Questions of Value — What Do You Have to Believe For Growth to Outperform Value?

Questions of Value is a series of memos in which we address common questions from our clients about the Partners Fund and Value investing. We welcome your feedback and suggestions for future memos.

Over the last 10 years, the performance of Value styles, as represented by the S&P 500 Value Index, has significantly lagged Growth styles, as represented by the S&P 500 Growth Index. Our analysis suggests the majority of this performance gap is due to a widening spread in valuations between the two investing styles. Based on price to next twelve-month earnings (NTM P/E) ratios, the difference in relative valuations between Growth and Value investing styles expanded to historically extreme levels in 2021. Many of our clients have benefitted from Growth’s historic run of outperformance and are now questioning whether it makes sense to rebalance some of their Growth-related profits into Value-oriented portfolios like the Poplar Forest Partners Fund. This strikes us as an important question for all equity market participants to consider. When exploring difficult questions, inverting or reframing the debate can helpful. For instance, the merits of increasing allocations to Value portfolios can be clarified by asking: “What do you have to believe for Growth to outperform Value from here?” In this memo, we explore this question by analyzing the past and future drivers of index performance.

Excluding rebalancing effects, the future performance of Growth and Value styles can be distilled into three key variables: (1) profits, or EPS Growth; (2) income, or dividends; and (3) valuation, or price-to-earnings (P/E) ratios. Following Growth’s outperformance of Value over the last ten years, to believe that Growth will continue to outperform you have to believe that at least one of these three variables will consistently favor Growth, such that the sum of all three enables the total returns of Growth to exceed those of Value.

Total Returns = EPS Growth + Dividend Yield + P/E Ratio Changes

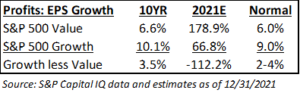

EPS Growth

Before thinking about the future trends of these three variables, it is helpful to analyze historical patterns. Over the last ten years, the S&P 500 Value Index grew earnings per share at a 7% CAGR versus a 10% CAGR for the S&P 500 Growth Index. Longer-term time series also suggest a 2-4 percentage point gap in earnings growth is typical when comparing Growth and Value styles since, by definition, Growth indices favor faster growing companies. In 2021, EPS Growth for Value styles exceeded that of Growth styles mostly due to cyclical rebounds in earnings from Financial Services, Basic Materials, and Energy companies — many of which had experienced meaningful profit declines or losses in 2020. During 2022-23, however, we expect profit growth trends for most companies to trend closer to historical averages.

The last ten years saw an unprecedented amount of innovation and disruption throughout the economy and we wouldn’t be surprised for these trends to persist. While disruptive innovations can be problematic for incumbent companies incapable of adaptation, overstated disruption risks can also create opportunities for discerning Value investors. One of the reasons we have allocated significant portions of the portfolio to the Financial Services and Healthcare sectors is because extensive government regulation of these sectors slows the adoption of disruptive technologies. This regulatory buffer on disruption improves the ability of established firms to successfully adapt their business models and potentially convert disruptive innovations into sustaining innovations. When high quality businesses get valued as if they will be imminently disrupted, attractive investment opportunities can emerge for highly selective, contrarian Value investors. For the sake of this general discussion about Value and Growth styles, we assume that disruptive innovations will continue and wouldn’t be surprised to see normalized EPS growth for Growth indices exceed Value by about 2-4 percentage points (as shown in the “Normal” column below).

Dividend Yields

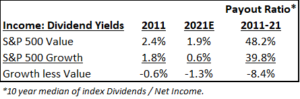

After profits, or EPS Growth, the second driver of total returns is income, or dividend yields. The dividend yields of Value stocks tend to be higher than Growth stocks since more mature companies don’t need to allocate all of their profits to reinvestment opportunities and can consistently return some portion of these profits to shareholders through dividends. The higher dividend yields of Value stocks serves to partially offset their lower EPS growth potential versus Growth stocks. Over the last ten years, dividend yields of both Growth and Value indices declined as stock prices and valuations increased faster than dividends. This has been particularly true for Growth indices where the dividend yield has declined from 1.8% to 0.6%.

While the dividend yield of a stock or index reflects dividends divided by the stock price, the payout ratio reflects dividends as a percentage of net income, or EPS. The payout ratio will vary over time depending on where we are in the economic cycle. History suggests Value indices tend to have a payout ratio that is 8-10 percentage points higher than Growth indices, which makes sense since Growth companies often have more reinvestment opportunities than Value companies. Over the next few years, we would expect dividend yields between Value and Growth indices to be more impacted by changes in stock prices than changes in payout ratios. From current price levels, we would expect the total return of Value indices to benefit from at least a 1 percentage point higher dividend yield than Growth indices.

P/E Ratio Changes

On the basis of normalized business fundamentals, we’ve suggested that Growth indices could generate EPS growth that is 2-4 percentage points higher than Value while Value indices offer dividend yields that are 1 percentage point higher than Growth. This simple math suggests an aggregate 1-3 percentage point return tailwind in favor of Growth, excluding any changes in valuation. At the end of 2021, however, relative valuations between Growth and Value indices were nearing extreme levels.

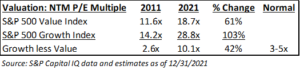

Over the last ten years, valuations, as measured by the price to next twelve months earnings (NTM P/E) ratio, increased about 60% for the Value indices but 100% for Growth indices. At year-end 2021, the NTM P/E ratio for the Growth index was around 29x, approximately 10 points higher than the NTM P/E ratio of the Value index. This 10 point excess compares to a median difference in NTM P/E ratios over the last 10 or 20 years of closer to 3-5 points. If the current valuation difference between the two styles were to revert to historical medians, that would create a 20-25% headwind to total returns for Growth indices versus Value. This potential valuation correction dramatically overshadows the 1-3 percentage point performance tailwind in favor of Growth from business fundamentals (EPS Growth + Dividend Yield). It is worth noting that recent indications from the Federal Reserve that they plan to raise interest rates could hasten a valuation correction in Growth stocks. We are less concerned about the impact of rising interest rates on our portfolios since the Poplar Forest Partners Fund trades at an 11x NTM P/E ratio, which represents a significant valuation discount to both the S&P 500 Value and the S&P 500 Growth Indices.

There’s great value in Value

In conclusion, to believe that Growth will continue to outperform Value, you have to believe that: (1) historically extreme valuations between the two investing styles will persist or expand; and/or (2) the relative performance of business fundamentals for Growth indices compared to Value will significantly exceed our estimates of normalized EPS growth and dividend yields. We find neither of these beliefs compelling and think the stage is set for a multi-year period in which Value indices can outperform Growth.

We believe the current environment is particularly well suited to our investment process. The Poplar Forest Partners Fund is a 30 stock, best ideas portfolio of high conviction value investments crafted to outperform our benchmarks over the long run. When compared to the S&P 500 Value Index, we believe the Poplar Forest Partners Fund offers higher potential EPS growth, similar dividend yields, and a lower valuation.

Let’s Discuss — We’d Love To Hear From You

Please contact Drew Taylor (dtaylor@poplarforestllc.com or (626) 304-6030) or your Poplar Forest relationship manager with feedback and suggestions for future Insights. Follow us on LinkedIn where we commonly post useful and informative material.

Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.