Dear Partner,

Before falling in love with investing, I was infatuated with politics. I remember my elementary school teacher telling us that my home state of Virginia was the mother of presidents. As a child, I imagined someday sitting in the Oval Office. This admittedly audacious idea came to me quite naturally as political affairs were a much-discussed topic at our family dinner table.

During my freshman year in high school, this interest in public service culminated in my serving as a page in the Virginia General Assembly. For three months, I had a front row seat to the messy process of turning bills into laws. Being a page required living in a hotel in downtown Richmond. Though we had chaperones and study hall, when we weren’t working in the Capital, we were largely left to fend for ourselves. My friends back in Bedford (population: 6,000) didn’t understand the appeal. Why would I give up home cooked meals and the excitement of the high school basketball season? They thought the idea of living in a hotel sounded weird and lonely; I thought it sounded exciting.

High school may be the ultimate time that peer pressure exerts its homogenizing impact, but I resisted. In this case, being different had its rewards; I learned about independence and the inner workings of government. And I got paid! I used the $1,000 stipend to buy 10 shares of IBM and 20 shares of American Medical International. My career aspirations shifted from public office to investing.

Why is this story on my mind right now? Because in the 38 years since I made those first investments, there have been times when being a contrarian, value investor has left me feeling as alone as a fourteen-year-old living far from home. We’re currently living through one of those lonely periods.

Value Investing is Currently Unpopular

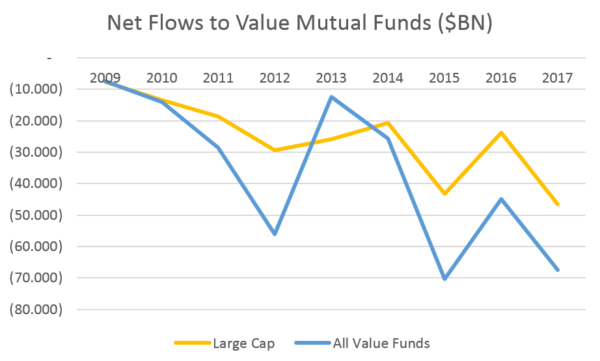

I suppose it isn’t surprising that value investing is about as popular as the Los Angeles Lakers these days. Value stocks failed to provide downside protection during the financial crisis and they lagged behind growth stocks in the recovery. From 12/31/2006 through 12/31/2017, growth stocks, as measured by the Russell 1000 Growth Index, increased in value by 190%, the S&P produced a 138% gain and value stocks, as measured by the Russell 1000 Value Index, generated a 98% return. As a result, some investors have been trading their value investments for growth stocks and index funds.

Source: Investment Company Institute

Times like this are a true test of conviction. Does your investment manager stick to his or her process when times are tough, or do business imperatives cause them to drift? Sadly, too many managers worry about being out of sync, so they chase what’s currently popular. As the Wall Street Journal reported on June 5:

“Hunting for cheap stocks has been out of favor for so long that some self-proclaimed value investors are stepping outside their mandate and buying faster-growing tech stocks, a move that could be costly should the economy start slowing.

“These buyers have drifted away from the hallmark of value investing championed by the likes of Benjamin Graham and Warren Buffett: actively picking stocks the market has overlooked.”

— from Value Investors Step on Gas as Tech Stocks Surge Further

While our competitors may waver, Poplar Forest has not and will not drift away from value investing!

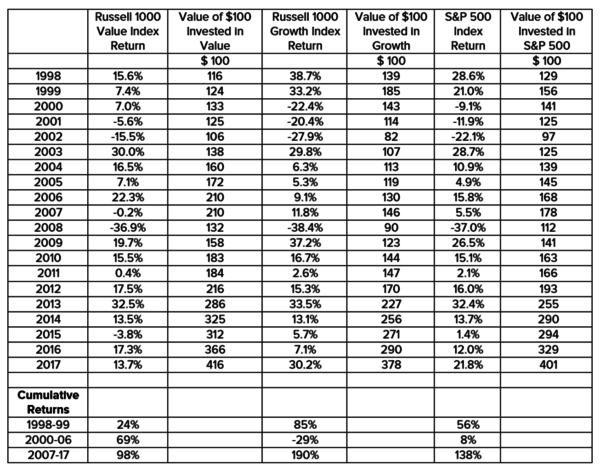

At Poplar Forest, we continue to believe that contrarian value investing provides the potential for market-beating, long-term returns. Despite growth stocks performing better over the last 10 years, value still had an edge over the last two decades. For example, in 11 of the last 20 calendar years, value beat growth (as measured by the Russell indices) and the cumulative return of value was superior. A hypothetical $100 invested in the Russell 1000 Value Index on 12/31/1997 would have been worth $416 on 12/31/2017 as opposed to the $378 produced by the Russell 1000 Growth index.

Source: Evestment

In some ways, the current environment is beginning to feel like that of the late 1990s. Tech stocks were the market darlings then, just as they are today. The valuation gap between tech and everything else isn’t as large, but the performance of e-commerce stocks in recent years feels eerily similar. I was a new portfolio manager when the tech bubble was inflating and I distinctly remember one of my peers pressuring me to buy some tech stocks to reduce my “tracking error.” Just like in high school, I resisted the peer pressure. I couldn’t find any tech stocks that met my risk and return hurdle rates on a normalized earnings basis and I wasn’t willing to compromise my investment process.

Although it was a lonely position to be in, I stayed with what were then referred to as “old economy” stocks that were trading at a substantial discount to the market. Though I didn’t yet have the experience that I have today, I believed that my process would be a long-term winner and I stuck to my playbook. Those two years, 1998 and 1999, were terribly frustrating, but I had tremendous support from veteran managers who encouraged me to stick with my convictions. Their advice proved prescient when the tech bubble burst in 2000.

Over the last three decades, I’ve learned that value investing:

- is hard – at times it feels like running into a burning building that others are fleeing.

- demands imagination – to see the feathers of the phoenix in the rubble.

- requires patience – it can take time for the market to see what we see.

- isn’t sexy – but historically it has been a good way to beat the market.

Poplar Forest’s Selective Approach to Value

While I consider the Russell 1000 Growth and Value Indices to be good indicators of the investment climate, I find their approach to be “naïve” – they attempt to simply divide the 1,000 largest stocks in the U.S. between statistically cheap value stocks and those deemed to be growth stocks because they aren’t cheap. While this naïve approach to value investing has beaten growth over the last two decades, we believe that we can do even better by being selective.

As longtime readers of this letter know, in building our portfolios we seek:

- Investments in which expectations are low. (These can create positively skewed risk/reward ratios. And even a reduction in bad news can generate positive stock price action.)

- Investments in which we understand the sellers’ perspective. (A stock can be cheap for good reasons.)

- Investments in which time is on our side. (These would include businesses we could imagine owning for a decade, with strong balance sheets and consistent free cash flow.)

In seeking to identify our best ideas, we perform thorough, independent, fundamental analysis that aims to determine where consensus thinking may be off base. Our weekly meetings involve rigorous debate in order to identify risks as well as potential rewards. It is a multi-stage, iterative process that involves experienced, dedicated professionals who have invested their own money alongside each of you.

Our selectivity leads to concentrated portfolios of our best ideas, and that concentration tends to magnify the performance of the naïve Russell 1000 Value Index. For example, in 2016, when value beat growth, Poplar Forest did better still; likewise, in 2017, when value lagged, our results were even more challenged. We believe this pattern of results is important for current and potential clients to understand as it could have implications for future results in an environment when value investing comes back into fashion. In short, when that happens, Poplar Forest clients have the potential not just to win, but to win big.

Value Versus Growth/Momentum

Investment concepts need not be limited to financial markets. Though I remain a Los Angeles Laker fan, I’ve been fascinated by the recent success of the Golden State Warriors. I find their story to be a real-world analogy to our business – one that highlights the difference between currently unpopular value investing and the now fashionable growth/momentum approaches to managing money.

In 2010, Joe Lacob and Peter Guber led an investment group that paid a then-record $450 million for the Warriors. The fundamentals looked typical for a value investment – over the prior decade, the team had only two winning seasons. While there had been NBA championships in 1956 and 1975, futility was more common – since starting as a professional ball club in 1947, they had lost 2,705 regular season games while winning just 2,293. Anyone looking in the rearview mirror would see a bleak picture. But the new owners didn’t extrapolate the past into the future. They saw things differently. They planned to rely on research and analysis and to vigorously debate their ideas. In deciding to exploit an opportunity – the under-used three-point shot – they believed that probabilities would prevail over conventional wisdom.

Their new approach got off to a rough start: their newly hired coach was fired after a year. In that year, the team lost 56% of their games. The next year was worse – the team lost 65% of the time. A second head coach was a little more successful, but he was replaced after just three years on the job. The team was playing better, but they were still only about average for the league – not the type of results that would justify the owners’ investment. Then the club settled on rookie coach Steve Kerr. Kerr had had great success as a player in winning three championships with the Chicago Bulls and two more with the San Antonio Spurs. He was a great outside shooter who had, at one time, the career record for making 45% of the three-point shots he attempted. What a perfect match for a team with under-utilized shooters in Steph Curry and Klay Thompson. In his first season, Kerr set the record for most wins by a first-year head coach. The team won its first title in 40 years!

After three NBA titles in four years, the Warriors are no longer a value story. Odds makers in Las Vegas predict they’ll be champs again next year. Winning means money: Forbes recently estimated the team to be worth $3.1 billion – almost seven times what the investor group paid just eight years ago! In stock market terms, the Warriors have transitioned from being a value investment into a momentum idea.

Momentum investments are predicated on a belief that winners will keep winning. For most of the last decade, this investment approach has delivered market beating results while value strategies have lagged. In a sense, the two approaches are philosophical opposites. In contrast to believing that winning stocks will continue to outperform, value investing often involves buying stocks after they have fallen in price. This is based on the belief that investors have excessively penalized the company for what may be short-term concerns. It can be quite financially rewarding when these perceived “losers” ultimately become “winners” again.

Many of the best performing stocks in the market over the last decade have been wonderful businesses, but price matters. For example, when Lacob and Guber bought the team in 2010, the pre-season odds of a Golden State championship were 185-to-1. The team was decidedly “out of favor,” and rightfully so. By the start of the 2014 season, the team had clearly improved and the odds were down to 25-to-1. That turned out to be good value when they won their first title in 40 years. Today, after the Warriors’ recent successes, the Vegas line setters are offering 5-to-4 odds. In practical terms, these odds suggest the Warriors have a 4-in-9 chance of winning a fourth title in five years. From my value-focused vantage point, this looks like an expensive wager.

To win another championship, the Warriors will have to make it back to the finals for the fifth consecutive year. In the history of the NBA, only six teams have made it to four or more consecutive finals appearances – and only one of those six (the Boston Celtics) made it five times in a row. Perhaps the Warriors will confound historic odds. Perhaps they are a new basketball dynasty that will upend the record books. It’s certainly possible, but history suggests the 5-to-4 odds currently offered in Vegas do not offer a good tradeoff between risk of loss and reward. It’s easy to forget how close the Warriors were to not making the playoffs this year. At one point, they were down 3 games to 2 against the Houston Rockets and they lost one of their best players to injury.

While I don’t know when or how the Warriors’ finals streak will end, I know that it will someday end. How very appropriate, in a market environment favoring tech stocks over just about anything else, that the basketball team closest to Silicon Valley has achieved this air of invincibility. In the same way, I don’t know when the market’s love affair with growth stocks will end, but I believe that most everything in life is cyclical and that value will eventually have a chance to again hold the championship trophy.

“It’s not easy to do what’s unpopular but that’s where you make your money. Buy stocks that look bad to less careful investors and hang on until their value is recognized.”

– John Neff

In Closing

I was fortunate to have found my vocation at an early age. While in Richmond at age 14, I learned that getting elected meant keeping constituents happy – it required popularity. I wasn’t suited to that type of job. Instead, I settled on one that required rigorous, but dispassionate analysis – a career in which the well-thought-out yet lonely idea can be rewarded. A profession that not just allows, but actually requires going against the grain – provided there is a well-grounded reason to support the unpopular position. As Benjamin Graham, the father of value investing said: “In the short run, the market is a voting machine, but in the long run, it is a weighing machine.”

With the economy now in one of its longest expansions ever, and with the stock market near all-time high levels, I know that many investors have grown worried that recession, trade wars, rising interest rates and/or a geopolitical mishap could trigger a bear market in stocks. While others may be worried about these macroeconomic issues, we continue to focus on the company-specific research that we believe gives us an edge. Through that lens, we aren’t worried — we’re excited. We believe that stock prices follow earnings in the long run. Our research suggests that the companies in our portfolio appear to offer above average earnings growth, driven primarily by improving profitability, yet they trade at a substantial discount to the S&P 500. We believe that free cash flow and buying at a discount to intrinsic value will ultimately outweigh popularity and momentum.

We couldn’t invest for the long term without client partners who understand that while value has worked well in the long run, it doesn’t work every year. While our recent results haven’t met our expectations, like the Warriors at the start of the 2013-14 season, we believe that our investment process and our talented team of professionals have us poised for a multi-year championship run. In 2016, we saw what could happen when sentiments shifted. And while we don’t know when this cycle will turn, we feel confident that, at some point, it will. If past is prologue, when the turn comes, we may be particularly well positioned. We will stick with our game plan because we believe that contrarian value investing can deliver market-beating, long-term returns for those with the patience to see it through to fruition.

Thank you for your support and trust,

J. Dale Harvey

July 1, 2018

Appendix – Value Versus Growth

Value better than Growth in 11 of the last 20 years: 2000-2006, 2008, 2012, 2014, 2016

Earnings growth is not a measure of a Fund’s future performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.

Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.