Dear Partner,

I celebrated New Year’s Eve at home with my wife. Thanks to COVID-19, the guest list was short: just the two of us. It was a quiet night, but I was perfectly happy. I’ve never understood the fuss people make about New Year’s. When I was a kid, my favorite end-of-year celebrations occurred when my parents went out to a party and I’d get to stay up with my Grandmother eating cheese curls and watching Dick Clark do his thing. With the exception of maybe twice – a 1984 shindig that coincided with the University of Virginia’s first bowl game and a ringing in of the new century in 1999 – no New Year’s Eve has ever bested those cheese curls. New Year’s extravaganzas rarely live up to the hype.

Outsized expectations are at the root of this problem. In popular culture, New Year’s Eve has been built up to be supposedly the best night of everyone’s year. The pressure is on to look better, feel better, and have more fun than on any of the 364 preceding nights. When expectations are that high, anything less than extraordinary is a disappointment. Good is a letdown if you were expecting great. But the opposite is also true. While the ball dropping in Times Square may get the TV coverage, I have far more fond memories of backyard barbecues and other every-day get togethers with friends that turned out to be special. Low (or even average) expectations create the potential for positive surprise.

Value investing could also be called “low expectations” investing. The goal is to identify and invest in companies that deliver better than expected results while avoiding those which may disappoint. As a result, at Poplar Forest we tend to avoid the stock market equivalent of a New Year’s black tie bash because, too often, reality fails to live up to what’s promised. As investors, we use valuation as a tool in trying to understand the expectations embedded in a stock price. A high price relative to current free cash flow, earnings, revenues or assets implies lots of growth while low multiples suggest the opposite. The most important job for our investment team is to identify situations where embedded expectations are unreasonably low while avoiding stocks that are cheap for good reason (aka value traps). Cheap stocks can stay cheap unless fundamentals turn out to be better than expected. In contrast, the “great” company that merely ends up being “good” often generates disappointing results for its shareholders – just like so many New Year’s Eves.

Growth vs. Value – Divergent Expectations

In the last three months, COVID vaccines have been approved and inoculations have begun. Contrary to some predictions, the election season was riot-free; what emerged was a seemingly investor-friendly balance of power in D.C. With Congress passing additional fiscal stimulus and the Federal Reserve continuing its low interest rate policies, investors now expect a rapid economic recovery and record earnings in 2021 as an increasingly vaccinated populous gets back to normal behavior patterns. At the end of 2020, this powerful combination of factors led to a dramatic recovery in stock prices with the S&P 500 achieving a new, all-time high in December. Though the fourth quarter saw a dramatic recovery in value stocks, the Growth/Value performance gap over the last 12 months was still exceedingly wide (Russell 1000 Growth Index +38% vs. Russell 1000 Value Index +3%). As a result, value stocks continue to reflect historically low expectations relative to growth stocks.

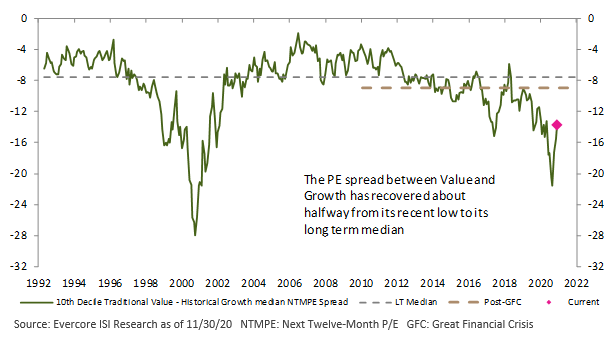

As you can see in the graph below, the cheapest stocks in the market are trading at a roughly 14-point discount to growth stocks as compared to an historic spread of roughly 8 points. The biggest driver of this increased spread is higher growth stock valuations that reflect exceedingly positive expectations for future results. That said, as long as the Fed keeps liquidity flowing, growth stock investors may continue to party like its 1999.

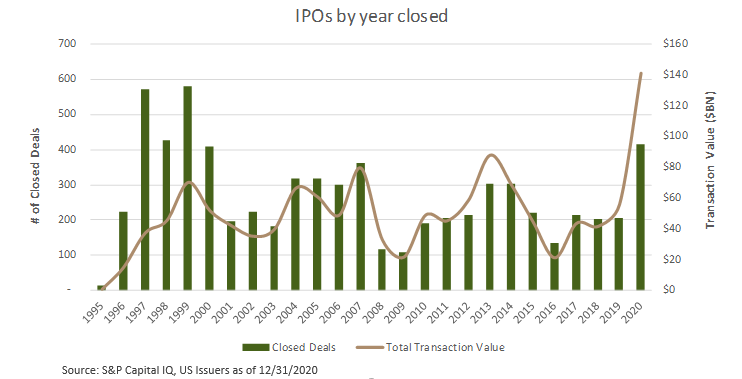

The Fed is doing all it can to support economic growth with easy money policies that have benefitted Wall Street far more than Main Street. A massive pool of liquidity has been looking for a home and has most recently settled on the newest batch of disruptive businesses now making their way into the public markets. Despite the pandemic, 2020 has set a new record for the amount of money raised in initial public offerings. While there haven’t been as many deals as we saw back in the tech bubble in 1999, the amount raised has dwarfed prior peaks.

It has been amazing to watch some of these companies, most recently Door Dash, go public at valuations measured in the tens of billions of dollars while the underlying businesses, in many cases, have little or no earnings. Investors in these deals are simply not concerned about current results. Instead, they are focused on the long-term potential they see in these companies as measured by TAM, or Total Addressable Market. The thinking goes, spend like crazy now to capture as much of the TAM as quickly as you can and only worry about profits after you’ve captured the market. It is an approach that Jeff Bezos used to make himself and Amazon’s investors rich. The strategy can work, but investors appear to be embedding some very rosy expectations for the future in their valuation of many of these companies. While some of these companies will likely live up to the excitement, the ratio of risk to reward doesn’t look compelling to me.

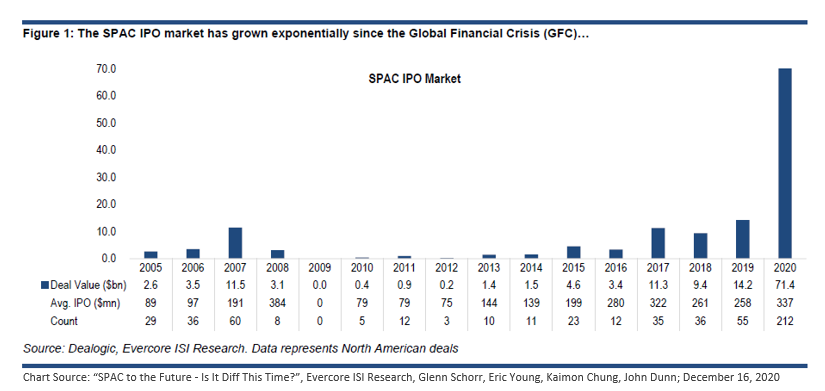

What most concerns me about the current public offering boom is the enormous amount of money raised by SPACs (Special Purpose Acquisition Companies). SPACs are created to collect money from investors with the intention of using those funds to acquire a business, generally in a targeted industry (like clean energy, for example). This can be an easier route to the public market for private companies as, in exchange for a hefty fee, the SPAC sponsor does all the paperwork and marketing to raise the money. For the investor, this type of situation is the ultimate speculation: you make the investment before you know anything about the company you’ll actually end up owning. You are effectively giving the sponsor of the SPAC a blank check to go buy something on your behalf. To me, buying into a SPAC is like spending a lot of money to take a blind date to a fancy New Year’s Eve Ball. Admittedly, I met my wife on a blind date, but how often does that happen?

I simply can’t imagine investing my money before understanding the business I was financing. At Poplar Forest, we carefully examine how the companies we invest in make money. We analyze their sales, earnings, cash flow, assets and liabilities, generally looking back at least a decade. We want to understand their competitive position and plans for growth and capital investment. We want to be up to speed on their cycles and normalized profitability. Finally, we are particularly focused on buying at a price that is low relative to our view of the company’s normalized earnings and free cash flow. We believe that valuation is a key determinant of long-term investment returns.

These days, a lot of money is invested without considering valuation. The most glaring example of this is Tesla. Don’t get me wrong; all my Tesla-driving friends can attest to how wonderful the cars are. Elon Musk is a genius and a great salesman. While Tesla doesn’t fit our approach to investing, I can certainly understand why so many have been drawn to the stock. Tesla shares had been particularly strong in this year’s growth dominated market, rising from $83 on 2019’s New Year’s Eve to $408 in mid-November 2020. Then a committee at Dow Jones decided it was time to add Tesla to the S&P 500 Index, AFTER the stock had already appreciated 388% in less than a year. Tesla was finally added to the S&P 500 because, for the first time since coming public in June 2010, it had finally strung together four quarters of net income.

Being added to an index generally does not do anything to increase a company’s sales, earnings or free cash flow, but in today’s index-driven world, it nevertheless can cause an increase in the stock price. In Tesla’s case, the stock has risen from $408 on the 16th of November, when the S&P inclusion decision was announced, to $695 (up 70%!) on December 18, the final trading day before the stock was actually added to the index. With roughly 950 million outstanding shares, the stock price appreciation added more than $272 billion to Tesla’s valuation. As a comparison, the total enterprise value (debt + equity) of General Motors is $178 billion while Ford is worth $194 billion. While Tesla’s stock price may continue to climb, the expectations baked into the stock price today seem excessive to me. Tesla is the sixth biggest stock in the S&P – more valuable than every public company in America except for Apple, Microsoft, Amazon, Facebook and Alphabet (Google). Twenty-one years may have passed since the tech bubble, but the market’s structure seems eerily similar.

Value Stocks – Still Very Muted Expectations

Amidst the hoopla over Door Dash, SPACs and Tesla, value stocks started to shine in the last three months of the year with the Russell 1000 Value Index outperforming the Russell 1000 Growth Index by 5% (Value +16.25% vs Growth +11.39%). Our portfolios beat both indices. Despite these very positive results, Growth still handily beat Value for the year. As a result, Value stocks continue to offer what we believe are muted expectations and, as a result, a much more attractive ratio of reward versus risk.

Throughout 2020, market volatility continued to present us with what we believe are very attractive investment opportunities and we had an unusually active year of portfolio management. Twelve new companies joined our portfolio this year as compared to a normal year when we might make six to eight new investments. Two of the new holdings are the result of mergers that closed early in the fourth quarter: Chevron’s all stock acquisition of Noble Energy and Morgan Stanley’s deal for E*TRADE Financial. In the fourth quarter, we also actively initiated investments in Citigroup, Curtis Wright and National Fuel Gas while liquidating positions in Bank of America, Baker Hughes, Kroger and SVB Financial Group.

Citigroup has historically produced disappointing results and the stock, at roughly 70% of book value, is priced as if the situation will never be remedied. While we understand the bear argument, we are optimistic that new CEO Jane Fraser will bring fresh thinking to the top job when she takes the reins in February. Our analysis suggests the company should be able to earn $10 a share in a few years, and the stock is trading at roughly 6x our assessment of normalized earnings. If the stock simply gets back to its historic valuation of 10x, we could make 65-70% while also collecting a 3.5% dividend yield.

Curtis Wright is a mid-cap company that participates in several different industrial sectors. We believe earnings can grow to $10-11 a share over the next few years based on cyclical recovery in the company’s end markets and underlying mid-single digit core growth. The stock is trading at around 11x normalized earnings as compared to its historic valuation of roughly 16x, thus implying potential upside of 45-50%.

National Fuel Gas is a mid-cap company that produces, processes, transports and delivers natural gas to customers in the northeastern U.S. During 2020, the company bought Shell’s natural gas properties in the Marcellus at what we considered a very attractive price. The acquisition, plus underlying growth in the company’s mid-stream and transportation segments, should lead to normalized earnings of at least $4.50 a share and potentially much more if natural gas prices rise. The stock is trading at around 9x normalized earnings as compared to its historic valuation in excess of 17x, thus implying potential upside of 85-90% augmented by a 4.3% dividend yield.

These three new investments join 29 existing holdings that we feel also offer particularly good value. As of 12/31/2020, our portfolio was valued at less than 10x actual 2019 (pre-COVID) earnings. We believe 2019 is a good estimation of normalized (post-vaccination) earnings given that we don’t own any businesses that may have been permanently impaired by the pandemic (for example, airlines, hotel chains or cruise ship operators). Many of our businesses are more mature than the average company in the S&P 500 and, as a result, they have historically been valued at a 25% discount to the S&P. With the S&P 500 trading at 23x 2019 earnings, the historic 25% discount would imply a P/E ratio of 17x for our portfolio – more than 70% higher than where it is trading today! On both an absolute and relative basis, our stocks appear to embed decidedly pessimistic expectations, while our analysis suggests a far brighter future.

Outlook – Interest Rates a Key Variable to Watch

I’ve been surprised by the magnitude of recovery in stock prices this year. Despite the pandemic, the S&P 500 produced a better than 18% total return in 2020 on the back of low interest rates and exceptional results from growth stocks (as noted, the Russell 1000 Growth Index gained more than 38%). Over the last decade, the S&P 500 traded at roughly 15.5x forecast earnings while today it trades at 22x (40% higher). Either the outlook for future growth is much better than it has been historically (unlikely), or investors are willing to pay higher multiples because interest rates are so low (more likely).

What I find troubling is a consensus opinion, as implied by stock prices, that the economy will get back to normal sometime in 2021, but that interest rates won’t return to pre-pandemic levels for years. With the Federal Reserve appearing more politically motivated than at any time in my investing career, perhaps the Central Bank will do politicians’ bidding, but at some point, interest rates seem destined to return to more normal levels. That said, the stock market seems likely to keep appreciating as long as the Fed continues to target faster economic growth and higher inflation with easy money policies. As the old adage goes: Don’t Fight the Fed!

In an environment that seems to be growing increasingly risky for investors, I continue to believe that a portfolio of carefully chosen and attractively priced value stocks can provide positive absolute returns in coming years regardless of what happens to the S&P 500. Though we see a future that may be even brighter, the Wall Street consensus forecast for the companies in which we’re invested is for long-term earnings growth of 7% a year. On top of that, our companies are currently paying dividends equal to roughly 3% of their current market value. This combination of growth and dividend payments suggests an attractive potential return absent any change in valuation, yet our portfolios trade at less than 12x forecast, but still depressed, 2021 earnings. At a time that growth stock investors are shrugging off the potential for increased competition, regulation, and/or anti-trust investigations, we think our portfolios of underappreciated investments are particularly compelling. The fourth quarter saw decidedly improved investment sentiment towards the types of businesses we favor, and I continue to believe the stage is set for years of market beating results from our portfolios.

While all of our New Year’s observances were likely more subdued than in the past, I suspect that each and every one of us was enthusiastically cheering the end of what was an immensely challenging year. I hope you and your families are all healthy, and all of us at Poplar Forest wish you and yours a decidedly better year in 2021!

Sincerely,

J. Dale Harvey

Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.