Dear Partner,

As Mike Tyson famously observed: “Everybody has a plan until they get punched in the mouth.” For the last few years, Value investing has felt like being in the ring with the former champ. Successful long-term investors know they will have to take a few punches along the way because there is simply no way to get every stock pick right. The issue is not about getting punched: it’s about how one responds to the blow.

In perhaps the greatest pugilistic contest of all time – 1974’s “Rumble in the Jungle” – George Foreman, the undefeated champion and 4-to-1 favorite, had former champ Muhammad Ali on the ropes in the early rounds. But Forman grew tired from throwing punches that were minimized by Ali’s rope-a-dope defensive tactics. As Foreman later explained: “I thought he was just one more knockout victim until, about the seventh round, I hit him hard to the jaw and he held me and whispered in my ear: ‘That all you got, George?’ I realized that this ain’t what I thought it was.”

The former Cassius Clay had won Olympic Gold in 1960 before becoming a professional and changing his name to Muhammad Ali. He became world champion in 1964, but lost the title in 1967 for opposing the Vietnam draft; he was sidelined for four years before the conviction was overturned by the Supreme Court. Once back in the ring, the still-undefeated Ali faced setbacks including a 1971 loss to Joe Frazier and a broken-jaw loss to Ken Norton in 1973. By the time he stepped into the ring for his ’74 bout with Foreman, the consensus opinion was that Ali was past his prime. But in the eighth round, Ali knocked out the exhausted Foreman, shocking the world and winning the title.

These days, value investors get about as much respect as Ali did before he faced off with Foreman. We are deemed to be past our prime given the new disruptive business models of Amazon, Google and the like. Growth and Momentum investing strategies have been champions for over a decade now, but at Poplar Forest, we think these approaches are running out of energy. Like Ali, we can take a punch. We may not float like butterflies, but we have grit and determination. We have the fortitude to stick to our plan even when we get hit in the jaw.

As you know, our investment process focuses on stock prices relative to normalized earnings and free cash flow. We assess individual businesses from the perspective of an owner who knows that there will be good years and bad years, and who understands that the fair value of a company should be based on mid-cycle results as opposed to the highs and lows that every business experiences over time. We buy a stock when we see a disconnect between its current price and our estimate of its fair value three years into the future. By disconnect, I mean the potential for us to earn at least 15% a year for at least three years (our target rate) assuming the stock has attained fair value by year three.

I have used this bottom-up process for twenty-three years now and I continue to believe that it is both philosophically sound and capable of delivering market-beating returns. History shows that, in the long run, stock prices follow earnings, and the companies in our portfolios are expected to grow their per share earnings by 8-10% per year over the next three-to-five years. Despite this attractive level of growth, the portfolio trades at just 11x earnings and a gross dividend yield of nearly 3%. Given the financial characteristics of the companies in which we’re invested, I believe the portfolio should be valued at closer to 15x earnings – multiple expansion alone could potentially drive a 35-40% gain from where the portfolio was trading on 9/30/19.

An investment process focused on normalized earnings can face headwinds when the majority of investors are pre-occupied with what can go wrong in the short term. Global economic growth has clearly slowed and there is raging debate about whether slow growth will give way to recession. While we don’t see the level of excess that typically precedes a recession, the yield curve, historically a reliable recession indicator, is flashing warning lights. Some commentators say the inverted curve is a false alarm driven by interest rates in Europe and that we’re simply living through a short-term, mid-cycle slowdown like we experienced in 2013 and 2016.

We don’t manage portfolios based on top-down economic forecasts, but we understand that the top-down concerns of other market participants can hurt the performance of our portfolios in the short-term. We will continue to focus on normalized results while acknowledging that the current backdrop is far from normal with a trade war, impeachment proceedings, weak industrial production, a President who called the Chairman of the Federal Reserve an “enemy,” unrest in the Middle East, negative interest rates overseas and an inverted yield curve (when long-term interest rates are lower than short-term rates) here at home. The short-term headlines look worrisome, but we believe investors are overly focused on what can go wrong in the here and now while paying little attention to what can go right looking out three to five years.

Investors’ Preoccupation with Volatility and Downside Risk has Created Opportunity

We acknowledge that risks are more elevated than they have been in years, but we don’t think the answer is to buy low yielding bonds or expensive electric utility or consumer staples stocks. Price matters — and we are willing to accept risk if we are paid to do so. Our fundamental analysis includes not just a base case view of normalized earnings and free cash flow, but also an assessment of each investment’s downside in a recession. Given the discounted valuations of our portfolios, we feel more than amply compensated for risks that have scared away other investors. Compared to the less cyclical companies in the portfolio, many of the economically exposed stocks we own appear priced to provide an extra return of 10% a year, over our three-year investment horizon, as compensation for their economic sensitivity. In contrast, when we’ve looked at more defensively postured businesses like electric utility companies, they appear to offer prospective returns in the 0-5% range. Purportedly “safe” stocks look unattractive (and potentially dangerous if their P/E’s revert to long-term levels) while supposedly “risky” value stocks look to be priced for outsized long-term returns.

An environment that has embraced growth and momentum stocks while shunning value investments has allowed the broad market averages to levitate at near record levels. There seems to be a belief that either the trade war will end or that the world’s central bankers will solve any problem by cutting interest rates. I think this is wishful thinking: lower interest rates are no remedy for a trade war. Lower rates may help offset some of the pain in the best of times, but I fear that over use of interest rate cuts has resulted in the decreased efficacy of monetary policy. The world’s central bankers have been running a decade-long experiment with low and/or negative interest rates and the result has been disappointing economic growth. Japan and Europe have pushed interest rates into negative territory and their economies are on the brink of recession. Why should we believe lower rates will work any better for us than they have for them? This is important because I don’t think the trade war with China will end soon. I hope we’re wrong, but we feel it is better to plan prudently than to simply hope for the best. We are also working on the assumption that the presidential election process will see tweets and candidate statements that continue to create market volatility.

Some investors treat volatility like a four-letter word, but we see it differently. Volatility provides opportunities for us to buy stocks at discounted prices when people panic and to sell stocks at high prices when investor fear dissipates. This is the advantage of a bottom-up investment process that focuses on normalized earnings and free cash flow. Assessment of fair values based on rigorous fundamental analysis gives us the confidence to calmly take advantage of the emotional swings of others. A world increasingly dominated by value-insensitive passive investment strategies, like index funds and ETFs, could create even bigger opportunities for us to buy low and sell high.

Value Investing – Not Washed Up

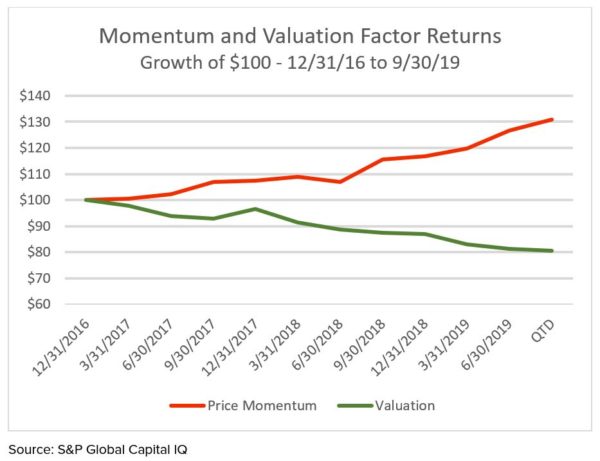

Like Ali in 1974, Value investing is deemed to be past its prime. The champions of recent years have included Growth stocks including Facebook, Amazon, Apple, Netflix and Google (“FAANG”) as well as “Safety” stocks like electric utilities and REITs. The strength of these sectors has been magnified by the popularity of Momentum investing – a strategy of buying the shares of stocks that have gone up a lot on the belief they will go up even more. Since the end of 2016, Momentum has had Value on the ropes.

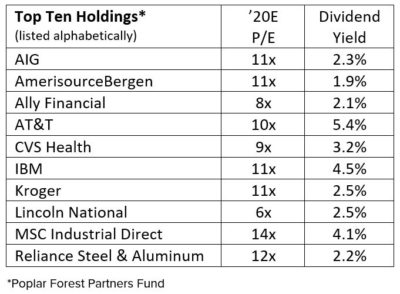

Momentum stocks may look as strong as an undefeated Foreman in ’74, but that doesn’t mean they will win the Rumble on Wall Street. Value investments aren’t sexy – our top ten holdings include presumed “has-beens” like AT&T and IBM and lesser known companies like Ally Financial and Amerisource Bergen. Though under-appreciated, we think the shares of these durable businesses can outperform over the next three-to-five years.

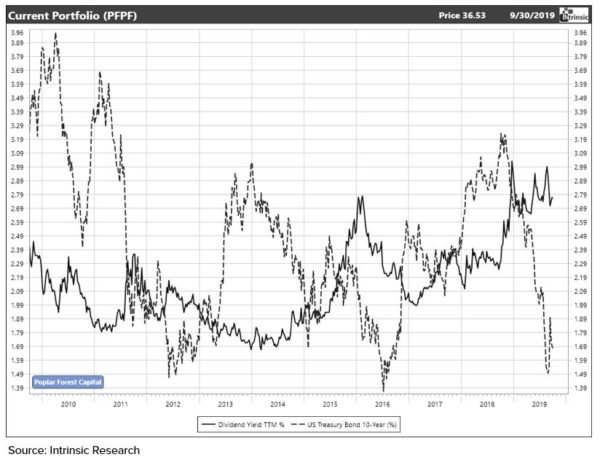

One over-looked attribute of value stocks is their robust free cash flow and their generally above average dividend yields. I find this particularly surprising in an environment in which fearful investors pushed the rate on 10-year Treasury bonds to a low of 1.5% in late August. While interest rates have moved up in recent weeks, as you can see in the chart below, our top ten holdings are trading at low prices relative to their expected earnings and they compare quite favorably to the current 1.67% yield of a 10-year treasury bond.

In the last 12 months, the companies in our portfolio distributed dividends equal to roughly 2.7% of the portfolio’s value – a full 1% more than a 10-year Treasury bond. Our stocks are currently providing some of the highest yields in a decade at the same time that Treasury bonds are near the lowest yields in that same time period. Furthermore, the income generated from Treasury bonds is fixed whereas the dividends paid by our companies are expected to grow on the order of 5-10% a year in the coming decade. Why would a long-term investor give up extra income and growth of that income in exchange for a bond that yields little, if anything, more than inflation? That might make sense on a short-term basis if we’re headed for a recession, but it seems like a significant opportunity cost for anyone with a multi-year time horizon.

Welcoming Experienced Pros to Our Corner

Thankfully for me, investing isn’t a contact sport with risk of concussion and brain damage. Professional investors can have multi-decade careers and I see myself standing tall in the investing ring for at least another twenty years. Having a decades-long time horizon is important in this profession as cycles can last many years, as evidenced by Value’s underperformance since the Great Recession. As I hope is clear in this letter, and in other communications you’ve gotten from us, we firmly believe that a Value cycle is coming. We don’t know when it will start (it may have even started at the beginning of September), but given historically wide valuation differentials, the rewards for perseverance could be substantial.

While boxing is a one-on-one contest, investing is a team endeavor. We have a world class investment team and are excited to have recently added two more experienced professionals to that lineup. Phyllis Thomas and Gregg Tenser joined us in July to head up a new small cap value initiative. Phyllis and Gregg first started working together in 2001 and they collectively have 65 years of investment experience. Their value philosophy dovetails beautifully with ours. As frustrated as we are with the performance of large value stocks, small cap value stocks have lagged their large peers by 1-2% a year over the last five and ten years and we think that underperformance spells opportunity.

As I’ve written previously, the current market cycle reminds me of the late 1990s period – the last time Value was declared dead. That cycle taught me the importance of sticking with a philosophically sound, and now time-tested, investment process. Following that process has produced portfolios that we believe offer incredibly compelling opportunity: 8-10% expected annual earnings growth plus almost 3% dividend yields. With the S&P 500 trading at 17x earnings, I believe this portfolio of predominantly Investment Grade rated businesses should be valued at close to 15x earnings, yet investor disdain for value stocks has it priced at just 11x.

In an environment that may have put other managers down for the count, we are positioning ourselves for growth and success. I haven’t started knocking back raw eggs for breakfast, but we will continue to work hard every day. While some of you have had ring-side seats for 12 years now, others are newer to our story. We appreciate the support all of you provide – it adds fuel to our fire. We believe that history is on our side and that Value is primed to regain the title!

Sincerely,

J. Dale Harvey

Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.