Poplar Forest Analyst Insights: Financials Q&A

In this edition of Analyst Insights, Derek Derman frames the impact of the COVID-19 pandemic on the Financial Services sector, highlights how banks and insurance companies are much stronger now than during the financial crisis, and discusses some of his highest conviction investment ideas.

In this edition of Analyst Insights, Derek Derman frames the impact of the COVID-19 pandemic on the Financial Services sector, highlights how banks and insurance companies are much stronger now than during the financial crisis, and discusses some of his highest conviction investment ideas.

What impact will record low interest rates, increased unemployment, and rising credit losses have on the Financial Services sector?

The Financial Services sector is highly sensitive to economic conditions and the COVID-19 pandemic has caused a severe contraction in GDP. The U.S. is now in a recession and unemployment claims are skyrocketing. The number of out of work Americans is more than 35 million, up from less than 2 million a year ago. Even as states begin to slowly reopen, many consumers are still fearful of getting sick and spending patterns remain depressed. With unemployment growing and continued uncertainty around the timing of effective therapeutics and vaccines, credit losses seem likely to jump higher in the short term. How bad net charge-offs will get is unknown. The pandemic’s duration will greatly influence ultimate loss rates—the longer the crisis the greater the negative impact will be.

If we look back at the 2008-9 financial crisis, bank net charge-offs more than quadrupled to a peak of 2.7% of loans. In the current crisis, unemployment is set to peak at a higher level than what we experienced during the financial crisis. The jobless rate peaked at 10% in 2009, but it’s already much higher today. While we don’t know whether elevated unemployment levels will quickly reverse or persist into 2021, the near-term spike in unemployment implies loan losses could be higher than the 2008-9 financial crisis.

All of this suggests financial service companies are facing tremendous headwinds and we are not surprised by investors’ “sell first” response. Higher unemployment will require greater loan loss provisions that depress earnings. Falling interest rates will also squeeze yields earned on loans. The sector’s earnings in 2020 will be down year-over-year.

With the Financial Services sector being one of the weakest performers this year, do you think investors are over-reacting? If so, what’s causing the misperception?

As just outlined, the Financial Services sector is being pressured on multiple fronts and most investors still have scars from the last downturn which occurred more than a decade ago. It makes sense that the initial sell-off would be severe and that the sector would underperform other less impacted segments of the market.

That said, we believe investors underappreciate the significantly stronger position financial firms are in today compared to the last cycle. The financial services industry has evolved in many ways since the 2008-9 financial crisis. With a strong push from regulators, the financial sector has been preparing itself over the past decade for the next downturn. It has built up capital levels, increased liquidity, and regularly performed severe stress tests on its balance sheet. The difference is already noticeable. Banks are not seeking bailout funds to stave off default. Instead they are providing assistance to the government’s rescue efforts. For example, banks are processing Paycheck Protection Program (PPP) loan applications, funding clients’ liquidity needs, offering forbearance, and waiving fees. And it’s not just banks. Life insurers, who took TARP (Troubled Asset Recovery Program) funds during the financial crisis, are not requesting any assistance in the current crisis.

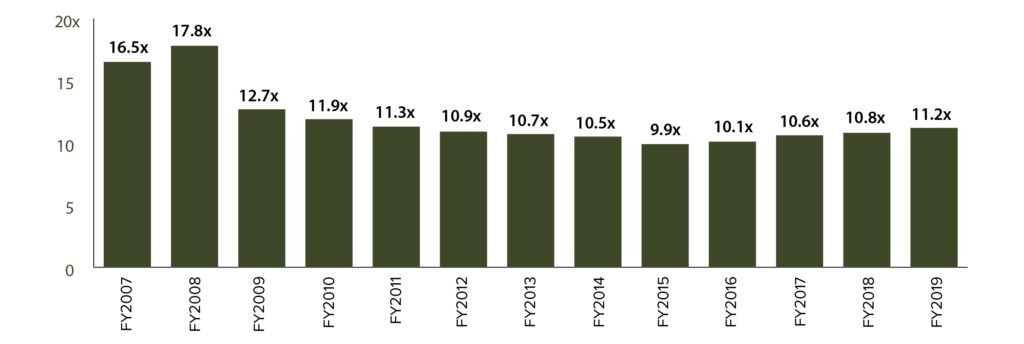

The Assets/Equity ratio, one measure of a bank’s financial leverage, is much lower heading into the current crisis compared to the financial crisis of 2008-9:

*Includes: JPM, C, WFC, BAC, GS and MS; Sources: Capital IQ & Poplar Forest Capital

The economic backdrop is also quite different. In the last crisis, home prices plunged and fears of bank runs were common. So far, home prices are stable to rising and may appreciate further as demand for more spacious quarters intensifies following the virus. Also, no one seems to be stuffing cash in their mattresses. Banks gathered $1.1 trillion in new deposits in 1Q-2020 alone. The stock market is similarly performing much better this time around. During the financial crisis, it took six years for the S&P 500 Index to exceed the prior peak. The strong bounce back from the market lows in late March suggests a much shorter timeframe is possible. With many financial services business lines tied to market values, this is a welcomed change.

Of course, no two downturns are the same and this one has some unique elements. Unlike most recessions, this downturn did not originate from the collapse of excesses somewhere in the market (tech bubble, mortgage bubble, etc.) The economy was posting moderate growth before the virus emerged and most metrics suggested stability ahead. Mandatory shutdowns to control the virus’s spread are what is causing this recession. This crisis is also different because the government is responding forcefully. The Fed has reduced interest rates to near zero and launched multiple programs to ensure financial markets function properly. Policymakers have quickly distributed trillions of aid dollars to help businesses and consumers.

While we don’t know when the health crisis from COVID-19 will end, we believe cyclical sectors such as Financial Services should outperform when it does. This is because lenders must accrue reserves for losses well in advance of actual charge-offs. That means lenders are sure to build loan loss reserves ahead of actual needs. By our estimates, banks will need to build reserves into next year. This pulls profitability down, causing investors to shift their valuation framework from forward earnings to book value. However, once losses near peak levels, investors may shift their price targets back to normalized earnings power which could lead to meaningful upside.

What type of Financial Services companies are likely to outperform over the next 1-3 years?

In downturns, it is typically the strong that get stronger. Weak players are forced to retrench. Those with sturdy capital levels that can manage the more challenging environment and afford to keep investing often gain lasting market share. We expect this crisis to be no different.

One of our current portfolio holdings, Bank of America (BAC) is a company well positioned to come out of the downturn stronger. After struggling mightily during the 2008-9 financial crisis, management has spent years repositioning the company. Management’s goal to lift the bank’s return on equity required streamlining operations, reducing credit risk, fortifying the balance sheet, and investing in digital platforms. The bank has reduced its expenses on an absolute basis every year since 2011. BAC has also shifted the loan mix towards higher credit scoring customers. Heavy investment in digital distribution has allowed the bank to reduce real estate and shift client behavior to lower cost channels. With its digital app, BAC has given consumers greater convenience (a bank branch in their pocket) while saving money and building a competitive advantage over smaller banks. The net result is BAC entered this crisis in a healthy position. It has excess capital on its balance sheet and a high quality loan portfolio. The recession will cause losses to go higher, but it is expected that BAC will gain market share. Early data points suggest this is already happening based on deposits, loans, and capital market activity.

I would also highlight Equitable Holdings (EQH) as a Financial Services company in which we have high conviction. EQH is a life insurer that also got into trouble during the financial crisis when it was owned by AXA Group. It wrote annuities with overly generous benefits. Profitability on these products soured and AXA decided to exit the business. EQH is now a repositioned standalone company. Management has been running off the troubled annuity portfolio, rapidly growing less capital intensive buffered annuities, trimming expenses, and optimizing the general account investment portfolio. The company also owns a controlling stake in AllianceBernstein—the asset manager with more than $576 billion assets under management. The current downturn is pressuring many life insurance peers yet EQH’s hedging program has protected its capital. While others are retrenching, EQH is continuing to invest in the business and executing on its share repurchase program.

Thanks for the insights, Derek.

Let’s Discuss

We’d love to continue the conversation. Please contact Patty Shields (pshields@poplarforestllc.com or 626-304-6045) is you’d like to schedule a call to discuss this or any other topic.

Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.