last time Growth momentum faded.

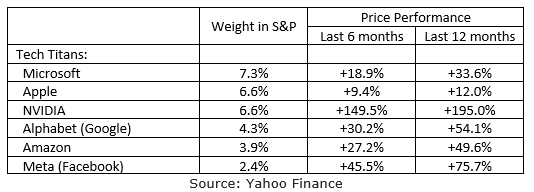

The Big May Strain to Maintain Their Gains

As you can see above, the stock prices of the Tech Titans (my nickname for the Tesla-less Magnificent 7) who are leading the way in the development of artificial intelligence, have been surging. The Tech Titans have beaten everything else, and for good reason – so far, at least, they have delivered superior earnings growth. Still, these six companies now account for 31% of the S&P 500, a level of concentration that I find concerning. Perhaps these winners will keep on winning, but it feels to me like their stock prices already embed very lofty expectations for the future.

My sense of the current enthusiasm for the Tech Titans is that the consensus opinion baked into their respective stock prices is based on the following thinking: First, we are far too early in the adoption curve for artificial intelligence to pick winners and losers, so we should just buy them all and the gains on the ultimate winners will more than offset the losses on the losers. Second, while there is not yet a clear path to monetization of this new technology, companies will surely figure that out later. In the meantime, NVIDIA is the only company with the chips needed to build out AI products and services. There is a gold rush going on, and NVIDIA is the only producer of the picks, shovels, and pans that miners will need to get rich.

What concerns me about this narrative is that it incorporates conflicting thinking about competition. For NVIDIA to keep prospering, it needs lots of customers in competition with one another to support demand for and pricing of its chips. However, if there is massive competition between NVIDIA’s customers, then I wonder if the ultimate profitability of AI products and services will prove disappointing. It reminds me a bit of the early days of video streaming – a product we all fell in love with during the pandemic. In the early days, there was a land grab mentality. Investors basically told companies to go capture as many customers as possible with the idea that they could sort out profitability later. Well, in the case of streaming, it is now later and the profit picture of a market with many competitors has been wildly disappointing (at least for everyone not named Netflix).

AI doesn’t feel like a winner-take-all market that will create massive profits for one or two companies, but instead will likely be an industry comprised of many well-funded and aggressive competitors. If this new technology does indeed lift all boats, and not just a few mega-yachts, then the profit expectations embedded in the Tech Titans’ stock prices may prove overly optimistic. The hard to discern variable is precisely when the current narrative will evolve into something less ebullient. The stocks have such tremendous momentum that they are hard to bet against. Perhaps the hardest part of investing is calling a top in frothy markets, as it is usually only evident in hindsight.

The anointed few don’t always stay anointed, and when the mighty fall, it isn’t pretty. We’ve already seen Tesla fall from grace (down 20% this year). I feel as though I’ve seen this movie before and it rarely ends well. Of course there was the Tech Bubble, not just a bubble in valuation, but also in earnings. The current AI frenzy also reminds me of Energy stocks in the early 1980s and Financials Service companies in 2006-07. Then, as now, the favored stocks in the market accounted for roughly 30% of the S&P. Fundamentals, in terms of earnings growth, free cash flow, and return on capital looked fabulous. The stocks in question didn’t look expensive relative to their fundamentals. The issue was that the fundamentals were not sustainable.

“Cheap” and “Inexpensive” are Not the Same

I believe the key to successful value investing is not in simply identifying statistically cheap stocks, it is about finding companies whose prospects may be under appreciated by other investors. With cheap stocks, you often get what you pay for. We are on the hunt for stocks that are worth more than their current price and are thus inexpensive on the basis of normalized earnings and free cash flow looking three-to-four years in the future. While it may sound counterintuitive, a stock that looks cheap on unsustainably high profits, may actually be expensive, while a high multiple on depressed results may actually be a bargain.

For example, two changes we made to the portfolio in the second quarter were the purchase of Vishay Intertechnology and the liquidation of our investment in Oshkosh Corporation. In the case of Oshkosh, we bought into the company in the spring of 2023. The company had recently finished a difficult year – they earned roughly $3.60 per share in 2022 — and the stock looked “expensive” at more than 20x earnings. We viewed it differently in that we believed earnings were depressed and that a recovery in the business would drive earnings to $10-11 per share in a few years. We believed that if earnings recovered to that degree, then the stock would appreciate materially. It’s been just over a year and the company has already reached the earnings level we projected for 2027. At this point, the stock is selling at what would appear to be a cheap multiple of 10x earnings, but with profits in their core access business at a peak, we worry that their results aren’t sustainable. It may sound counterintuitive, but there was more value in the stock when the P/E ratio was high and less now when it is low. That’s the power of “normalized” earnings.

We used the proceeds from the sale of Oshkosh to invest in Vishay Intertechnology – a producer of semiconductors and related passive components. While artificial intelligence spending may have created a modern-day gold rush for NVIDIA, conditions are far different elsewhere in the semiconductor industry. Companies like Vishay that serve more traditional end markets such as automobiles, consumer electronics, and medical and industrial products, are dealing with excess inventories and depressed profits. As was the case with Oshkosh when we first invested, the stock doesn’t look cheap given its P/E ratio of 29x depressed earnings. However, looking out a few years, we believe the company can earn at least $3 a share and, on that basis, today’s $23 stock price looks inexpensive. And the company’s prospects may prove to be even better – management has a plan to accelerate revenue growth which could drive more margin expansion than we have forecast. If management delivers on its plans, earnings could exceed $5 per share and the valuation may expand beyond the 13x target in our base case analysis.

In addition to swapping our Oshkosh investment into Vishay, we liquidated our position in Wells Fargo and swapped our investment in Phillip Morris International into shares of Kraft Foods. While Wells Fargo is currently doing well, I have lingering concerns that we have not yet seen the full economic impact of an extended period of restrictive monetary policy. If credit costs increase, that stock may struggle. Similarly, Phillip Morris is doing well fundamentally, but with almost all of its profits coming from non-U.S. markets, currency fluctuations have erased almost all of the underlying earnings growth produced by the business. We are concerned that this trend will continue; stagnant earnings and a higher stock price reduced the attractiveness of the investment. Kraft, the well-known food company, has spent the last few years reinvesting in its business after the prior management team cut costs too deeply. The business now appears to be on stronger footing and we believe the market is under-estimating the company’s normalized earnings power. As a result of these transactions, we currently own shares of 29 different companies while having a 5% cash reserve for new investments.

Conclusion – Part of a Balanced Diet

While I’d love to eat good barbecue every day, I know that my long-term health depends on a balanced diet that includes fish and vegetables and fruit. In the same way, I believe that investors’ long-term financial health depends on a balanced portfolio of bonds and stocks, Growth and Value. I worry that given the performance of the biggest Growth stocks, many investor portfolios may have gotten out of balance because the “Value” part of their diet is increasingly made of “Growth” ingredients. In my opinion, this is a good time to review exposures and to perhaps add another helping of Poplar Forest to your plate.

Our portfolio is currently valued at less than 13x earnings as compared to 16x for the Russell Value Index and 22x for the S&P 500. Not only is our portfolio providing absolute value, but we believe it is also exceedingly inexpensive given projected growth in earnings and free cash flow per share of 14% per year over the next three years. I love what we own and our goal is to provide market-beating results whether the economy stays strong and the stock market broadens out to include the type of businesses we own or whether the AI fever breaks and the Tech Titans come back down to earth.

Sincerely,

June 30, 2024

Click here for Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.