Dear Partner,

On hot summer weekends when I was a kid, my family would sometimes drive up into the Blue Ridge Mountains to picnic by the side of Little Stony Creek. My brother and I would wade into the cool water to hunt crawdads while my dad cooked over a fire he’d built. To me, there will always be something extra tasty about food prepared over a campfire.

My dad knew there were a lot of different ways to start a fire; the important thing was to pick the right one for the job at hand. When building a campfire, he used newspaper and kindling. Once he got that going, he’d add bigger logs. Wanting to be like my father, I’d build a small ancillary fire with dried leaves, moss, and twigs. My goal was always to ignite my blaze with just one match. I remember gently blowing on the embers and watching the flames grow.

Back at home, my father liked grilling over charcoal, and he’d use lighter fluid to get the briquettes going. My brother and I were amazed by the power of lighter fluid, especially after we learned how to build soup can cannons which used the liquid to propel tennis balls as far as the eye could see. Over time, however, we learned that the lighter fluid’s blaze — while big and bright — was also brief. All by itself, it burned only a short time. You certainly couldn’t cook a hamburger with it.

Relighting an Economic Fire

I’ve been thinking about this lately as I’ve watched the Federal Reserve try to rekindle our economic fire amid the COVID-19 pandemic. In campfire cookery terms, the virus has been like a once in a hundred year downpour that soaked the woodpile — wet wood doesn’t burn well. Fortunately, the Fed has trillions of dollars of industrial strength lighter fluid. When combined with the dry kindling that is the U.S. Congress’s fiscal stimulus, the economy could soon be cooking again. With our portfolio trading at less than 14x depressed 2020 estimated earnings, we feel very well positioned for recovery.

Value investing tends to work best when economic conditions are improving. The value universe has higher cyclical exposure (49% of the Russell 1000 Index vs. 35% of the S&P 500 Index) and higher operating and financial leverage, which magnifies accelerating top line growth. Prior to the recent uptick in COVID cases, deep value stocks were rallying as investors recognized improving economic heat that may grow with intensity in coming months. For example, we saw a 17.7% jump in retail sales and a 44.4% rebound in pending home sales in May and surprisingly strong increases in regional Fed Manufacturing Indices. The question now is whether we are simply seeing short-lived lighter fluid flames or the first signs of self-sustaining fire.

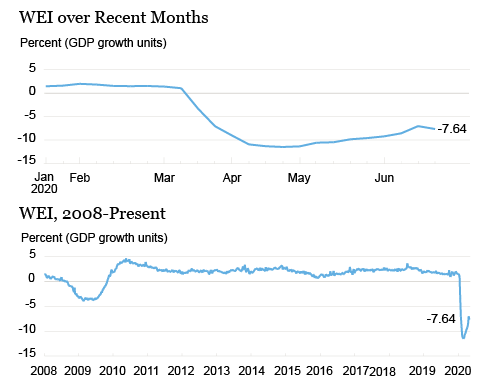

This question is as critical to the Fed as it is to investors more generally. The Fed wants to pour on just enough fuel to get the fire going without creating worrisome inflation. To help monitor their task in real time, the Fed has devised a short-term measure of the economy they have labeled the Weekly Economic Index (or WEI). Per the Fed: “The Weekly Economic Index (WEI) provides a signal of the state of the U.S. economy based on data available at a daily or weekly frequency. It represents the common component of ten different daily and weekly series covering consumer behavior, the labor market, and production.”

As you can see, this Weekly Economic Index suggests that the economy hit bottom in mid-April. If the available anecdotal evidence is correct, we could see this short-term gauge of activity start to improve more rapidly in coming weeks. If we are right that economic activity is improving, then value stocks should do well. Perhaps we simply need to heed the old adage “don’t fight the Fed.” The Fed has made clear its intention to do whatever it takes to get the economy going again. In addition, with Congress likely to provide a second round of fiscal stimulus this summer, the economy could soon get hot.

Could COVID Douse the Flames?

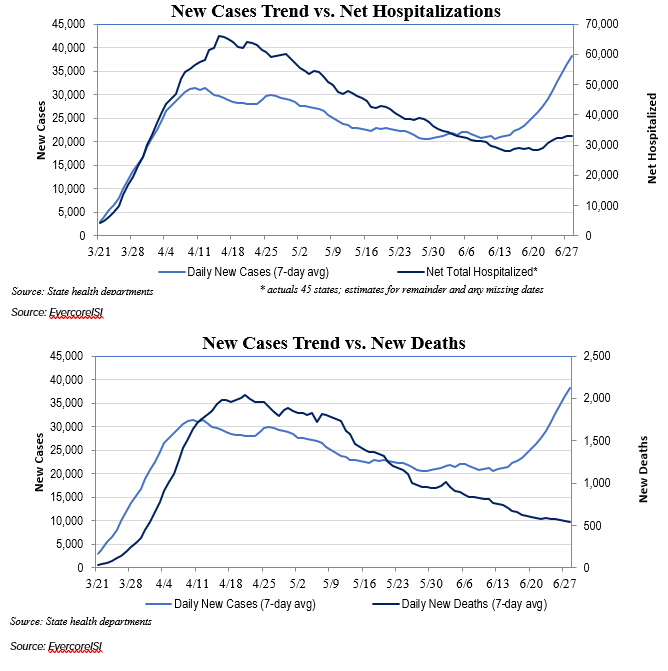

The biggest potential impediment to this outlook, obviously, is the COVID-19 virus. Recent headlines have pointed to increasing infections amid protests and the reopening of the economy. While we are certainly watching the growth in daily confirmed cases, we believe the critical variable to watch is hospitalizations. Encouragingly, new hospitalizations and deaths have positively deviated from new case growth.

In addition to the data presented above, we are encouraged by two other observations. First, European countries have generally not seen an uptick in cases as they reopened their economies. Second, front line healthcare workers, those presumably most exposed to the virus, have shown below average rates of infection. Being exposed doesn’t automatically translate into illness, particularly if we all wear masks and stay out of bars. With confirmed cases growing, we expect individuals to increase their compliance with health recommendations regarding masks and social distancing – actions that can “bend the curve” again.

As summer gives way to fall, there will likely be concern about a second wave of COVID cases. While this fear may prove justified, we believe there will be rapid advances in treatment protocols in coming weeks and months that will dampen the impact of a second wave. For example, in mid-June, we learned that the generic drug Dexamethasone resulted in a 30% reduction in deaths among severely sick COVID patients. We expect more announcements like this to result in a cocktail of treatments that dramatically lower the death rate going forward. If new treatments continue to make the disease less deadly (and thus less scary), consumer confidence may improve and boost the economy along with it.

Investors are Skeptical that the Economy’s Relit Fire is Self-sustaining

After suffering the quickest and, perhaps, most violent bear market on record as the economy was shuttered to minimize COVID deaths, stocks have rallied with equal fervor after bottoming in late March. The first phase rally (March 23 to May 14) was driven by Fed induced reduction in discount rates, and growth stocks continued to lead the market. The second phase of recovery, driven by initial reopening of the economy, saw a shift in performance with deep value stocks taking the lead. With our investments consciously skewed toward deep value stocks, we enjoyed the recovery. Given the portfolio’s near record discount to the S&P 5001, we see the potential for several years of substantially better than market results as the economy heals.

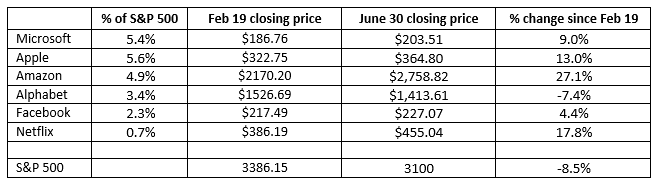

While much has been made of the dramatic increase in stock prices since the March 23 low, the performance of the S&P 500 has been skewed by the leading growth companies. For example, the market darlings listed below collectively account for approximately 22% of the S&P 500. These companies declined less in the COVID Crash and recovered far more than the average stock in the S&P.

Furthermore, the median stock in the S&P is still more than 16% lower in price than it was at the February 19th high. The deep value part of the market is even further from record high territory. For example, the S&P 500 Pure Value Index is still down more than 27% from its level at the market peak on Feb 19th. When confidence that our economic fire has been rekindled, we should see improvement in the performance of a broader based group of stocks, and value stocks in particular.

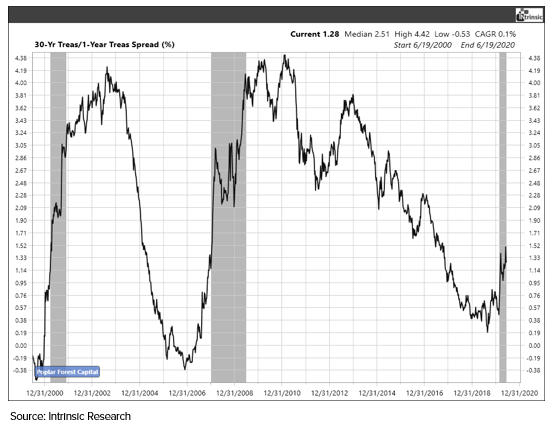

Like the temperature gauge on an oven, the difference between short- and long-term interest rates can be a helpful indicator of the heat of the business environment. As you can see above, the difference (or “spread”) between the interest rate on 1-year and 30-year Treasury bonds is moving higher, just as it did coming out of the last two recessions. An increasing spread between short-term and long-term interest rates is a positive for financial service companies, the largest weight in our portfolio. While some investors may be disappointed by reduced dividends and share repurchases during the crisis, we are supportive of actions that further improve the already strong capital levels at the banks in which we’re invested. We believe the industry is in far stronger shape than during the 2007-09 Global Financial Crisis. As investors gain increasing confidence in economic recovery, we expect higher long-term interest rates and higher financial service stock prices.

For further evidence of improvement, we will be closely watching the Institute for Supply Management’s Purchasing Managers Index (PMI). If the Index moves into positive territory, as some early indicators suggest, value stocks could start roaring. The last times we saw such acceleration (2013 and 2016), our portfolios produced particularly strong absolute and relative results.

Outlook – Uncertainty Likely to Create Volatility

The market, as measured by the S&P 500, has come a long way in a short period of time. That said, the gains have not been universally enjoyed and value stocks, in particular, seem to offer relatively better risk/reward ratios as compared to the many growth stocks that are increasingly important to the S&P. Given current valuations, the S&P may well end the year somewhere near current prices, but the path could be bumpy, with significant sector rotation under the surface. The list of factors potentially causing volatility between now and year’s end includes, but isn’t limited to:

- Economic releases – signs of acceleration or malaise?

- COVID – case growth, hospitalizations, and news regarding treatments/vaccines

- November elections – shifting poll numbers could easily move markets

- Relations with China – will the President use harsher rhetoric to improve his reelection odds?

At Poplar Forest, we view volatility as an opportunity to buy low and sell high. At the market low in March, we were very active on the buy side of the ledger. As the market recovered, we eliminated four stocks from the portfolio: Carnival Corp, Darden Restaurants, Hewlett-Packard Enterprises and United Parcel Service. Of these sales, Carnival and Darden were both relatively new investments for us.

We invested in Carnival, the leading cruise company, in late 2019 and early 2020 at prices that we believed reflected recessionary earnings. That said, our recession analysis assumed a garden variety downturn, not a complete halt in sailings. While the stock continues to look cheap on an asset value basis, the company is burning cash every day and we are concerned that COVID will be particularly impactful to a business that serves an older demographic in closely confined spaces.

Darden was an even newer investment that we made during the March market meltdown. The stock fell to a level that we believed offered three years of potential returns well in excess of our 15% annual hurdle rate as diners returned to their restaurants. As it turned out, we didn’t have to wait three years. After a rapid recovery, the stock no longer appeared to offer prospective returns consistent with a top 30 idea, and we sold it. This is a perfect example of how market volatility can create opportunity.

We are currently invested in 31 companies. The portfolio is skewed towards deep value stocks (Financials 22%) with roughly 30% exposure to more defensive investments (Healthcare 18%). We have a cash position of roughly 5% and a heavily-researched list of stocks we’d like to buy if the market gives us an opportunity to do so at what we consider to be attractive prices. With our portfolio valued at near-historic discounts to the S&P 500, we see potential for at least 50% relative upside once investors are comfortable that COVID is under control and that the U.S. economy is again cooking over a self-sustaining fire.

I hope you enjoy a happy and healthy summer,

J. Dale Harvey

1 The Partners Fund portfolio trades at a 38% discount to the S&P 500 Index based on p/e as of 6/30/2020.

Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.