")

Dear Partner,

A few years ago, after telling the kids we were spending News Years night at a friend’s house in Santa Monica, we ended up coming home early. You can imagine the scene. The driveway: full of cars. The house: full of kids. There’s music and dancing and someone is running around in their underwear. We turned on the lights, turned down the music and then made sure everyone got home safe. Happily, our house emerged a little messy, but without any breakage. Who knows what we’d have found if we’d gotten home at noon the next day as opposed to 1:30 in the morning?

The current investment environment reminds me of that New Year’s Eve. After avoiding a recession despite historically aggressive monetary tightening by the Federal Reserve, the 2023 bull market extended into 2024 with Growth stocks continuing to lead the way. The Russell 1000 Growth Index was up 38% in 2024 and a whopping 86% over the last two years as compared to one year 25% return, and two year 53% return for the S&P 500.

Stocks have been buoyed by the avoidance of recession, solid economic growth, and expectations of market-friendly policies from the incoming Trump administration. The Fed has been cutting short-term interest rates as inflation has come down, though it is still well above their 2% target. Despite that, the Fed has still penciled in another two rate cuts in 2025. Economically speaking, everything appears to be going great. In fact, the U.S. economy is the envy of most countries in the developed world, many of whom are fighting to avoid recession. It’s no wonder that U.S. stocks are besting their non-U.S. peers.

Advocating for prudence and caution in a roaring bull market is akin to turning down the stereo at a house party. Historically, the Federal Reserve could be relied on to call a halt to raucous reveling. William McChesney Martin, Fed Chairman from 1951-1970, argued that central bankers are “in the position of the chaperone who has ordered the punch bowl removed just when the party was really warming up.” In contrast, the current Federal Reserve seems prepared to order more tequila shots for everyone with further reductions in short-term interest rates. And investors want more! I’m reminded of former Citigroup CEO Chuck Price, who said in 2007: “When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance. We’re still dancing.”

The Bull Market is Going Strong, What Could Possibly Go Wrong?

Under President Trump, the regulatory burden on business is apt to go down and there is talk of lower tax rates, though given the state of the Federal budget, that potential seems limited. In 2017, the Federal budget deficit was 3.6% of GDP as opposed to roughly 6% today – but then again, maybe deficits don’t matter to investors any more. With S&P 500 earnings having doubled over the last eight years, the impact of lower corporate tax rates will likely be far more modest than during Trump 1. Earnings for the S&P 500 may be boosted by about $5 per share (a 2% bump) if corporate tax rates are cut to 18% — and $10 per share (a 4% bump) at a 15% rate – according to analysts at Wolfe Research. Both of those potential outcomes pale in comparison to the $18 benefit (a 14% bump) from tax rate reduction in President Trump’s first term.

Still, investors are optimistic, and I’m not alone in seeing signs of speculative excess. For example, bitcoin prices have more than doubled this year. MicroStrategy: “the world’s first and largest Bitcoin Treasury Company,” has used leverage to bet on rising bitcoin prices and investors have cheered them on. The stock is up 350% this year. And if that isn’t enough, Tuttle Capital Management offers an ETF that aims to deliver twice the daily return of MicroStrategy. The Wall Street Journal recently reported that Levered ETFs that aim to double or triple the daily returns of an index, or even a single stock, have grown 46% this year to $137 billion.

But leverage on top of leverage rarely ends well. At times like this, I am reminded of Warren Buffet’s admonition “to be fearful when others are greedy and to be greedy only when others are fearful.” Notably, Buffett’s Berkshire Hathaway has been selling down large investments in Apple and Bank of America while adding to an already sizeable cash hoard. I don’t know that Buffett is predicting a market crash, but given the starting valuation for stocks (S&P at 25x expected earnings in 2024 and nearly 23x expected in 2025 that embed an historically robust 15% earnings growth rate), future returns are apt to be muted. Perhaps he’s been talking to strategists at Goldman Sachs or Bank of America who predict returns of 3% and 1% respectively for the S&P over the coming decade. Low-risk Treasury bonds and bills with yields in excess of 4% look awfully compelling in comparison.

There is a general view that because Trump’s first term saw above-average gains right up until COVID, the same will be true the second time around. I sincerely hope that is the case, but I worry because the starting conditions are less friendly in valuation terms, interest rates are higher, and some announced policy positions may not be as market friendly as investors hope. For example, healthcare and packaged food companies already appear to be in the new administration’s dog house. In addition, mass deportations and tariffs could be inflationary. If inflation heats back up, interest rates may head higher.

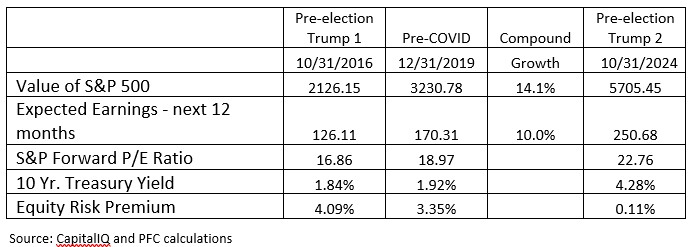

As you can see below, valuations just ahead of Election Day 2024 were 35% higher than they were in 2016 while interest rates have more than doubled. The implied Risk Premium in stocks is far lower than it was at the start of President Trump’s first term. They may not be getting paid to take equity market risk, but investors keep plowing money into the stock market. Stocks as a percentage of Household wealth is at a record high.

Investors have rosy expectations for the future – solid earnings growth, lower inflation and interest rates, pro-business policies at home, and calm geopolitics abroad. As long as this narrative continues to hold, investors can party like its 1999. But with the S&P 500 trading at almost 23x expected 2025 earnings, there is virtually no margin of safety should the future disappoint. A margin of safety is a bit like the homeowners policy you want in case something bad happens when your kids throw a party while you’re out of town.

Value Investing in a Bull Market

Our Contrarian approach to value investing involves identifying companies where investors have what we believe are unduly low expectations about the future. Low expectations, in the form of valuation, can play the role of that homeowner’s policy: you may enjoy lots of upside if things go right, but limited downside if the future turns out to be less rosy than expected. With our portfolio being valued at just 13x earnings, the equity risk premium reflected in our stocks is more than 4% as compared to the S&P basically at breakeven.

We are continuing to invest cautiously, not just because of the speculative fervor reflected in leveraged bets on AI and bitcoin, but also because of the warning signs we see in the most economically sensitive industries. Whether it is commodity chemicals, steel, or transportation, stock price performance in these industries suggest softer economic conditions than is implied with the S&P 500 at all-time high levels. Some of this is a function of weak economic activity outside the U.S., but it bears watching. In addition, the farm economy is quite soft, and higher insurance premiums and interest rates have created affordability problems for big ticket items like cars and homes. If the share prices of stocks in these areas of the market get down to levels that we believe are consistent with past recessions, we may increase our exposure.

Healthcare and food companies, two areas highlighted earlier in this letter, would have historically looked like safe bets — a place to hide for someone worried about weakening economic activity — but both industries are under attack from a new administration that pledges to “Make America Healthy Again.” I’m all for better health, but I’m not convinced that Team RFK is on the right track with the reforms he wants to push. The opportunity set being presented in healthcare is increasingly attractive and our team is spending a lot of time looking for the best bargains in the sector.

I believe that above average long-term results require a different-than-average portfolio. And being different than average sometimes puts you on the wrong side of short-term investment themes. As contrarians, at Poplar Forest we often look to buy in when other investors are selling out over concerns that we believe are short-term in nature.

In my opinion, for the investor looking to generate truly outstanding long-term results, staying true to an investment discipline is imperative, especially when it appears unfashionable in the short term. A recent report from Wellington Management supports this view. Their work demonstrated that more than half of investment managers with top 10% results over a decade had spent three years in the bottom quartile of their peer group with close to a quarter of them spending five of the ten years in the bottom quartile. To be the best, you have to be willing to look like the worst, at least some of the time.

In an environment in which investors are enamored with AI and bitcoin, our prosaic portfolio may not provide scintillating cocktail party conversation, but at 13x earnings with projected growth of more than 13% a year for the next three years, I think our portfolio is something to talk about! And we continue to find what we believe are compelling new investment ideas that I believe enhance the risk/reward ratio of the portfolio.

During the fourth quarter, we made an initial investment into a distribution company serving both consumer and industrial end markets. We are particularly excited about the growth prospects for the industrial side of their business. The stock is valued at less than 15x earnings with a better than 3% dividend yield, while their closest peers trade at more than 20x earnings. We are looking for signs of improvement from what has been a stagnant industrial economy before adding to the position. I know this company well; I first invested in it in the late 1990s – another two-tier market in which investors were drawn to the promise of new technology as opposed to old-line industrial profit – to fantasy for the future over free cash flow.

It’s no fun to be out-of-sync with the broad market, but I’ve been there before. Market cycles come and go and throughout them, I’ve stayed true to a consistent investment process for more than three decades now — 16 years at the Capital Group and more than 17 at Poplar Forest. I plan to keep doing what I love for as long as I can (94-year-old Warren Buffett is still going strong!) as I fervently believe our approach to Contrarian Value investing can deliver market-beating, long-term returns.

In the roaring bull market that has seen valuations climb to historically high levels, our commitment to Absolute Value Investing has left us a bit behind the broad market averages in the short-term. But like the tortoise racing the hare in Aesop’s fable, I believe we will end up celebrating in the investing marathon Winner’s Circle. I expect music and dancing and maybe even a few tequila shots.

I wish you all a healthy and prosperous New Year!

Sincerely,

J. Dale Harvey

December 31, 2024

Click here for Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.