")

I’ve always liked to cook, but staying home during the pandemic gave me the chance to up my game. I’ve tried new things (my grill-seared ahi tuna is a hit), honed some old skills (my sourdough bread is better than ever), and also begun reading more about cooking. I loved the 2006 book Heat, in which writer Bill Buford describes learning to cook in Italy. So when my wife heard he had a new book out – Dirt, in which he searches for the secret of French cooking – she bought it for me.

I have a particular fondness for French food and Dirt read like a love story. I devoured it. By the end of its 432 pages, I’d laughed, cried, and added the city of Lyon, where much of the book takes place, to my bucket list. My wife thinks Buford has made my sauces better. But he also taught me something about teamwork.

A French restaurant does not succeed, Buford writes, only because of its Chef de Cuisine, or head chef. Excellence requires a team. In a French kitchen there is the Sous Chef (the head chef’s deputy) and several Chefs de Partie (those who run particular stations like meat or fish or vegetables or desserts). There are behind-the-scenes staff procuring supplies and paying the bills and a front-of-house workforce directly interacting with customers. As I read Dirt, I couldn’t help but think that successful investment firms aren’t so different.

At Poplar Forest, I may be the Head Chef, but I couldn’t do my job without the help of an amazing team: Derek, my Sous Chef; Cathy, Nick, Steve, Phyllis and Gregg our Chefs de Partie; Ryan, Erin, Marla, and Nina, who keep everything running smoothly behind the scenes; and Drew, Chris and Patty who interface with our clients. Many of our team members have been at Poplar Forest for more than a decade; they joined when we had just a handful of patrons, as they believed we were cooking up something special. To the Poplar Forest team: thank you for all that you do for our clients and for putting your trust in me those many years ago!

Good Food Requires Good Ingredients

One of the most frequent questions I’m asked right now is: how long will this value cycle last? I don’t know precisely – nobody does – but the opportunity for outperformance continues to look very large. There is still a wide dispersion in the valuation of “growth” and “value” stocks, and we at Poplar Forest are still finding plenty of interesting new investment ideas. I think the availability of good ideas is a critical measure of how much further we have to go in the value cycle. I remember the difficulty of finding good ideas in 2006-2007 – that was a sign that the 2000-2006 value cycle was nearing its end. If a chef can’t find good ingredients at the farmers market, his or her restaurant’s daily specials are not apt to taste very special.

During the second quarter, we added three new stocks to the portfolio: Allstate, United Therapeutics and Organon & Co. In addition, we have been doing the prep work on a half dozen tasty-looking investment opportunities. If our additional research supports our initial assessments of these businesses, I would expect at least a couple of them to make it onto Poplar Forest’s menu. It feels like we are moving from a macro-driven environment to a “stock pickers’” market – the new ideas that appear most interesting are in a number of different industries. Our investment theses are not driven by a macroeconomic forecast or “risk on/risk off” expectations. We have identified what we believe are mispriced stocks with company specific catalysts for value creation.

During the second quarter, we liquidated our investments in Morgan Stanley, Stanley Black & Decker and ViacomCBS as we believed their respective stock prices adequately reflected, on a risk-adjusted basis, the future we see for each company. Here’s a closer look at the new ingredients we’ve added to the portfolio:

Allstate is the fourth largest writer of auto insurance and the second largest provider of homeowners insurance in America. Until recently, Allstate also offered life insurance and annuities. The stock has long traded at a discount to peers like Progressive (17.3x ‘21E) and Mercury General (16.0x ‘21E). We believe a large portion of the discounted valuation was due to the life insurance and annuities businesses. The disposition of these operations freed up billions of dollars of capital, some of which was used to fund the acquisition of auto and home insurer National General, while also freeing funds for additional share repurchase. We believe the repositioned company will enjoy accelerating growth and that the stock’s P/E ratio (8.6x ‘21E) will expand to a level more in line with its peers.

United Therapeutics was founded in 1996 with the goal of developing life-extending treatments for patients suffering from lung disease. The company has been very successful in serving niches like pulmonary hypertension (excessive blood pressure in the lungs) and is expanding into other end markets and launching new devices to deliver medications to patients. Management believes that they can double the number of patients served over the next three years – an expectation that, if met, could bring a doubling of their revenues and EPS. Despite this impressive growth potential, the shares are currently valued at 12.5x estimated 2021 earnings. In addition, the company boasts a balance sheet with $3.2 billion of cash and investments and just $800 million of debt. If you reduce the stock price by the amount of net cash on the balance sheet, the P/E ratio drops to just 8.5x.

Organon & Co. was spun out of Merck in early June. The company is comprised of a collection of mature products with little or no growth but with substantial cash generation. As is sometimes the case with spinoffs, selling by Merck shareholders who are less interested in the company’s financial profile created what we believe is an extreme valuation dislocation. In the few weeks that the shares have been traded, they have changed hands at less than 5x expected earnings per share. The stock would still be cheap at our target valuation of 7-8x earnings, but such a valuation could see a 40-60% increase in the share price.

Outlook – Value Could Keep Cooking!

While I continue to see a very profitable path forward for value stocks, the stock market never moves in a straight line. Volatility can be our friend as market zigs and zags (which signify shifting data and sentiment) may provide us with opportunities to improve the risk/reward profile of our funds. To put this in context, from 2000-2006, a period of seven consecutive years of value stocks beating growth stocks, the Russell 1000 Value Index produced a 7.8% compound annual return as compared to the -4.9% annualized loss of its Growth sibling. But this massive outperformance wasn’t consistent from one quarter to the next. In fact, out of the 28 quarters in this period of massive outperformance, the Russell Value Index only beat the Growth Index in 17 quarters – just 60% of the time.

With growth stocks having reasserted themselves as interest rates trended lower during the second quarter, some naysayers are already predicting the end of this value cycle. I couldn’t disagree more. For one, I continue to believe that bond yields have separated from reality due to price manipulation on behalf of central banks at home and abroad. Negative real yields will continue to fuel the global economic oven with the benefit being robust earnings growth. This means there should be fewer reasons to pay a premium for earnings growth, as it won’t be scarce. Furthermore, when interest rates do start to normalize, that may put downward pressure on the valuations of the leading growth stocks. In short, value stocks appear to offer competitive earnings growth potential and their valuations can improve as interest rates normalize. That combination may be a powerful wealth creator.

A continuation of the unprecedented, pandemic-induced emergency monetary measures (0% short-term interest rates and the buying of tens of billions of dollars’ worth of bonds every month) is not the course of action I’d vote for if I were on the board of the Federal Reserve, but I don’t get a vote. The Fed has made clear that it is very comfortable with accelerating inflation. Those worried about the risk of higher than expected inflation should keep in mind that, historically, value stocks have done better than growth stocks in periods of increasing inflation. As you can see below in data from a recent Bernstein Research report, i value stocks already have a large gap to close if inflation simply returns to the “normal” levels of the last decade (roughly 2%) and even more upside if inflation accelerates to higher levels.

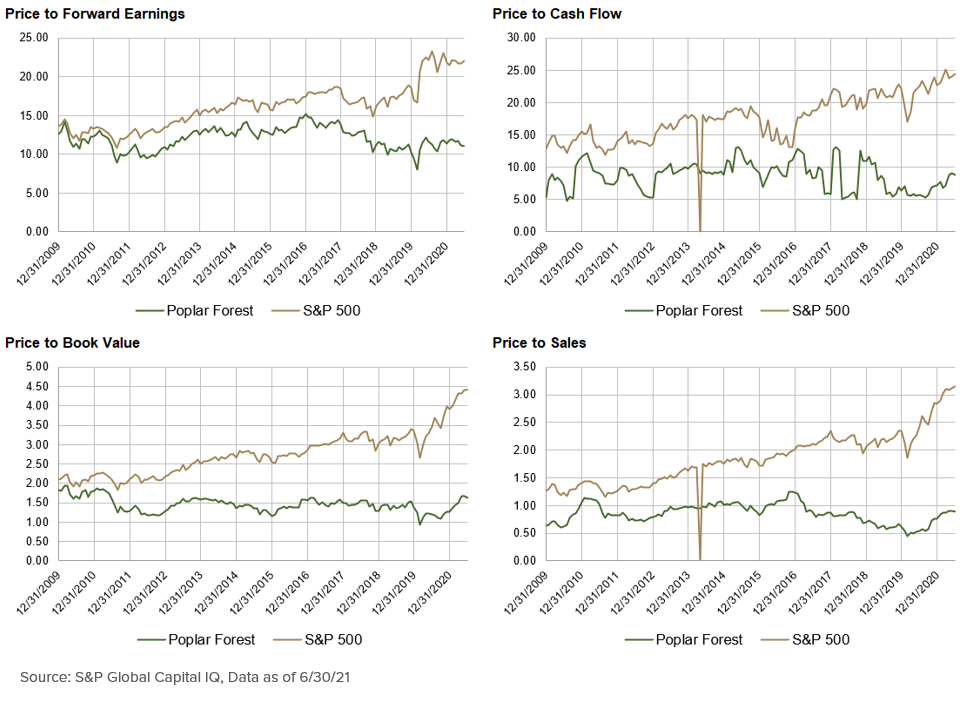

With an economic backdrop that should be positive for value stocks, our portfolio continues to trade at what we believe is an overly discounted level. Consensus earnings estimates for the companies we own have increased by roughly 15% in the last three months and, as a result, the fund’s P/E ratio has fallen to roughly 11.1 times forward expected earnings as of June 30, 2021 (as compared to the S&P 500 at 22.0x and the Russell 1000 Value Index at 17.2x).

As you can see above, by following a recipe that focuses on absolute value, we have produced portfolios that have maintained their value characteristics even as broad measures of the stock market have gotten progressively more expensive. At a time when the S&P is recording all time high prices, we believe these valuation gaps can provide some downside protection should there be an inflation-induced market correction while also providing substantial upside as market valuations normalize. In summary, I continue to be excited about the prospects of our portfolio and about potential additions to our investment menu.

Whether you are enjoying burgers and hot dogs or a fancier repast, I hope you and your family have a healthy and happy Fourth of July and a delicious summer!

Sincerely,

J. Dale Harvey

i www.bernsteinresearch.com; Portfolio Strategy: Strategic Outlook for Factors, and Why They Are Needed in Portfolios; Inigo Fraser-Jenkins, 6/7/2021

Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.