")

With COVID having become endemic, 2022 was the year we all dared to take much-delayed summer vacations. For me, that meant heading to the beach in North Carolina. You may wonder: doesn’t he live in California? I do, and while I’ve surely enjoyed many an hour looking out at the Pacific, the view of the Atlantic from the Carolina coast feels like heaven to me. When I was a kid, our family vacation was most often a week or two in a rented condo in Myrtle Beach, S.C. – and I loved just about every minute of it: body surfing and beach walks, hours at the arcade and all the fresh shrimp we could eat.

The only things I don’t remember fondly were the occasional hurricane warnings. When the warnings came, we’d nervously watch the news each evening for reports on the path of storms that might be headed our way. Those storms usually stayed out at sea and our vacations were uninterrupted, but in 1998, the first time I’d taken my own kids to Myrtle Beach, our family was forced to evacuate in advance of Hurricane Bonnie. The weather looked almost placid as we packed to leave, but 24 hours later, Bonnie came ashore as a category 2 storm that killed several people and caused a half billion dollars of damage.

Hurricane season in the Atlantic typically runs from June to November. According to the National Weather Service, a hurricane is a “tropical cyclone with maximum sustained winds of 74 mph (64 knots) or higher.” These cyclones are created when masses of warm air collide with cool air over warm ocean water. Warm water and warm air are key ingredients, but it is that collision with cooler air that produces the wind, rain and thunderstorms that make hurricanes so destructive.

I’ve been thinking about hurricanes lately as I’ve been evaluating the potential impact of a recession on our portfolio. Just as hurricanes can cause damage to coastal property, recessions can harm investor portfolios as a shrinking economy sends corporate profits lower. With memories of the Category 5 calamity of the Global Financial Crisis (the “GFC” in 2008-09), it is no wonder that the risk of recession is top of mind for many investors today.

First and foremost, I do not believe that we are currently in a recession; quite the contrary – the economy is as warm as the water in the tropics. Corporate margins are robust and earnings have continued to grow. The employment picture is rosy with low initial claims for unemployment and roughly two job openings for every one person looking for work. Basically, fiscal stimulus and accommodative monetary policy did such a good job offsetting COVID-induced weakness that strong demand has overwhelmed more limited supply. The result: unacceptably high inflation.

While inflation has probably peaked, we are living in a supply constrained world and I suspect inflation will be stickier than central bankers want. Importantly, the decade after the Global Financial Crisis was a time of excess supply, and central bankers around the world kept interest rates artificially low to stimulate demand. Investment strategies that worked well in the aftermath of the GFC seem less likely to work well in coming years – in particular, and as we’ve seen so far in 2022, investment approaches that favor long duration (high P/E) growth stocks may fare poorly in a time of increasing interest rates. If, as I suspect, it takes more time than desired for inflation to fall to levels consistent with the U.S. Federal Reserve’s (the “Fed’s”) definition of price stability (2% inflation), then we may be living with structurally higher interest rates for years. Value stocks may do particularly well in this environment. The Fed has made clear that they will use monetary policy to cool the economy to combat inflation. Just as cool air colliding with warm air over tropical waters produces hurricanes, the collision of increasingly chilly monetary policy and a warm economy could create an economic storm with the potential to turn into a hurricane.

Storm Watch

According to the National Oceanic and Atmospheric Administration, typically 10 tropical storms form each year in the Atlantic Ocean, the Caribbean Sea, and the Gulf of Mexico. Roughly six of these storms grow into hurricanes, but the majority stay at sea. In an average three-year period, only two major hurricanes will strike the U.S. coastline between Texas and Maine. While the 2022 hurricane season had been relatively mild, in just the last two weeks, Hurricane Fiona caused extensive damage in Puerto Rico and Canada while Hurricane Ian has wreaked havoc in Florida and the Carolina coast. Our thoughts and prayers are with all of those who have been affected by these destructive storms.

Recessions are rarer than hurricanes – over the last 40 years, we’ve only had four. While I am hopeful that the growing economic storm clouds will fizzle out over the proverbial ocean, at Poplar Forest, we think it is prudent to plan for something more severe. Fed Chairman Powell seems intent on convincing the market that he can whip inflation, and an aggressive Fed could turn a relatively harmless tropical storm into an economic hurricane. As you can see below, recessionary economic activity (highlighted in grey) reduces companies’ revenues and profits. If there is a recession in 2023, earnings estimates may decline by 20% or more for the S&P 500. We have already seen some diminution in estimates during September and we expect more when companies report third quarter earnings in the next few weeks. While stocks don’t currently look particularly expensive when compared to current consensus expectations for earnings, if those expectations are reduced by 20% or more, then the price-to-earnings ratio on the S&P 500 could increase from the fairly reasonable current level of 16x to a more expensive 20x or more.

Source: Intrinsic Research

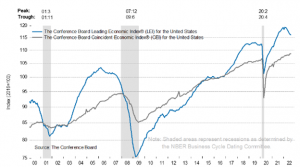

Like meteorologists watching for signs of dangerous storms, we are monitoring various indicators for signals of economic trouble. While the economy looks mostly sunny today, the extended forecast is more worrisome as measured by the Conference Board’s Index of Leading Economic Indicators (the “LEI”). The ten components of the LEI for the U.S. include:

- Average weekly hours in manufacturing;

- Average weekly initial claims for unemployment insurance;

- Manufacturers’ new orders for consumer goods and materials;

- ISM® Index of New Orders;

- Manufacturers’ new orders for nondefense capital goods excluding aircraft orders;

- Building permits for new private housing units;

- S&P 500® Index of Stock Prices;

- Leading Credit Index™;

- Interest rate spread (10-year Treasury bonds less federal funds rate);

- Average consumer expectations for business conditions.

This collection of macroeconomic variables has historically done a very good job of forecasting the direction of the economy; earnings for the S&P 500 have historically followed a similar pattern. As the Conference Board said in its recent release: the “US LEI continued to decline signaling a contraction in economic activity may be imminent.”

Source: The Conference Board

I believe the most helpful leading indicator is the difference (the “spread”) between yields on 10-year Treasury Bonds and the Federal Funds rate. As you can see below, in the past, this indicator has fallen well below zero in advance of recessions. Despite the Fed’s decision to raise rates by 0.75% (to 3.00-3.25%) at its last meeting, this yield spread is currently still well above zero with 10-year Treasury bonds now yielding 3.75%. While risks are growing, increasing long-term interest rates are a sign that the Fed has not yet moved far enough to actually trigger a recession. We will be watching closely to see where long-term rates go as the Fed continues to raise short-term rates (potentially to 4.5% or more in 2023).

In terms of recession signaling, the danger generally comes when long-term interest rates stop going up alongside short-term rates and the yield curve inverts (when short-term interest rates become materially higher than long-term rates). One exception to this rule of thumb was in 1998; the yield curve inverted, and although economic conditions worsened dramatically in emerging markets, a U.S. recession was avoided. The S&P 500 declined 19.3% during a 45 day stretch in 1998, but stock prices quickly recovered and moved higher as the tech bubble continued to inflate in 1999.

Trying to Reason with Hurricane Season

There is no guarantee that restrictive monetary policy will create a recession. And even if it does, it is important to remember that monetary policy works with a lag that has historically averaged about a year – that means we may be looking at mid-2023 before the threatening winds really pick up. At this point, in our multi-year projections for the businesses in which we are invested, we are assuming that we will have to live through a Category 1 or 2 storm (a mild recession) sometime in 2023. I hope this will prove to be an overly conservative assumption, but given the clouds we see on the horizon, it seems prudent to be conservative right now.

As long-term owners of businesses, we don’t turn and run just because a storm might come. Storms come and go and, over time, the market has continued to move to new highs. However, this is not a time for risky investments; we want to make sure that the companies in our portfolio can survive a potential economic hurricane. We focus on the absolute value of businesses (low valuations are like homeowners’ insurance). We avoid speculation (we don’t build on the sand). We focus on businesses with strong balance sheets and consistent free cash flow (it’s important to be resting on a strong foundation when the wind starts howling). We focus on idiosyncratic opportunities (where we’re not merely dependent on the weather staying sunny). We have avoided housing and autos (industries where a storm seems most likely to come ashore). We have been holding a bit of extra cash (the equivalent of bottled water and flashlight batteries in case the power goes out). Our cash reserves are currently around 5% of assets; if we get really concerned that a Category 5 storm is coming, we may take cash to 20-25% of our portfolios if we don’t find great investment opportunities as short-term oriented investors head for higher ground.

Furthermore, I’ve lived through enough cycles to know that people sometimes panic when they hear a dire weather forecast. We have identified a list of companies we’d like to invest in; if someone wants to sell us their beautiful beach house at a 50% discount to what we think its worth, we may buy it – especially if we believe the foundation is strong. During the third quarter, we didn’t establish any new positions as we haven’t gotten sufficiently discounted prices on the properties we have targeted, though some are getting very close. On the other hand, because one of our investments – Organon, a mid-sized pharmaceutical company that was spun off from Merck – has a weaker balance sheet than we’d like in this climate, we liquidated our stake.

The Forecast – Partly Cloudy with a Chance of Thunderstorms

While I’m generally an optimistic person, I came into this year with a defensive mindset. That approach has served us relatively well in this volatile period. Like Bill Murray’s character in the 1980 comedy classic Caddyshack said, about impending rain, while “I don’t think the heavy stuff’s going to come down for a while,” I do think a conservative posture continues to make sense given the Fed’s attitude on battling inflation. One of the longest standing admonitions in the investment business is: “Don’t fight the Fed.” History suggests that when the Fed is raising interest rates, it is prudent to plan for inclement weather, and that’s just what we’ve done.

Historically, value investing has been particularly helpful in managing bear markets. While this wasn’t the case when the Housing Bubble burst, it definitely was when the Tech Bubble popped. I continue to believe that we are in the midst of an investment cycle that resembles the late 1990s/early 2000s period. If I’m right, value stocks will have several more years of outperformance and our focus on absolute value may prove particularly rewarding. As someone who invests alongside each of you, I continue to be excited about the long-term prospects of our portfolio of companies with solid balance sheets, ample free cash flow, and robust idiosyncratic opportunities. While our companies are projected to grow earnings faster than the S&P over the next few years, they are valued at less than 9x estimated 2023 earnings while the S&P is valued at 15x. Though there are a few clouds on the horizon, our portfolio continues to look like an incredible bargain to me.

We will continue to watch the skies for signs of trouble and believe we have a solid plan for navigating whatever weather comes our way.

Sincerely,

J. Dale Harvey

Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.