")

One of my favorite times of the year is our annual spring trip to the New Orleans Jazz and Heritage Festival, aka JazzFest. Over two weekends, more than 80,000 people gather in front of 13 stages to hear everything from rock to blues, hip hop, swamp funk, zydeco, and – oh yes – jazz. It’s not just the music that lures us; vendors there sell some of the best fried chicken I’ve ever eaten, a delectable cheesy pasta dish called Crawfish Monica, and a pulled pork sandwich I can’t get enough of: Cochon de Lait. Suffice it to say, my taste buds end up as satiated as my ear drums.

Late spring weather in the Big Easy can be unpredictable; over the years, we’ve had everything from breezy perfection to thunderstorms to sweltering heat and humidity. This year, the forecast said a brief shower was due to pass through on Saturday, so as it started to sprinkle, my wife and I stayed put in a prime spot in front of the Festival Stage. One of my favorite local rock bands, the Revivalists, was scheduled for three o’clock, and I knew they were worth the wait. An hour later, after an unrelenting downpour, we were completely soaked under our trash-bag ponchos. And then came the news: the Revivalists had cancelled because of illness. Instead, their spot was filled by a rocking blues artist named Samantha Fish. I have nothing against Fish, and she played a great set, but had I known I wasn’t going to hear the tunes I expected, I would have headed for shelter when the rain started falling.

Judging from conversations I’ve had with financial advisors over the last few months, many of them are experiencing something akin to my soggy JazzFest disappointment. After living through challenging results when value investing was out of favor, these advisors have recently discovered “style drift” at some of the “value” funds they have selected for client accounts. After more than a decade of strong returns from Growth stocks, performance anxiety has led some value managers to re-define what they mean by “value” so as to be able to include companies with higher-growth characteristics in their portfolios. In the last four months, having more growth stocks in a portfolio has produced better performance when compared to investment managers, like Poplar Forest, who stay true to an absolute value investing discipline, but I think it is important for investment professionals to do the job their clients expect. While Growth stocks have become all the rage again in recent months, if that euphoria fades, Value stocks may provide a needed port in the storm.

Drummers Shouldn’t Try to Play Lead Guitar

Imagine buying a ticket to see the Rolling Stones, but ending up at a Taylor Swift show. It’s not that “Swifties” are wrong to love her, it’s more that when you’ve paid good money to see one of the world’s greatest rock bands, you expect to get some satisfaction, not a pop music extravaganza. It’s the same with growth and value funds: they do different jobs for clients.

Calling a fund “value” when, in my opinion, it offers value in name only, is happening more than you might think. When looking at data in Morningstar, you can find several high profile “Value” funds that have repositioned themselves more like a “Core” manager who owns a balance of both growth and value stocks. You might ask: if both options are good, why should we care? Here’s why: Think of “growth” and “value” portfolios like members of a great band: each musician has a role to play. If everyone is playing lead guitar, you won’t have rhythm. If everyone plays drums, there will be no melody. Beautiful music can only be created by talented musicians who work together while playing their designated role.

At Poplar Forest, we understand our role in clients’ diversified portfolios – portfolios that include bonds and stocks, U.S. securities as well as foreign ones, large and small, growth and value. We agree with the observation of Nobel laureate Harry Markowitz: “diversification is the only free lunch in investing.” By owning uncorrelated assets and rebalancing systematically, investors have the potential to improve their risk adjusted returns. A “value” manager suffering from style drift is like a drummer trying to play lead guitar – the client may not get the diversification benefits they expect if their value manager produces results that end up being highly correlated with the S&P 500. In a market that has become increasingly dominated by a handful of huge tech companies, staying true to our absolute Value investment discipline seems particularly imperative today. In 2021 and 2022, that discipline paid off handsomely and I suspect it will do so again when current investor enthusiasms fade.

You won’t see style drift at Poplar Forest. We are dedicated value investors and I’ve been following the same investment process for 27 years now. While some market participants are currently enthused about the growth potential of the biggest tech companies in the world, we are equally excited about a portfolio of smaller and more prosaic companies that is trading at just 12x earnings at a time when the S&P is valued at roughly 20x.

At Poplar Forest, we know that clients have hired us to manage the value sleeve of their portfolio. That is a job that I believe we are particularly good at and is one that we take seriously. We strive to build a portfolio of under-appreciated companies who have the potential to deliver market-beating, long-term returns. We focus on normalized earnings and free cash flow and prefer companies with strong balance sheets, though we are willing to invest in non-Investment Grade-rated businesses if we believe we are being well compensated for their higher risk. During the last quarter, this bottom-up investment process led us to make a new investment in Oshkosh Corporation while liquidating two positions in companies – Perrigo and MillerKnoll – that had the weakest balance sheets in the portfolio.

Oshkosh is an under-earning manufacturer of heavy-duty specialty trucks and access equipment. While the business has some cyclicality, a strong balance sheet and a sales backlog well above historical norms should reduce downside in a recession. We have under-written our investment on an expectation of $9 of earnings per share in 2026, well below management’s recently re-iterated target for $12 of EPS in 2025. We expect a better than hurdle-rate return in our base case and we have very positive optionality should management deliver on their plans.

In the case of Perrigo, the trigger for our exit was the unexpected retirement of the 62-year-old CEO (who was under contract through October 2024). Over the last few years, the company has improved the quality of its operations by favorably settling outstanding tax liabilities while also divesting a low-quality generic drug business and acquiring a growing non-U.S. consumer healthcare business. The future looks bright and that was why we were so surprised by the CEO’s departure. If much of the hard work has now been done, why not stick around to capture the expected rewards? We interpreted his exit as a vote of no confidence and we decided to follow him out the door.

With MillerKnoll, our original investment thesis was predicated on the company realizing cost savings and revenue synergies from the merger of Herman Miller and Knoll – both successful office furniture manufacturers. These deal positives were expected to be augmented by a post-Covid improvement in sales as workers returned to the office. While the company has done a good job controlling costs, we no longer have conviction in the return-to-office aspect of our thesis. The reduced potential for a cyclical recovery in sales, coupled with a stretched balance sheet, resulted in a risk/reward balance that we no longer found compelling.

As a result of our portfolio decisions, we now have investments in 29 different companies as well as a healthy cash position that gives us dry powder to make new investments if a Fed-induced recession offers up bargains in the weeks and months to come.

The Economic Forecast Calls for Rain

“I was born in the rain on the Pontchartrain, underneath the Louisiana moon

I don’t mind the strain of a hurricane, they come around every June

The high black water, a devil’s daughter, she’s hard, she’s cold, and she’s mean

But nobody taught her, it takes a lot of water, to wash away New Orleans.”

from “Hurricane,” by Thom Schuyler, Keith Stegall, and Stewart Harris

Whenever I think of rain and New Orleans, “Hurricane” comes to mind. While the song was first recorded by Levon Helm in 1980, my favorite version was performed by Band of Heathens in 2018. It’s a bluesy song that tells of “the old man down in the (French) Quarter” who is unfazed by a coming hurricane. Of late, most market observers sound like that old man. They say there’s nothing to worry about: a debt ceiling deal was reached, the banking crisis is behind us, inflation is coming down, the Federal Reserve has (at least temporarily) stopped raising interest rates, and if there is to be a recession, it will be mild and earnings need not fall much if at all. On the back of all this good news, stocks, as measured by the S&P 500, rose more than 20% from last October’s low – enough for observers to declare the bear market over and a new bull market underway as of June 8th.

I worry, however, that recent market gains may prove transitory as the economy falls into recession in coming months. The Federal Reserve has aggressively raised interest rates at the same time that money supply has fallen. Monetary policy works with a lag, often a year, and I suspect we will see increasing signs of recession in the near future. This is coming at a time when banks are struggling with the impact of an inverted yield curve and rising credit costs – getting a loan may become increasingly difficult/costly just when companies are most in need of new funding. We are already seeing signs of increased competitive activity when we talk to company management teams and we expect those pressures to intensify as top line growth slows. Earnings for the S&P 500 typically fall at least 15% in a recession and I see no reason to expect anything different this time around. With the S&P trading at roughly 20x earnings, there appears to be little evidence that investors have built a recessionary profit decline into their expectations.

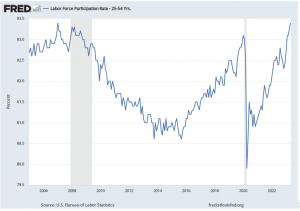

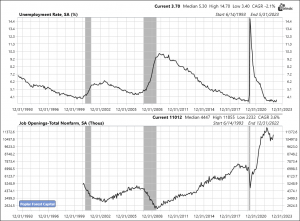

The outlook for corporate profitability also appears to be challenged by a tight labor market with historically low unemployment and an historically high number of job openings (see Appendix for more information). As you can see below, America is basically out of workers (or people willing to work), as evidenced by the high participation rate of the prime age labor force. The U.S. labor force is roughly 167 million and grows 0.5-1.0% a year, or around 1.25 million people annually. In comparison, over the last year, the U.S. economy created over 4 million new jobs. There simply aren’t enough new workers to allow the economy to continue growing at current rates. The balance of power appears to be shifting from employers to employees as evidenced by a 50% increase in labor strikes in 2022. That trend may continue. For example, an authorization to strike recently received 97% approval from Teamsters Union members as negotiations for a new contract with UPS continue. If the Teamsters were to walk out, it would be the biggest work stoppage in U.S. history and a major problem for the U.S. economy.

Unless there is a dramatic change to U.S. immigration policies that would allow more workers to enter the country, companies that want to grow may have to pay higher wages to attract new employees. That will either reduce margins or force firms to raise prices to protect profitability. Wage-driven price increases can lead to the type of persistent inflation the Fed is most worried about. In the long run, AI may be able to help, but in the near term, I believe profit growth may be increasingly difficult to come by until we get some slack in the labor market – and that seems unlikely outside of a recession.

As a result of these macroeconomic forces, investors may be facing two less than ideal outcomes: 1) very low earnings growth and sticky inflation if we avoid a recession or 2) an earnings decline of at least 15% if the Fed keeps tightening monetary policy until it sees real-time signs of recession (much higher initial jobless claims, for instance). Neither of these outcomes seem to be reflected in stock prices today, with the S&P 500 trading at roughly 20x consensus earnings (which could be 15% too high). Suffice it to say, I’m not as sanguine as that old man down in the Quarter.

I’ve lived through my share of economic hurricanes (recessions), though, and I believe that at Poplar Forest, we’ve done a good job of preparing our portfolios for foul weather. We’ve been building an economic contraction into our financial forecasts for more than a year now and, given the increasingly cloudy economic skies, we’ve been particularly focused on the financial strength of the companies in which we invest. I believe the imbedded credit quality of our portfolio is currently higher than at any time since we opened our doors in late 2007; we only have two non-Investment Grade-rated companies (both BB+ – a notch away from Investment Grade) in the portfolio and they total just 5% of our assets. Both these companies have improving financial situations and I expect them to both be upgraded within the next 12 months.

In summary, I believe that we are invested in a great collection of businesses with above average earnings potential driven by margin expansion and the shareholder friendly deployment of free cash flow. Despite this attractive fundamental outlook, the portfolio is valued at just 12x earnings while providing a free cash yield of 6% with roughly half of that free cash flow being paid out as dividends. On top of that, we have a healthy cash cushion that is currently earning at least 5% and that gives us optionality to pick up potential bargains if a recession sends the stock market lower as it did last fall.

In closing, a note on our team. During the second quarter, Nick Wells, who covered consumer and materials companies for us for the last five years, left the firm and we wish him and his family only the best as he pursues new opportunities. As of today (July 3rd), Charlotte Hall is joining Poplar Forest as an analyst after more than seven years with the Capital Group, primarily in a senior analyst role. Charlotte is a Pasadena native who graduated magna cum laude, Phi Beta Kappa from Duke. During her time at Capital, she covered an eclectic group of companies ranging from steel producers to environmental services to data and information services, and U.K. retailers. As part of her analyst responsibilities, she personally managed a roughly $1 billion portfolio of client assets. We are extremely excited to have Charlotte join the team.

Sincerely,

June 30, 2023

APPENDIX – Historically Low Unemployment and Historically High Job Openings

Source: Federal Reserve Bank of St. Louis; U.S. Bureau of Labor Statistics

Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.