")

Dear Partner,

Back in 1962, a British guitar player named Brian Jones wasn’t sure what to call his new band. Before the band’s first gig, though, he had to decide. While on the phone with the owner of the venue, Jones looked down and saw an album — The Best of Muddy Waters – laying on the floor. Track Five on side one was “The Rollin’ Stones Blues.” In that instant, the Rollin’ Stones (who would only later add a final “g” to become “Rolling”) were born.

Mick Jagger claims that the first album he ever bought was by Waters, the legendary Mississippi-born blues master. So you can understand why Jagger quickly hit it off with Keith Richards who once said, “If you don’t know the blues, there’s no point in picking up the guitar and playing rock’n’roll or any other form of popular music.” In this, the last of four quarterly letters in which I’ve linked investing and music, I’m sharing my inspiration from these two men who continue to produce great music at 80 years of age. Plus, I’m incredibly excited, and already have tickets, to see them live this spring!

The Rolling Stones have been playing blues-influenced rock’n’roll longer than I’ve been alive. Their recent album, Hackney Diamonds, is in my opinion their best work in many, many years. In the more than six decades since the band was formed, music has seen countless genres come and go from disco and new wave, to punk rock and grunge, and through it all, the Stones have kept doing what they do best, unwavering in the face of changing tastes.

I believe that value investing is as timeless as The Rolling Stones. Warren Buffett has been practicing it unceasingly since 1958. He met Charlie Munger a year later and this investment duo produced decades of outstanding investment results for their clients – in particular, the shareholders of Berkshire Hathaway. That Buffett (age 93) and Munger (age 99 when he passed away in late November) continued their unrivaled success while working well into their nineties is yet another inspiration for me.

Along the way, Buffett and Munger lived through several periods when value investing was left for dead including the Nifty Fifty period (in the 1960s), the New Economy era (in the late 1990s), and what I’ll call the New Economy Redux (in recent years) when investors focused largely on the leading growth stocks (Apple, Amazon, Alphabet, Meta, Microsoft, Nvidia and Tesla). Though at times, Berkshire looked terribly out of step with short-term market trends, Warren and Charlie kept at it with the belief that their strategy of buying stock in under-appreciated companies with sound fundamentals (revenues, earnings and free cash flow), would ultimately win out over trying to constantly adjust to the shifting winds of investor enthusiasm. As Buffett put it in a 1987 letter to shareholders, “In the short run, the market is a voting machine but in the long run, it is a weighing machine.”

Selectivity – The Key to Success

“You can’t always get what you want

But if you try sometimes, well, you might find

You get what you need”

From “You Can’t Always Get What You Want”

Over the years, Buffett and Munger have been unusually selective in making new investments. They have been price-sensitive, and have tended to be most active in times of stock market distress; otherwise, they’ve been happy doing nothing. As Munger once put it: “Lots of hardship will come, and you gotta handle it well by soldiering through. And… a few rare opportunities will come. You got to learn how to recognize them when they come and not make that too minor of a trip to the pie counter when the opportunity is available.”

At Poplar Forest, we’re a bit more active than Berkshire, but also far more selective than many other fund management companies. In my experience, many mutual funds have 50 to 100 or more investments and a portfolio turnover rate of 50-100% per year. At the low end of those ranges — say a 50-stock portfolio with 50% turnover — fund managers need to identify at least 25 new ideas a year, while at the high end of the range they may be making 100 new investments annually. I think truly great ideas are far scarcer than that.

At Poplar Forest, we will typically examine 75 potential investments a year. Of course, we want them to all be great ideas, but we only need 6 to 8 of them to emerge from our rigorous research process with a “Buy” rating. We generally only own our 30 best ideas and we tend to hold each of those investments for three or four years on average. This structure allows us to be very picky.

During calendar 2023, we made just six new investments, with one of those in the fourth quarter. In late October, we bought an initial stake in Sun Communities, a real estate company that owns manufactured home sites, marinas and RV parks. The idea was championed by my partner and co-manager, Derek Derman, who has helped expand my investment horizons just as Munger did for Buffett. When we got involved with Sun, the stock had fallen almost 50% from its old high on concerns about higher interest rates and challenges with a business they purchased in England. On the latter point, we think the problems will prove temporary and that the fundamental outlook for the business is good given the company’s ability to raise prices every year and its business model with very high incremental margins on those new revenues.

The stock market, as measured by the S&P 500, ended 2023 at close to all-time high levels due to investors’ optimistic outlook for continued economic growth and falling interest rates in 2024. With stocks near their highs, finding great new ideas at the right prices has become more challenging. That said, we have identified a number of potential investments that we may be interested in making if shifting sentiment gives us an opportunity. With monetary policy still exceedingly tight, we believe investors may be disappointed by economic growth in the coming year. I have a hard time imagining the Fed aggressively lowering interest rates unless they see real economic weakness, and that is a scenario in which earnings could prove disappointing — stock prices often fall when companies produce disappointing earnings.

Given all that, I’m pleased to say that we are currently invested in 30 companies that we believe offer compelling ratios of reward to risk regardless of whether we see continued growth or an economic slowdown in 2024. We also have a cash position equal to roughly 5% of assets. Because of the macroeconomic risks we see, we are going to remain highly selective in making new investments. Furthermore, cash investments currently yield about 5% — admittedly below our 15% hurdle rate, but far higher than we’ve received in more than a decade. In effect, the potential opportunity cost of being selective is lower today than it has been since the Global Financial Crisis – cash is not trash!

Free Cash Flow is King

“The best things in life are free

But you can keep ‘em for the birds and bees

Now give me money (that’s what I want).”

From “Money”

I’ve been reading Berkshire Hathaway annual reports since I was in college, and one of the earliest lessons I learned from Warren and Charlie was to spend more time focusing on individual company fundamentals and less time on macroeconomics. Macroeconomics can’t be ignored, but I think it is all but impossible to develop an investing edge in predicting variables like employment and inflation. (The Governors of the Federal Reserve are supposed to be at the top of their field and nonetheless, their forecasting track record is terrible.)

When evaluating investments, we start with the knowledge that the economy will have bad years and great ones. We want businesses that can survive economic storms and also thrive when the sun shines. When we look at individual businesses, we focus on those in-between years when things are neither great nor horrible – what we refer to as “normal” conditions.

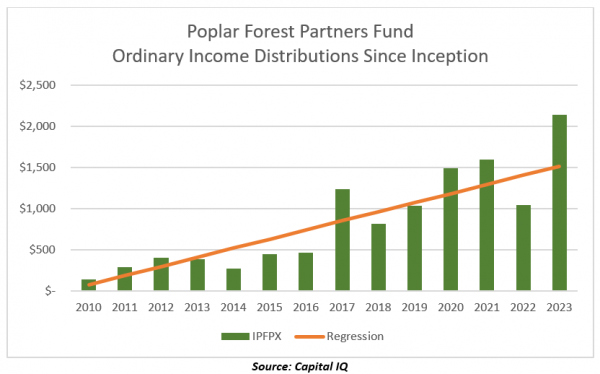

And like The Rolling Stones, we focus on the money – more specifically, the free cash flow that our companies generate. Free cash flow is the money that a company has left over after paying all its bills and investing for growth. We particularly like businesses that consistently generate free cash flow in good years, bad years, and all the years in between. We like it even more when that free cash flow grows and when it is returned to shareholders in the form of dividends and share repurchases. The cash that companies pay out in dividends flows back to you in the form of an annual ordinary income distribution from the mutual fund.

As you can see below, for our clients who invested with us when we launched the Poplar Forest Partners mutual fund in 2010, and who reinvested their dividend and capital gains distributions, we’ve been able to deliver a growing stream of income over time. The common stock dividends paid out by the companies in our portfolio, and returned to you, have increased at a compound rate of more than 25% per year since the inception of the mutual fund for those clients who reinvested all their dividends.

As we look to the future, I believe we are well positioned to continue the trends illustrated above. Over the last twelve months, the companies in which we are invested have generated free cash flow equal to 6.5% of their value (also known as a “free cash yield”). Furthermore, our forecasts suggest that those free cash flows may grow by roughly 12% per year over the next three years. Combining a 6.5% free cash yield with potential for double digit growth of those free cash flows makes for an incredibly compelling investment opportunity, in my opinion, and yet another reason for us to be selective when evaluating new investments ideas.

Focusing on companies that consistently generate free cash flow and return it to shareholders allows us to follow another Buffett/Munger tenet: stay within your circle of competence. During 2023, investors’ attention seemed focused on companies that are currently perceived to be winners in the burgeoning field of Artificial Intelligence or AI. While I expect AI to provide years of productivity improvements across the economy, trying to determine which companies will be the winners of the race is beyond my circle of competence. I think back to the early days of the internet when America Online was deemed a winner; today, AOL is all but irrelevant. Poplar Forest may miss out on some big gains in AI stocks, but we think that by sticking to our disciplined approach to value investing, we will be winners in the end.

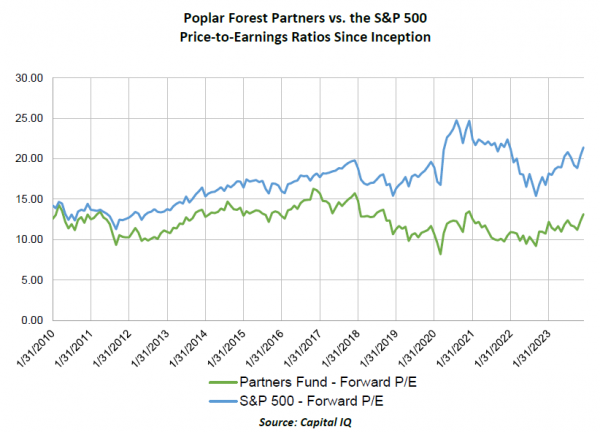

The hardest part of a value investor’s job is having the patience to wait for the market to gain an appreciation for the values inherent in a portfolio like ours. While the S&P 500 has gotten increasingly expensive over the years, we have stuck to our discipline and believe that we offer compelling absolute value in an expensive world. As you can see in the chart above, the Price-to-Earnings (P/E) ratio on our portfolio is lower than it was when we launched the fund back in December 2009 while the P/E ratio for the S&P 500 is far higher.

A New Investment Paradigm – At a Minimum, the Headwinds Appear to be Abating

“When the whole wide world’s against you, and you’re standing in the rain,

And you want someone beside you to pull you up again,

When the whole wide world’s against you and life’s got you on the run,

And you think the party is over, but it’s only just, only just begun”

From “Whole Wide World”

For value investors, the period between the Global Financial Crisis and the onset of Covid felt a lot like standing in the rain – like the whole wide world was against us. During this rainstorm, the Russell 1000 Growth Index beat the Russell 1000 Value Index by almost 6.5% per year. While that was a difficult period to live through, I believe the Covid Crisis unleashed a new investment paradigm – Growth stocks are no longer trouncing Value shares as they did from 2007-2020. In fact, as you can see on the graph below, relative to the Growth Index, Value stocks bottomed around August 31, 2020. Since then, that relative bottom has been tested twice and in late November, the Russell 1000 Value Index appears to have made what technicians would call a triple bottom and at a level that preceded handsome gains in the past. When you add in the higher dividend yields that tend to accompany value stocks, they have outperformed their Growth siblings for more than three years now. While I’m hopeful that this triple bottom will mark a long-term base off of which Value stocks can move to higher relative highs, at a minimum, it feels as if the headwinds we had to face for 13 years have abated. In a world without headwinds, I believe we can do quite well.

Value Beat Growth by 12% per year from 1999-2006,

Growth Beat Value by 6.5% per year from 2007-2020;

Something Different Has Been Going on Since Covid

Source: Intrinsic Research

Source: Intrinsic Research

In the last three calendar years, Growth and Value stocks have produced roughly comparable returns (8.6% for Russell 1000 Growth ETF versus 9.0% for Russell 1000 Value ETF), yet we have done much better with a three-year annualized return of 13.4%. We’ve also beaten the S&P 500 by almost 4% per year. We are often asked when Value will start to outperform – my answer: Value is already outperforming! Given the inherent value I see in our portfolio today, and to paraphrase the Stones, while some may think the Value party is over, I believe it has only just begun!

On behalf of everyone here at Poplar Forest, we wish you all a Happy, Healthy and Prosperous New Year.

Sincerely,

December 31, 2023

Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.