J. Dale Harvey

Lead Portfolio Manager

Dear Shareholder,

Several years ago, my wife convinced me that a week at a health spa in Mexico was a perfect way to kick off the new year. I was initially skeptical, but on our first visit – after we tucked our phones into tiny spa-issued “sleeping bags” and locked them in our room’s safe — I quickly became a convert. Until then, I hadn’t imagined how restorative it would be to take a break from texts, emails, and the 24-hour news cycle.

That would prove to be just the first of many lessons I was about to learn. Each morning started with a pre-dawn, five-mile hike during which we could watch the sun rise over the desert hills. Meals were healthy and comprised mostly of fresh produce from an amazingly lush and productive 80-acre garden. When we toured the place, we heard that the soil there was primarily clay and decomposed granite – a less than ideal mix for growing vegetables. For decades, though, the ranch team had worked this ground and added compost, drip irrigation, and mulch that helped the soil retain water.

To me, the spa’s garden was proof that hard work could turn seemingly worthless land into an Eden of abundance. And even though I was on vacation, I couldn’t help but think of my team’s approach to contrarian, value investing. It reminded me of the ranch garden in that, then, as now, we start with materials that other investors may view as substandard, but — as this past year’s results demonstrate – fundamental analysis, the hard-won wisdom of experience, and careful stewardship can produce bountiful results!

A Season of Growth and Transition

This wasn’t the first time I’d thought of this analogy. A favorite mentor of mine used to describe portfolio management as akin to gardening. The team must plant new seedlings, then water, fertilize, weed, and prune them before – ultimately – preparing for harvest. The Poplar Forest team has long had a similar process, and in 2025 – the year in which we merged with Tocqueville Asset Management – that process produced particularly rewarding results.

When we announced our deal with Tocqueville in April, we shared our excitement about finding a partner that offered us full autonomy to run our contrarian value strategy while providing enhanced resources in research, trading, and back-office support. To our surprise, a few clients expressed concerns regarding merger integration risk, personnel differences, or whether the move was driven by my plans to retire (I’m not planning to do that any time soon).

As we close the door on 2025, we are proud to have proved that those concerns were unfounded, especially as we look at what we have achieved. The Poplar Forest Partners Fund had an excellent harvest with a total return well in excess of 17% and 15% returns of the S&P 500 and the Russell 1000 Value Index. Not only do these results validate our decision to join Tocqueville, but they demonstrate the value of our idiosyncratic stock selection process. We have more time for investment research, more resources to draw upon, and frankly, we’re having more fun. While the transition required effort, we believe we are now even better positioned to manage client assets for many years to come.

The Coming Growing Season – Rate Cuts and Fiscal Stimulus

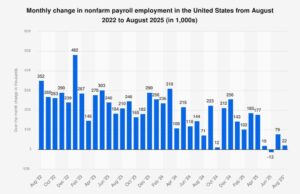

From a fundamental standpoint, the coming year looks promising. The Fed recently cut short-term interest rates for the third time this year, and more reductions appear likely. Furthermore, the stimulative aspects of the “One Big Beautiful Bill” have just begun to impact an economy that has worked through tariff-driven cost increases. This macroeconomic backdrop suggests accelerating growth in coming months. To my mind, the U.S. economy currently looks like a garden suffering from too little water, so the added stimulus may provide irrigation just when it’s needed most. Low-income consumers feel stretched and the job market has been wilting, as you can see below:

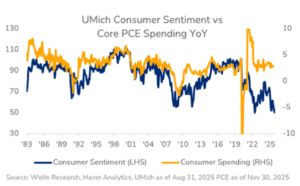

Many investors are currently weighing whether this employment weakness is a “soft patch” driven by transitory factors like tariffs or is instead something more systemic. With consumer spending accounting for 65-70% of U.S. GDP, consumer sentiment is key. One of the most puzzling disconnects this year has been between how people said they feel and how they actually spent. While there is normally a tight correlation between sentiment and spending, that relationship has diverged recently:

People reported feeling discouraged, yet they kept buying things. I suspect this disconnect exists because, as long as people are collecting paychecks, they tend to continue to spend – and maybe even overspend, thanks to easy credit card availability. I worry that consumer spending could weaken substantially in the new year if the jobs picture does not improve.

The crux of the sentiment issue is affordability; prices have increased significantly in recent years, and the cost of living feels high. The challenge reminds me of the quote frequently attributed to Mark Twain: “Everybody talks about the weather, but nobody does anything about it.” If affordability were easy to solve, it wouldn’t be a problem. This is a significant hurdle for policy makers as we approach mid-term elections and I’m curious to see what actions politicians take to win votes.

We are living in what has been described as a “K-shaped” economy where wealthier households continue to spend while everyone else is forced to retrench. In the long run, we believe sustainable economic growth must be broad; otherwise, as a nation we risk increasing populist volatility and the potential for growth-restraining tax increases.

Avoiding Too Much of a Good Thing

In my own gardening, I’ve largely focused on grapes and root vegetables like carrots, garlic and potatoes while my wife Amy handles the tomatoes and leafy greens. Just as in investing, each year presents us with unique challenges. As a quote offered up by Google’s AI tool Gemini aptly puts it:

“The garden is a metaphor for life, and it’s also a laboratory. You have to balance the soil, the water, the sun, and the wind, and if any one of those elements is out of whack, the whole experiment fails.”

— Unknown

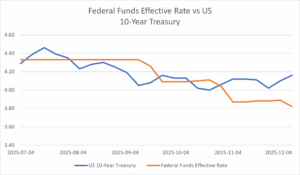

Just as too little water stunts growth, too much fertilizer can produce overly vigorous plants with lots of leaves but little fruit. While as an investor I am watchful of slowing growth, other investors may worry that monetary and fiscal policy may run too “hot” and lead to renewed inflation – especially if a new Fed Chair delivers aggressive rate reductions. It will be hard for the economy to prosper if long-term interest rates increase materially from current levels. We will continue to closely watch 10-year Treasury yields for signs that the Fed is cutting too aggressively. Recently, long-term interest rates increased even as short-term rates fell, suggesting that fixed income investors may be worried that the Fed will go too far, too fast.

Sticking to Our Process

While macroeconomic weather forecasts may change, our team’s investment process remains constant. We build our garden one stock at a time – not based on what might be popular at this weekend’s farmers’ market, but on what we believe will make delicious and well-rounded meals for years to come.

Working at Tocqueville gives us access to a larger “nursery” of ideas and the opportunity to compare notes with other “Experienced Gardners.” We have more intellectual property to support our disciplined investment process focused on normalized earnings and free cash flow. Simply put, we feel we’re now working in more fertile soil.

This year we’ve made seven new investments, including two in the most recent quarter. In late October, we began accumulating shares in International Flavors and Fragrances, a supplier of ingredients to major consumer staples companies like P&G, Nestle, and General Mills. Before we bought it, the stock had fallen more than 50% following an ill-advised acquisition, but we were attracted by a new management team that is focused on deleveraging and streamlining the company’s portfolio of businesses. We believe a final divestment will clean up the company’s balance sheet and leave it focused on three core businesses with strong market positions and attractive returns on capital potential. Additionally, in mid-December we began accumulating shares in a healthcare company that has all the hallmarks of our contrarian investment process. We look forward to sharing more about this investment once the position is fully established.

In Closing – Gratitude and Optimism for the Coming Year

My wife and my annual pilgrimage to the health spa is coming up, and for me, it will be particularly welcome after such a busy year. Our team is now happily settled in at Tocqueville, and integration activities are behind us. We’ve been very impressed with our new Tocqueville colleagues – analysts, portfolio managers, traders, admin, etc. – and we look forward to continuing to work with them in 2026. The talent pool is deep, and the technology infrastructure is impressive. Personally, I’ve loved having more time in our investment garden and I expect to have even more time to do so going forward.

We enter the new year with a portfolio of companies that we believe possess above-average earnings growth potential, yet trade at a discounted valuation of just 13x forward earnings (compared to the S&P at roughly 22x). We are also researching a handful of new ideas that may further improve the risk/reward characteristics of the portfolio. It’s a great time to be a value investor!

I feel truly blessed to work with smart and talented professionals on behalf of all of you – our patient, long-term client partners. Thank you for your partnership, and I wish you a happy, healthy and – if you’ll forgive one more gardening reference – fruitful new year!

Thank you for your continued trust and confidence,

J. Dale Harvey

December 31, 2025

Click here for Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.