")

Dear Partners,

I want to be clear: I have no plans to retire.

I say this because a couple of long-time clients recently asked if our decision to join forces with Tocqueville Asset Management was the first step on my path to retirement. If two people ask, I figure at least 20 are wondering the same thing, so I wanted to address the question up front. I continue to love what I do, and the Tocqueville transaction only makes me more excited about what’s ahead. I believe that a multi-year value cycle is starting, and I’m looking to grow, not contract. So, this is not about me riding off into the sunset. On the contrary, the opposite is true.

In a time of uncertainty that has accompanied a new administration in Washington, I’m particularly pleased to have at our disposal the expanded resources that come with joining Tocqueville. We’ve spent four years getting to know each other, and several months of planning how we will integrate to bring more value to clients. As a result, I could not be more thrilled about our future together. The cultural fit between our firms is remarkable, and given the strength of their administrative and operations team, I will get to spend more time doing what I love: picking stocks and working with clients and prospects. I was blessed to discover my passion for investing at an early age and while I can’t guarantee that I’ll still be working at 94, a la Warren Buffett, this deal has extended my career by many years. Bottom line: I look forward to working on behalf of you and all our clients for a long, long time!

Presidential Cycles – Taking the President at his Word

Three decades ago, I was first exposed to the idea of Presidential Cycles in investing. The premise was that presidents were interested in keeping themselves (and their party) in power. With that thought in mind, the first policies they would pursue after inauguration were the more painful ones. The sooner that hard and difficult work was out of the way, the reasoning went, the sooner a new administration would benefit from the fruits of those actions and recovery would increase their odds of re-election.

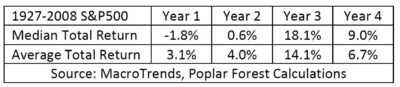

I’m not enough of a historian to know the year-by-year efforts of each president, but prior to the Global Financial Crisis in 2008-09, the data supported this eat-your-vegetables-first contention. Starting in 1927, stocks produced a pattern of weak returns early in presidential terms, with strong results after mid-term elections, especially in year three:

As a parent, I know the wisdom of having kids eat their vegetables before getting dessert. Unfortunately, in more recent times, politicians have acted less parentally and more like the visiting uncle who hands out free ice cream without worrying about leafy greens. As a result, we have a massive Federal budget deficit and a dangerously high level of debt relative to the size of the economy. President Trump says he aims to fix these problems, but also many more including illegal immigration, the trade deficit, and the wars in Ukraine and Gaza. While most presidents focus on a single key issue right out of the gate, President Trump seems to be trying to solve all our problems at the same time. Given all that is being attempted, there are apt to be bumps in the road.

The Investor’s Dilemma – Is A Bird in the Hand Worth Two in the Bush?

The proverb “a bird in the hand is worth two in the bush” dates back to medieval times, when a falconer had to decide whether or not to release his bird in the hopes that it would return with captured prey. It takes a lot of time and hard work to train a falcon and losing one is a major setback, so the decision to send a raptor out hunting is not one to be taken lightly. In the same way, investing is about managing uncertainty — do I invest $100 of my hard-earned savings today for the promise of $200 in the future? While it has been said that investors hate uncertainty, uncertainty is inherent in investing. I think the real issue is that investors often demand higher prospective returns (via a lower purchase price) to compensate for higher perceived risk. That appears to be happening now. At one point in March, the S&P 500 had fallen just over 10% from all-time high levels reached in February – a so-called market “correction.” Since then, stocks have recaptured some of those losses, but it feels like investors are on edge and increasingly interested in risk management. If investors start to price-in the effects of a full-blown recession, history suggests stocks could see a peak-to-trough decline of 20% or more.

For those who are regular readers of my letters, you know that I have been particularly focused on risk management in recent years. While I am inherently an optimist, the risk/reward ratio of stocks in the S&P 500 has reminded me of the late 1990s when Growth stocks were also market leaders; and as was the case then, there are still a number of Value stocks that we believe offer attractive upside potential and discounted valuations. The late-90s bull market was followed by a seven-year run of Value stock out-performance from 2000-06, and I believe the stage is set for a similar cycle in coming years. One thing I learned in the 2000-06 cycle is that carefully chosen value stocks have the potential to rise in price even when the broad market averages fall. That has certainly been the case through the first three months of 2025.

When it comes to managing portfolios in a period of uncertainty, such as the one we are currently living in, I believe that it may be more prudent to secure the proverbial bird in one’s hand as opposed to releasing it in hopes of getting two in the future. As a practical matter, a research process that focuses on free cash flow and discounted valuations seems especially relevant in today’s environment. By free cash flow, I mean the amount of money a company has after collecting from customers, paying its bills, and investing for the future. Over the last twelve months, our portfolio companies have generated free cash flow equal to more than 10% of their market value (a 10% “free cash yield”). Suffice it to say, more free cash flow is better than less, provided sufficient funds are reinvested in the business – especially if the future appears as uncertain as it does today. Among the questions fueling that uncertainty:

- What’s going to happen with tariffs and potential trade wars?

- Will mass deportations continue (and with what impact on the supply of workers)?

- What about DOGE and other efforts to balance the budget? Will entitlements be spared?

- Can he really bring peace to Ukraine and Gaza?

- And what about Canada, Panama, and Greenland?

- The list goes on…

Bullish investors read today’s news and focus on the promise of reduced regulation, lower budget deficits, and AI-led productivity increases that they hope can drive double-digit earnings growth and dramatically higher stock prices in the future. The economy is reasonably strong, they tell themselves, unemployment is low, inflation is retreating, and the Federal Reserve will soon cut short-term interest rates again. Optimistic investors are buying the dip as they only see blue skies ahead.

Bears, on the other hand, say shrinking the Federal budget deficit by firing tens of thousands of government workers and cancelling contracts will likely lead to recession. Consumers and businesses are already pulling back due to the uncertainty of what may prove to be inflationary tariffs. They worry about a “stagflationary” environment of slow economic growth and stubbornly high prices which will prevent the Fed from lowering interest rates. Bears acknowledge that addressing America’s many challenges could lead to a brighter future, but they worry about costs of addressing those problems.

While my team and I are cognizant of both arguments, our focus remains on our bottom-up investment process, which seeks to identify out-of-favor and under-appreciated companies in which we’d be happy to be invested for many years. We compare our assessment of the upside in a bullish scenario against the downside of a more bearish outcome. Our goal is to invest only when we believe the odds are stacked in our favor. That doesn’t mean we get every investment right, but if we can be right more often than wrong in situations where upside substantially exceeds downside, then we may be able to deliver compelling long-term investment results.

In the short term, this focus on risk as compared to potential reward has proven especially helpful. In the first three months of the year, Value stocks have beaten Growth stocks and our portfolio has beaten both. Value stocks are demonstrating their historic role of providing downside protection and if current uncertainties continue, value stocks may continue to be ascendant. With our portfolio valued at 13x earnings, as compared to the S&P 500 at 20x, we may be particularly well positioned for continued outperformance. And like a medieval falconer, while we are prepared to go hunting for value if the market sells off, for now we are focused on the birds in our hands. Whether or not we get new opportunities may depend on how the economy responds to the many policies emanating from the White House.

Looking Ahead

The next three months are momentous ones for me, I’ll celebrate my 60th birthday and the 45th anniversary of my first stock purchases. In those 45 years, I’ve lived through five bear markets and six bull markets that included countless corrections of 10-20% along the way. In short, this isn’t my first rodeo. I’ve watched investors panic when conditions get difficult and I’ve been fortunate to be able to execute on Warren Buffet’s admonition to be fearful when others are greedy and greedy when others are fearful. To that end, our team has been developing a shopping list of companies we would like to invest in if prices get to levels that suggest limited downside and the potential for market-beating long-term returns.

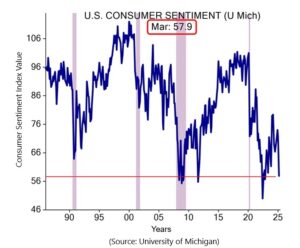

The opportunity set will largely be driven by the potential for recession. In a recession, earnings generally decline and valuations often fall which may create an even larger array of investment opportunities. Recessions are hard to predict and the general belief right now is that one will be avoided. I sincerely hope the consensus is right, but I worry that the fear of a recession can become self-fulfilling. If tariff uncertainty stays high, businesses may continue to hold back on hiring. If consumer confidence stays low, consumer spending could fall, especially for those government workers who fear for their jobs. As you can see below, consumer sentiment appears dangerously depressed right now (grey bars indicate recessions).

Like sugar-addicted spoiled children, many market participants have generally believed that while the President talked about hard-to-swallow policies, like tariffs, on the campaign trail, he didn’t really mean it. Surely, these people hoped, the threat of tariffs were a negotiating ploy – not future policy. Surely, tax cuts would come first. Bolstering these hopes was the fact that, in his first term, President Trump referred relentlessly to the stock market as a measure of his accomplishments. That led to a widespread belief that in his second term, a negative stock market reaction would act as a sort of check-and-balance, causing the President to back down.

The President isn’t following the script most investors expected. In fact, the President’s actions have largely followed the promises he made on the campaign trail. And when the market sold off in conjunction with the instigation of tariffs, the President didn’t flinch. He has stated, and his Treasury Secretary has confirmed, that the administration is not worried about recession or downside in the stock market. Team Trump is focused on solving long-standing problems like the deficit, and they say that if that means life gets harder in the short-term, so be it – long-term gain is worth some short-term pain. This approach may yet prove to be more bark than bite, but for now, I think it is prudent to take the President at his word. Given all the President is attempting to do, and the short-term hits to the economy those actions could entail, I continue to believe that caution and prudence are warranted.

Given all the uncertainty, the critical question my team and I ask ourselves is whether or not we are being adequately compensated for the risks we see. Our investment team is carefully examining the potential for long-term gains and short-term downside for a growing collection of businesses that we fundamentally like. We have established downside price targets that could occur in a recession, and if panicked investors drive prices down to those levels, we are prepared to take advantage of their fear.

Given the attractiveness of our existing investments, new ideas face a particularly high hurdle to make it into our portfolios. Over the next three years, the companies we already own are expected to grow earnings at a rate comparable to the S&P 500, yet our portfolio has a price-to-earnings ratio at about a 35% discount to the S&P. In addition to comparable earnings growth, our companies currently offer dividend yields that are twice that of the S&P 500.

Yes, investment risks look elevated today, but given the dynamics of our portfolio companies, we believe we are being handsomely rewarded for taking on that risk. It is a mindset that has served us well so far this year. Since the start of the year, Growth stocks are down 10%, the S&P 500 has fallen 4% and Value stocks have gained 2%, and the Poplar Forest Partners Fund is up 6%. As we’ve told people in the past, we believe that when Value beats Growth, we can beat both — that is exactly what has happened so far this year.

For 17 1/2 years, our clients have entrusted the Poplar Forest team with their wealth. We take that responsibility seriously and we will continue to strive to be worthy of your trust. Joining forces with Tocqueville gives us even more tools to deliver on our ambitions. I am excited to work every day with talented professionals who share a common goal of delivering market-beating long-term results while helping to mitigate against downside risk. I continue to have more than 90% of my investable assets in the funds that we manage and I will do my level best to continue to deliver many more years of shared investment success for all of us.

With gratitude,

J. Dale Harvey

March 31, 2025

Click here for Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.