")

Despite a global pandemic that has killed more than 4.7 million people and shut down huge parts of the global economy, the stock market has done just fine. Yes, we had to live through the COVID Crash that saw the S&P 500 decline by 34% over 33 days, but to my knowledge, no bear market has ever been recovered from so quickly. Trillions of dollars of fiscal and monetary stimulus clearly helped. Vaccines were developed in months, not years, and more than 6.2 billion doses have already been administered worldwide. Sports stadiums are full again, kids are back in school, and workers are slowly heading back to the office. Companies now have more job openings than there are people looking for work. The economy is doing great! No wonder the stock market is near all-time high levels.

With the economy getting back to normal more quickly than expected, the U.S. Federal Reserve (the “Fed”) will soon start the multi-year process of normalizing monetary policy. In the face of potentially rising interest rates, investor worries are growing: stocks look expensive, bond prices go down when yields rise, and cash earns nothing. But, there is a fourth option: value stocks. When I say value stocks, I don’t mean the Russell 1000 Value Index: I mean carefully selected securities trading at highly discounted prices. While the growth-stock-dominated S&P 500 may face a headwind in a rising rate environment, I think that carefully chosen value stocks can grow earnings and enjoy expanding P/E multiples. This isn’t an intellectual exercise for me: Poplar Forest funds account for more than 95% of my investable assets. I own the same stocks, in the same proportions, and pay the same fees you pay. Our interests are aligned.

We are currently invested in 29 companies that we believe can grow earnings about 8% annually over the next few years while paying dividends that currently equal about 2.5% of the value of the portfolio. These are solid businesses – more than 90% are companies with Investment Grade credit ratings that have a history of returning cash to shareholders through the payment of dividends. Despite their financial strength and earnings growth potential, their shares are collectively valued at a bargain price of roughly 10x earnings. Despite widespread speculative excess in the stock market, selectivity has allowed us to assemble a portfolio that we believe can generate long-term investment results that should easily outpace cash, bonds or the S&P 500. While some say value stocks only work when interest rates rise, we think relative earnings growth rates and free cash flows are more important. The companies in our portfolio appear poised to grow earnings at a rate consistent with that generated by the S&P 500 over the last 50 years, yet the portfolio is valued at less than half of the S&P’s P/E.

At Poplar Forest, we invest based on business fundamentals. We strive to buy stocks at substantial discounts to the value of each business’ future free cash flows with the expectation that other investors will ultimately realize the value we see. Sometimes perceived value gaps close quickly, sometimes the process takes years, and sometimes we are wrong. If we have trouble finding what we believe are great ideas, cash may build up in the portfolio as we await better opportunities. (In the late 1990s when stock prices looked really out of whack, cash got to 20-25% of the portfolios I managed.) As we ended the third quarter, cash was less than 3% of our assets as we have continued to find what we believe are very attractive long-term investment opportunities. That said, we liquidated four investments while building new positions in just three. All three of these new investments are under-earning businesses that offer what we believe will be above average earnings growth over the next few years.

While we have no special ability to predict what will happen in the next few months, we believe we are being handsomely rewarded while we wait for the value we see to be recognized by others. Over the last 12 months, the companies in our portfolio produced free cash flow (cash from operations less capital spending) that equaled roughly 9% of their market value as of 9/30/21. This level of cash generation seems particularly attractive in an environment of unsustainably low interest rates and rampant speculation.

Investing versus Speculating

This year, the stock market has been buffeted by growing ranks of traders who are being egged on by new brokerage firms like Robinhood. While they may refer to themselves as “investors,” they look more like gamblers who found each other on message boards and united to take on the “establishment.” They gleefully created headaches for hedge funds who were positioned for expected bankruptcy at companies like GameStop and AMC Entertainment. The fundamentals of those companies were very weak, but the collective will of these speculators drove stock prices higher and allowed the companies in question to raise the funds they needed to survive in a sort of reverse Darwinism.

I worry when I read about the mob’s trading strategies, most particularly, YOLO. For the uninitiated, YOLO stands for “You Only Live Once” – “Let’s buy this stock that’s being touted on this message board. Sure, this thing could go to zero, but it might quickly double. You only live once!!” This short-term, get-rich-quick speculation reminds me of late 1990s behavior that ended with many day traders losing everything.

While speculative excess may continue to build as long as the Fed keeps flooding the market with liquidity, at some point, they will have to normalize monetary policy. I’m reminded of former Citigroup CEO Chuck Prince’s quote back in 2007: “When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance.” The WallStreetBets crowd may keep partying like its 1999, but at Poplar Forest, we are increasingly focused on managing risk given an outlook for increasing volatility and more mundane returns for the stock market as a whole. Security selection seems more important than ever.

Don’t Fight the Fed

Although I am worried about the magnitude of speculation I see in the stock market, I’m not expecting another nasty bear market any time soon. Historically, investors can sleep easy as long as the yield curve is upward sloping – when long-term interest rates are higher than short-term interest rates — as is the case today. While the stock market regularly has short-term corrections of 5-10%, the risk of a bear market decline of 20% or more appears low until the yield curve inverts. I have no reason to believe it will be different this time, but we should all be aware that risks are rising. In short, I believe the coming period of monetary policy normalization will lead to increased volatility.

Everything seems to be riding on the Fed and I can’t remember a time in my career when they had as much influence on financial markets as they have today. In the interest of supporting recovery from the COVID pandemic, the Fed has kept short-term interest rates pinned near 0% while continuing to buy $120 billion a month of bonds. With inflation currently running well north of the Fed’s 2% target rate, owners of bonds are losing purchasing power every day that the Fed resists normalizing monetary policy.

Yield on 10-year Treasury Bonds as Compared to Inflation (Core CPI)

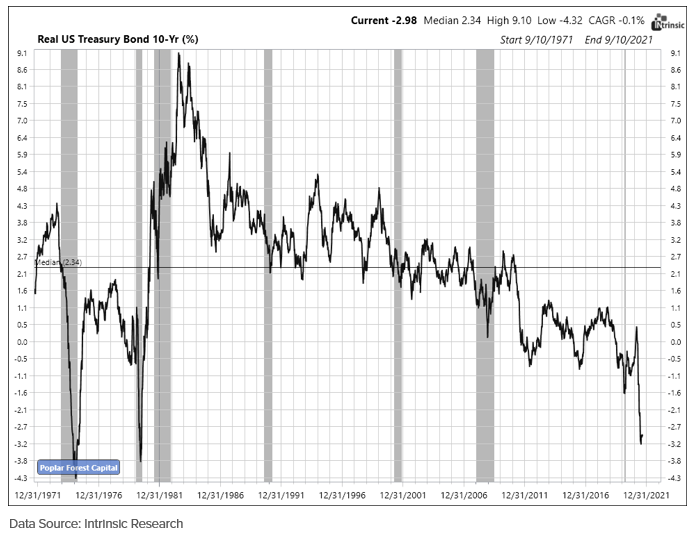

With so much of my personal wealth invested in our funds, I understand the desire to have protection from a bear market in stocks. Government bonds have historically done well when stock prices fall – in effect, bonds are a little like an insurance policy for your stock portfolio. My concern is the current cost of that insurance. Historically, the yield on a 10-year treasury bond exceeded the underlying rate of inflation by 2-3% (this is the so-called “Real” interest rate). While bonds weren’t expected to keep up with stocks, they provided bear market protection while still helping investors grow their purchasing power by 2-3% a year. Today, that relationship has been turned on its head; bond buyers are giving up future wealth in exchange for that stock market insurance policy. In the last 50 years, bonds have only looked this expensive relative to inflation two other times (1974 and 1980).

Chairman Powell had better be right that the inflation we see everywhere really is “transitory.” Otherwise, bond yields could rise dramatically. I am not suggesting that we are on the verge of a 1970s-era inflation problem, but I do believe that the 40-year tailwind of ever-lower interest rates has ended. Rising rates could lead to falling stock P/E ratios, especially for companies with low current free cash flows and high valuations.

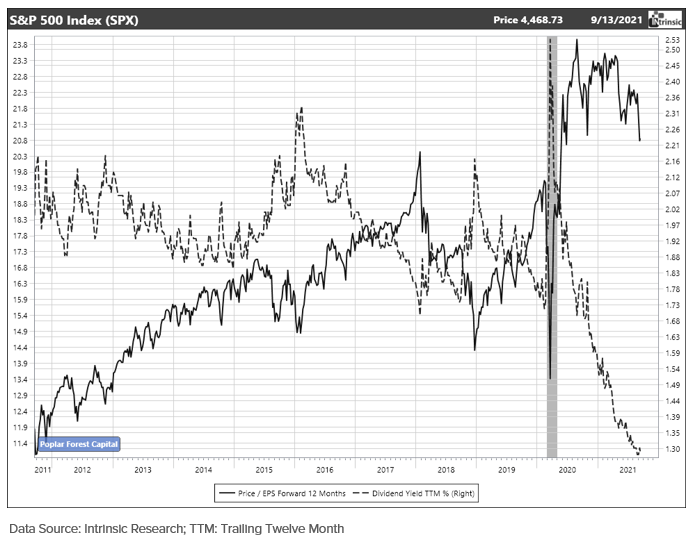

If rates rise, the growth-stock-dominated S&P could be in for a period of disappointing total returns. Over the last 50 years, the S&P 500 has grown earnings at a compound rate of 7%. The current dividend yield is 1.3%. Over the last decade, the S&P 500 has traded at 16.6x expected earnings as compared to its current ratio of 21.0x. If rising rates were to push the S&P 500’s P/E ratio back to that 16.6x average, the 20% valuation contraction could eat up more than two years of historic earnings growth and dividends.

In looking at the graph of the S&P’s valuation over time, we see that this index is trading at a 20% premium to where it has been valued over the last decade. It is much harder to find similar data for the Russell 1000 Value Index, so I examined the top holdings of that index as a valuation indicator. Admittedly, the ten largest stocks only represent 17.5% of the Russell 1000 Value Index, but I think they make an illustrative point. Similar to the data for the S&P 500, the ten largest holdings in the Russell Value Index are currently valued at a 21% premium to where they have traded over the last decade.

In contrast to the S&P trading at a 20% premium and the largest Russell Value stocks at a 21% premium, the largest holdings in the Poplar Forest Partners Fund are being valued at a 10% discount. While the valuations of the leading stock market indices could contract as Fed policy normalizes, I think this data suggests that our portfolio could weather a negative market revaluation; we could actually see P/E multiples expand. While past experience is not a forecast of the future, that is what happened to the cheap stocks I owned back in the late 1990s when the tech bubble burst.

Conclusion – It All Comes Down to Security Selection

In the more than 40 years that I have been investing, I’ve watched as investor portfolios shifted from individual stocks to mutual funds to index funds and ETFs. On one hand, that has helped diversify investor portfolios while cutting costs dramatically. Some may agree with Mae West who said that “Too much of a good thing can be wonderful,” but I think things have gone too far. Free trading apps encourage speculators to buy and sell stocks without knowing what the companies they represent do and with little or no regard for valuation. The other extreme is a portfolio of ETFs and Index Funds. Yes, they offer low fees, but when you own a little bit of everything, you have nowhere to hide when almost everything looks expensive, as it does today.

Passive investing has grown in popularity because investors were comfortable simply getting average results in exchange for low fees. For years, active management has failed to live up to its promise of market-beating results. When it comes to active management, I don’t believe that past performance will be an indicator of future results. At a time when the broad stock averages look expensive and bonds and cash yield less than inflation, I believe this is the ideal time for a benchmark-agnostic, contrarian, high conviction investment process focused on price relative to normalized earnings and free cash flow.

While I expect the path of markets to be a bit choppy over the next 12-24 months as the Fed normalizes monetary policy, I believe that the securities we have selected can generate market-beating, long-term investment results. We believe that the companies in our portfolio can grow earnings at competitive rates while providing an above-market dividend yield. As the market realizes that earnings growth isn’t scarce, we could see value stocks close the valuation gap with growth stocks. And when value beats growth, we believe Poplar Forest can beat both.

Sincerely,

J. Dale Harvey

Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.