To My Partners,

I’m pleased to report that after a couple lean years, 2016 was decidedly better for Poplar Forest. The Partners Fund was up 26.24%, the more conservative Cornerstone Fund returned 18.87% and the mid- cap focused Outliers Fund gained 10.57%. While both the Partners and Cornerstone funds handily beat the market, Outliers lagged a bit. After reflecting on the results of the Outliers Fund over the last few years, we decided to make a change: I will be joining Steve as a co-manager of the Fund in a structure similar to what Derek and I have used for the Cornerstone Fund since its inception two years ago. Steve discusses this change in more detail in his commentary, which you will find on pages 12-14 of the full downloadable report.

While we are obviously pleased with our 2016 results, I would urge you – as always — to focus on our long term results. Our contrarian approach to investing usually leaves us positioned quite differently than the broad market and that often means our investment returns are decidedly different than the broad market averages – some years, like 2016, are quite a bit better and others are worse. I suspect that will be the case going forward as our investment process is built on normalized earnings and free cash flow looking out three to five years; sometimes we have to live with weak short term performance in order to position ourselves for market-beating long term returns.

After such a strong year in 2016, you may be wondering if we’re heading into a weak period – I don’t think so. I believe the market has transitioned away from a focus on monetary policy as a salve for disappointingly slow economic growth to a more optimistic mindset. While investment programs that focused on quality, low volatility and high dividend yields were winning approaches in 2009-2015, I believe that 2016 was the first of at least a handful of years in which value oriented strategies, like those we employ at Poplar Forest, will be market leaders.

Though the recovery from the bursting of the housing bubble in 2008 has been slow, the U.S. economy appears to be on much sounder footing with unemployment now below 5% and wage growth starting to show signs of life. While much attention, rightfully, has been paid to the outcome of the recent presidential election, I think it is important to note that the economy was strengthening well before Election Day. For example, in the third quarter, the U.S. economy grew at a rate of roughly 3%, and worries of persistently low inflation and economic stagnation had already begun to be replaced with a growing confidence that the economy is in a self-sustaining mode that will allow the Federal Reserve to begin the process of bringing interest rates back to more normal levels (a Fed Funds rate of 3%).

An environment in which the U.S. economy is running steadily on its own is likely to see an additional boost from new leadership in Washington. We’re optimistic about the potential benefits of regulatory reform and tax relief and believe that the post-election rally has not fully reflected the upside potentially accruing from anticipated changes in these areas.

The Trump Plan – Can We Afford It All?

Like an old-time politician promising a chicken in every pot, Donald Trump the candidate talked of plans for regulatory reform, lower taxes, more defense spending and a $1 trillion plan to improve American infrastructure. For investors in stocks, these plans are all very bullish. Reduced regulation should mean lower costs. Lower corporate taxes could lead to higher profits (perhaps 5-10% higher earnings for the S&P 500®). More defense spending will mean work and higher income for defense contractors. Spending $1 trillion on infrastructure means more jobs and new business opportunities for companies that build roads, bridges, airports and water and power systems. What’s not to like? If all this comes to pass, the stock market seems likely to rise by much more than the 5% increase we’ve seen in the S&P 500® since Election Day.

In addition to expecting much higher stock prices, I’d love to pay less in taxes each year. And as someone who drives in snarled LA traffic and who travels on commercial airliners for work and pleasure, I can attest to the need for improvements in the nation’s infrastructure. I have an easy time imagining the projects that need to be undertaken; I am less clear on how these projects are to be funded.

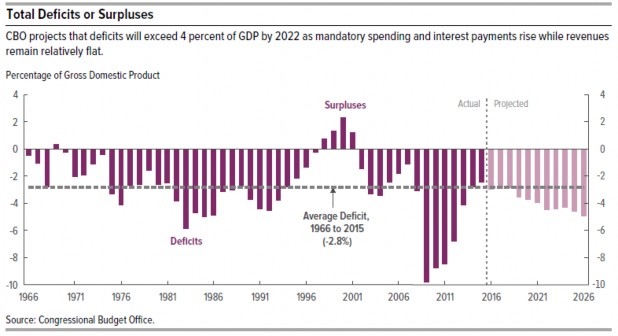

As you can see in the graph above, while the Federal budget deficit improved dramatically in the recovery of recent years, mandatory spending programs and interest payments are projected to drive the excess of spending over revenues to around 5% of GDP over the next decade. I am quite curious to see how a Republican-led Congress responds to the push for lower taxes and more defense and infrastructure spending. Perhaps we’ll simply borrow the money to do all these wonderful things and the deficit will grow to an even larger share of GDP. If that’s the case, then corporate earnings will likely be much higher than investors currently expect. On the other hand, the bond market could be in for a very difficult period as interest rates might head higher and at a faster rate than many people expect.

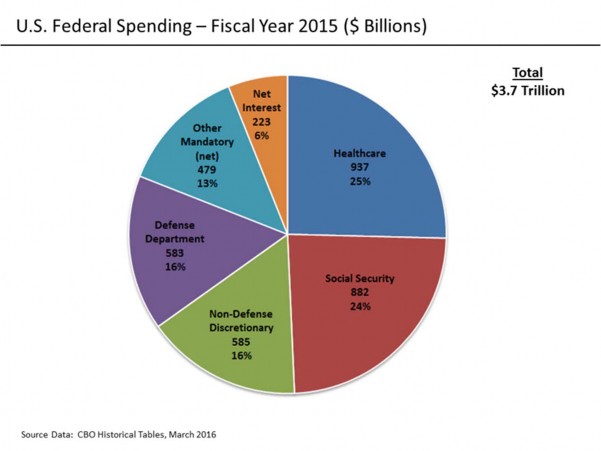

One approach to addressing the potential for a growing deficit would be to make cutbacks in other areas, but with non-defense discretionary spending equal to just 16% of outlays, there doesn’t seem to be enough room to cut. If Congress says no to a bigger federal budget, then investors may end up being disappointed. Candidate Trump’s $1 trillion infrastructure plan used the words “deficit neutral.” Perhaps I simply suffer from a lack of imagination with respect to the funding of his plan. As the old saying goes, maybe we’ll be able to have our cake and eat it too.

If we assume the powers that be can come up with the money, what impact will all this fiscal stimulus have on an economy that’s already doing ok? I worry most about the impact on the labor market given that we’re already running below 5% unemployment. There is certainly potential for some workers to re- enter the workforce and for other workers to shift from part-time to full-time, but Candidate Trump made clear he wanted to create more jobs for American workers and I worry that wages may have to rise much more than expected to get everything done. Inflation has not been a concern for years and I think far too many investors have not taken steps to protect their purchasing power if prices start to rise at a faster pace. At Poplar Forest, we have been focused on protecting purchasing power for some time now and I believe our portfolios are well positioned if inflation starts to come in ahead of expectations.

Though it would likely make for a very exciting couple years for stocks, I worry that doing everything Candidate Trump promised as soon as possible – pursuing regulatory reform and cutting taxes while

ramping up defense and infrastructure spending – is too much in a short period of time. If it were up to me, I would start planning for a big infrastructure program now so that when the next recession inevitably comes, we’ll have “shovel ready” projects that can be funded at a time more appropriate for fiscal stimulus. After eight years of easy money policies, the Federal Reserve has very little monetary dry powder to use in a recession and I see no reason to also use what little capacity we have for fiscal stimulus at a time when the economy is doing okay. Can’t we save our money for a rainy day?

Staying Attentive to Downside Risk

As it turns out, no one in Congress has asked for my opinion on the subject of fiscal stimulus and I suspect that Congress will likely strive to give us everything they think we want whether it is prudent or not in the long term – they want to be reelected after all! As a result, I think the most likely outcome is a very strong equity market for the next couple years with continued minor corrections along the way (please see Appendix). I think all the pieces are in place for the bull market that started in the depths of the financial crisis to reach much higher levels. Unfortunately, the advance I expect is likely to sow the seeds for a future bear market.

For the last eight years, I have believed that U.S. business conditions were better than generally perceived. We saw plenty of bargains in the market and we have held very little cash during the entire period. Despite rampant worry on the part of many investors, stocks, as measured by the S&P 500®, increased in price at a rate of 11.6% per year from their starting level at Dec. 31, 2008. Dividends have added a couple percentage points to stocks’ total return and those who have stayed invested in equities over this period must surely have smiles on their faces.

In recent months, we have felt the consensus opinion start to move in our direction. Perhaps the slowly improving economy has enhanced investors’ risk tolerance, possibly it’s the election, or maybe a review of the return from stocks has raised investor confidence. We are starting to hear reports that investors are beginning to sell bond funds and shift money to stocks. This would reverse multi-year trends and, if it continues, would suggest much more possible upside for stocks.

At some point, perhaps several years from now, the consensus opinion about equities will become too bullish. When we see conditions headed that way, we expect to have a more defensively positioned portfolio that may potentially provide downside protection in the next bear market. While the next bear market seems years away, we’ve begun to think about what steps we’d need to take. The signposts we’ll be watching for include:

- The shape of the yield curve – a flat curve suggests danger

- Valuation – we’ll start to worry if stocks start to trade at 20 times forward earnings

- Funds flow – if investors appear to be pouring huge sums into the stock market, watch out!

- Excesses – we’ll be on the lookout for excess in the economy that might create problems (like housing in 2007 or tech stocks valuations in 1999)

- Opportunities – if we can’t find enough individual equities that meet our 15% return hurdle, we are likely to raise cash

For now, all these indicators look supportive of our positive outlook and we believe that it is too early to worry. That said, and given our three to five year investment time horizon, we are now building a future recession into our base case forecasts for the companies in which we are investing. It seems likely that we’ll have to deal with a recession at some point in the next five years and we want to be as comfortable as possible that the companies in which we invest will do okay in a weak economic environment. We believe that investing in financially strong companies when they are out of favor can produce market- beating returns when times are good while also potentially providing downside protection when recession hits.

Patience – Thank you!

Long-term, contrarian value investing requires patience. Having client partners who share our long-term orientation allows us to buy stocks that sometimes produce weak results in the early stages of the investment. Having confidence that our partners will stick with us in difficult times allows us to pursue an approach to investing that we believe can produce market-beating results in the long run. Relative to the S&P 500®, 2016 is the best year we’ve had since starting Poplar Forest in 2007. The seeds for this year’s strong results were sown in 2014 and 2015 and I’m confident that we are only just starting to enjoy the fruits of our labors in those lean years. Thank you for your confidence in Poplar Forest and for investing alongside us in the Poplar Forest Partners, Cornerstone and Outliers funds.

I hope you all had a wonderful holiday season and I look forward to reporting to you again after we’ve seen what our new President and Congress accomplish in the early days of the new administration.

J. Dale Harvey

January 2, 2017

Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.