")

My father taught me to drive in a sky-blue Ford pickup truck with “three on the tree” – a three-speed manual transmission whose gearshift was mounted on the steering column. Dad’s hands-on lessons were terrific, but for sheer shock value, they paled in comparison to the gory car crash videos my classmates and I were forced to watch in Drivers Education class. Our teacher seemed determined to scare all of us into driving safely. Of all the lessons he drilled into us, he repeated one more than any other: “Drive defensively.”

These days, the investment highway seems more treacherous than an L.A. freeway in a rainstorm. Among the obstacles in any stock picker’s path: resurgent COVID in Europe and Asia, the Russian invasion of Ukraine and the resulting sanctions, soaring commodity prices, plunging consumer confidence, and last but not least, the Federal Reserve’s recent decision to finally begin normalizing monetary policy. These driving conditions led to a number of traffic accidents as evidenced by the 13% selloff in the S&P 500 between January 3rd and March 8th. During this time, the Russell Value Index outperformed its Growth sibling by more than 12%. Value has become defensive again, just as it was in the aftermath of the late 1990s Tech Bubble.

At Poplar Forest, we aren’t assembling our portfolios in a vacant parking lot; we’ve had to stay keenly aware of other drivers. And that has paid off. Our portfolios held up well during the recent stock market correction and we ended the first quarter with a gain of 4%. As we have said in the past, when value beats growth, we expect to beat both. The recent quarter provided more evidence supporting that contention. And with our portfolio being valued at less than 11x earnings despite prospects for 8-10% annual earnings growth, we remain very excited about prospective returns.

We have continued to follow the road less traveled in search of new opportunities. During the first three months of the year, we found two heavily-discounted investments and added them to our portfolios. One is a consumer healthcare company while the other is a transportation business whose shares have been buffeted by the current macroeconomic uncertainties. Importantly, both are “self-help” investments offering idiosyncratic profit improvement opportunities that are independent of the external environment – profit improvement potential that we believe is significantly underestimated by investors.

As we survey the road ahead, our biggest concern is inflation. If left unchecked, inflation eats away at the purchasing power of our investments. In an environment of ridiculously low interest rates, inflation is a value transfer from savers to borrowers. In the long run, taxing savings and subsidizing borrowing is bad public policy and can lead to serious misallocations of capital across the economy. At its essence, high inflation readings are a reflection of a basic truth – demand exceeds supply for just about everything in the economy right now: gasoline, food, cars, housing, semiconductors, etc. Inflation seems likely to continue to erode purchasing power until demand and supply come more into balance. This is particularly a challenge for low-income consumers and retirees living on a fixed income.

COVID Constrained Supply + Stimulus Driven Demand = Inflation

Two years ago, lockdowns intended to limit the spread of COVID resulted in a six-month, 10% economic contraction, as measured by inflation-adjusted Gross Domestic Profit (“real GDP”). To put that in context, during the Global Financial Crisis (GFC), real GDP shrank 4% over twelve months. The COVID lockdowns led to a 14.4% decline in jobs in just two months (as compared to a 6.3% loss over 21 months during the GFC). The Global Financial Crisis was, by a factor of two, the worst recession since World War II, and the COVID Crisis was more than twice as bad as the GFC.

In and of itself, a 14.4% decline in employment would have been devastating for the U.S. economy. The U.S. Federal Reserve (the “Fed”) and Congress responded with unprecedented monetary and fiscal stimulus. As a result, the economic hardships from COVID were dampened and demand for goods remained strong as we all settled into new work-from-home routines. Within 15 months of the lockdowns, consumer spending was at all time high levels.

With demand having largely recovered from the COVID Crisis by late spring 2021, it would have been prudent for the Fed to begin normalizing monetary policy. But they didn’t. Instead, though we were no longer in a crisis, the Fed continued with crisis-based policies. Stimulus driven demand quickly came up against COVID-constrained supply. Real GDP grew by 7% in the fourth quarter of 2021 (as compared with roughly 2% per year since the GFC), yet the Fed continued to leave interest rates unchanged while adding to their already bloated balance sheet by buying more bonds. With the Fed failing to do its job, the free market was left to use price as the mechanism to balance the books between elevated demand and constrained supply.

With free markets behind the wheel, investor focus has shifted to demand-destruction, for example: with consumers paying more for gasoline, they have less to spend on clothes. Some worry that reduced consumer spending could drive us into recession. I think that is unlikely given the underlying strength of the economy, but I acknowledge the disquieting message of plunging consumer confidence. While the road ahead may be bumpy, I remain hopeful that supply will recover more quickly than feared. We are starting to see the first signs of that when we talk with companies. While it is understandable that short-term traders may sell stocks based on potential revenue headwinds, normalized earnings and free cash flows should be relatively unaffected. Given our differentiated time horizon, these short-term selloffs may create opportunities for our long-term investment process.

We are currently finding lots of compelling opportunities and I feel a bit like the proverbial kid in a candy store – I just wish I had a bigger shopping cart! We love the companies we own and they collectively trade at a 45% discount to the S&P 500 (based on relative multiples of estimated earnings over the next 12 months) despite comparable earnings growth, solid balance sheets and above market dividend yields. Bluntly put, we don’t want to sell any of them right now. To fund the purchase of new investments, we expanded the Poplar Forest garage, which usually holds 30 investment vehicles, to make room for two more.

Potential Potholes: COVID, War, Consumer Confidence, Interest Rates

Here in the U.S., COVID cases have declined by more than 90% from the Omicron peak. In Europe, the news is not as good as case counts only fell around 50% from their peak, and they have started rising again. China is even more troubling as their zero COVID policy has resulted in limited herd immunity. In the short-term, lockdowns in China and the potential for COVID absenteeism in Europe could exacerbate currently constrained supply. Factories can’t run at full capacity if their workforce is out sick. We will continue to monitor COVID data for signs of an emerging new variant that could derail a recovery in supply.

Likewise, the Russian invasion of Ukraine is not just a humanitarian disaster, it also adds to the world’s supply problems. Sanctions have constrained Russian oil exports, and higher gasoline prices have reduced consumers’ disposable income. Transportation costs are climbing and will make their way into the prices of finished goods. The prices of metals and agricultural products have also risen dramatically and these increases will further erode consumer purchasing power. The European economy was a bit weaker than the U.S. economy prior to the invasion, and given the geography, the war may push Europe into recession. We will be closely monitoring the situation in Ukraine and, in particular, the evolution of sanctions.

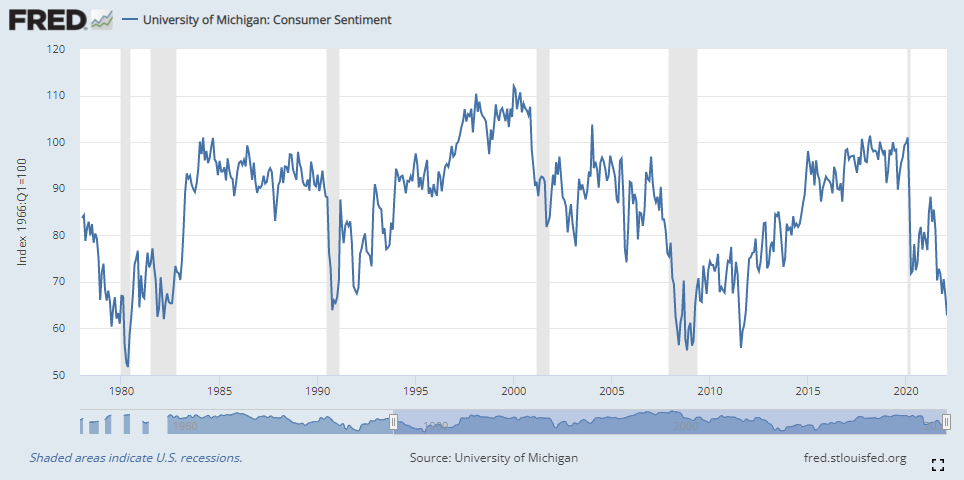

Given these challenges, it probably shouldn’t be a surprise to see the recent decline in Consumer Confidence as reported by the University of Michigan. The current sentiment measure has fallen below the lows seen during the depth of the COVID Crisis and is a data point that is historically inconsistent – at this point in the recovery from a recession, people are usually feeling better. A pessimist would look at this chart and think that gloomy consumers will cut back on spending thus increasing the odds of recession. I look at it differently. I get concerned when conditions look too good to continue. During the peak of the Tech Bubble’s excesses, sentiment exceeded 100 on Michigan’s scale; today we are below 70 – that suggests a lot of upside potential. If I’m right about the underlying strength of the economy, we should see this economic indicator start to move higher..

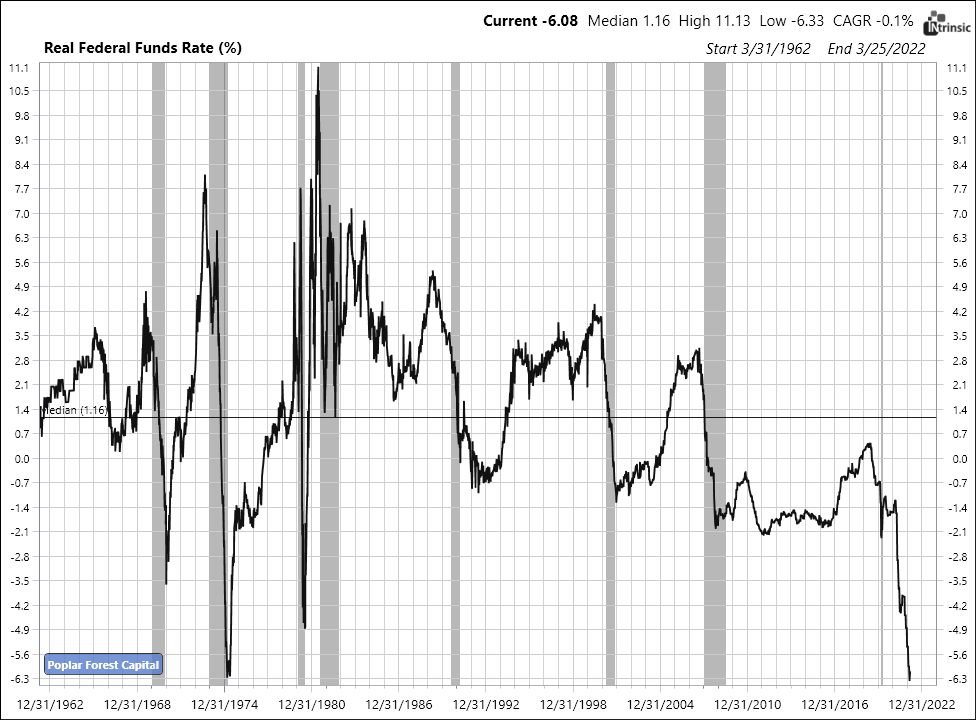

While I believe the Fed is woefully behind in its efforts to at least normalize monetary policy, in March they at least took a first baby step with a 0.25% increase in short-term rates (and they suggested they will soon start to shrink their $9 trillion portfolio of bonds). Despite this, interest rates that are well below the rate of inflation continue to encourage borrowing in an effort to stimulate economic growth. Monetary policy is highly accommodative and the Fed will have to dramatically change its behavior if it wants to avoid being written up for reckless driving. With this first move, the Fed has begun to slowly take its foot off the gas but this seems insufficient to slow down the race car that is the U.S. economy.

As you can see in the graph above, during recessions short-term interest rates are typically cut to a level below inflation to encourage growth. With the exception of the post-GFC era, later in the economic cycle, when demand is more robust, short-term interest rates have been increased to a level 2-3% above inflation in order to cool the economy. Even after March’s 0.25% increase, interest rates continue to be at historically low levels as compared to inflation. The Fed has not fundamentally changed its driving behavior despite getting a speeding ticket for the highest inflation in forty years!

We will be closely monitoring the bond market (credit spreads and the slope of the yield curve) for signs of stress, but our working assumption is that both short- and long-term interest rates will end up higher than expected by most market participants. Given the correlation between interest rates and stock price valuations, the S&P 500 could end up spinning its wheels as continued earnings growth is offset by lower valuations. This dynamic could continue to be a major challenge for the sports cars of the stock market (highly valued growth stocks), but should be less of an issue for the companies we own, given the four-wheel-drive power of their low absolute and relative valuations.

Help Navigating the Road Ahead

A recent study from the American Automobile Association (AAA) confirms what we’ve all seen firsthand – there are more risky drivers on the road. AAA’s study found a marked increase in “younger and disproportionately male” drivers who are “a statistically riskier driver group than the average population.” Meanwhile, “safety-minded individuals” are driving less. If ever there were a time to practice defensive driving, it’s now!

Just as highways are crowded with more speed demons, the stock market seems to have more risky investors zigging and zagging about. I’m glad that I don’t have to navigate all this traffic by myself. For years now, Derek Derman has been riding shotgun alongside me. He initially joined Poplar Forest in September 2011 as an analyst covering financial service companies. After putting up several years of outstanding investment results, he joined me as Co-Portfolio Manager when we launched the Cornerstone Fund in 2014. Derek and I have worked very closely ever since and I have grown to appreciate his sensitivity to risk. Derek has a keen eye for black ice and other dangers that could leave us broken down on the side of the road. In recognition of his contributions, I have named Derek Co-Portfolio Manager for the Poplar Forest Partners Fund.

While I will continue to be the guy driving the bus, I hope you will enjoy the ride a little more knowing that Derek, a 25-year investment veteran, is my co-pilot. I’m hopeful that with Derek’s help, we’ll have a smooth ride for many years to come. I want to be clear; I am just 56 years old, in great health, and I have no intention of getting out of the drivers’ seat. But if something unexpected were ever to happen to me, I have every confidence that Derek, with the support of our outstanding analyst team, would keep driving in the direction of long-term investment success.

The era between the Global Financial Crisis and COVID was a challenging one for value investors. Many of you have been with me since the beginning and I appreciate the support you showed us when it appeared that we were getting left in the dust. Times appear to be changing – value has begun to outperform while also being defensive in recent market drawdowns. Like the Tortoise in Aesop’s fairy tale, we have consistently followed our long-standing investment process despite what appeared to be an insurmountable lead held by the growth stock Hare. Investing isn’t a quarter mile drag race, it’s more like the multi-day, 6,200-mile Dakar Rally from Paris to Dakar Senegal. I believe we have the endurance, the equipment, and the crew to not just finish at Dakar, but to end up in the winners’ circle.

Sincerely,

J. Dale Harvey

Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.