Dear Partner,

In the small town where I grew up, having your own car seemed like a path to freedom and happiness. I suppose that’s why my father refused to allow me to buy one. As he saw it, a car would lead to girls and drinking and he feared my schoolwork would suffer. I did get to drive my mother’s old Pinto station wagon to school and work, but it certainly did not attract girls. There was an upside; my parents promised to buy me a car if I achieved a 3.0 or better in my first year of college.

As we loaded my belongings into my father’s pickup truck at the end of freshman year, I noticed new license plates on the dashboard that read “J DALE” – I was getting a car! The details were withheld until we got home. After we unpacked the truck, Dad took me to the machine shop where my reward was being repainted. That 1973 Chevy Caprice Classic convertible was a thing of beauty – fire engine red with a white top. Admittedly, it was 11 years old and got maybe 8 miles to the gallon, but it could also seat 6-7 people comfortably. Needless to say, it was a hit when I rolled into the fraternity parking lot for the start of my second year at school.

My love affair with that car sadly ended when I graduated. I was headed to New York City and having a land yacht in Manhattan just wasn’t practical. Besides, I needed the money. So I sold my beloved red convertible. Four years later, the situation had changed – I was approaching the end of graduate school in Boston and would soon be moving to Los Angeles for a job – I was going to need a car.

There were 12 inches of snow on the ground on that late March day when I headed out to find a used red convertible I could afford. The Chrysler salesman could hardly believe his ears. “Sure'” he said, “you can take the used La Baron for a spin.” It was freezing cold, but I still put the top down for the test drive. The car had been on the lot for months and there weren’t many prospective convertible buyers in late winter in Boston. They were so anxious to sell it that they gave me a great price. What’s more, they let me put the down payment on my credit card, financed the rest, and agreed to make the first two payments. In the intervening 25 years, I’ve owned a succession of red convertibles with “J DALE” plates. Though I’m always sensitive to price, I’ve never gotten as good a deal as I did on that cold winter day.

I wouldn’t call myself a “car guy”, but I love to cruise down the highway on a sunny day with the top down and great tunes playing. I have a hard time imagining myself in one of the driverless vehicles that are getting so much press these days. Automobiles have become ever more sophisticated for decades and I suspect Henry Ford would be amazed at what is packed into today’s new vehicles. I really appreciate my car’s navigation system and rear view camera, but I’m not ready to give up the wheel. While I acknowledge a computer directed vehicle may be safer than one piloted by a distracted driver, isn’t a better solution to eliminate distractions?

Just as new technology has improved the driving experience, innovation has also improved investors’ returns. Index funds have now been around for 40 years and they have certainly saved clients’ money while avoiding the underperformance that can come with a poorly managed mutual fund. Index funds have given rise to new investment vehicles like ETFs (exchange traded funds) which allow investors to

buy and sell baskets of stocks at any minute of the trading day. Index funds have also grown more sophisticated with “smart beta” and “factor” based portfolios available to those wanting to slice the market different ways. Most of these new investment choices are lower in cost because they don’t rely on humans for decision making. Just as a computer directed car may be safer than one steered by a distracted driver, computer orchestrated investing may produce better outcomes than poorly managed mutual funds. For many investors, simply getting an “average” return is an improvement; I’ve always strived to do far better than average.

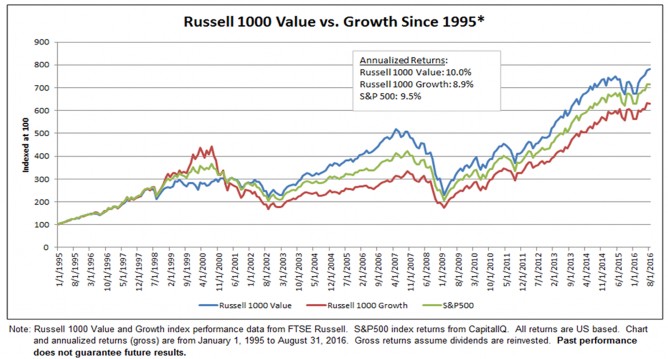

Though it doesn’t work every year, value investing has demonstrated an ability to deliver market beating results over long periods of time, as you can see above. We believe the current environment offers a particularly compelling opportunity for value stocks. The general premise is simple: statistically cheap stocks reflect low expectations. If the future turns out to be better, which can often happen when expectations are low, then the stock will often move higher. As a contrarian value investor, I’ve watched with interest the development of factor based ETFs like the iShares Edge MSCI USA Value Factor ETF. That fund’s prospectus states that it “seeks to track the investment results of an index composed of U.S. large- and mid-capitalization stocks with value characteristics and relative lower valuations.” The supporting documents summarize the stock selection process as “combining the z-scores of the three valuation descriptors, namely Forward Price to Earnings, Enterprise Value/Operating Cash Flows and Price to Book Value.” BlackRock, the sponsor of the Value ETF, charges 0.15% per year for a fund that seeks to merely track the performance of an index of value stocks. While “combining z-scores” may sound impressive, I think Poplar Forest’s active investment process may produce index-beating returns after expenses.

How We Steer Our Portfolios

We have access to the same type of data used in the creation of the MSCI USA Enhanced Value Index, but we don’t just buy a stock because a computer algorithm says to. Computers may be good at identifying statistically cheap stocks, but many of those stocks are cheap for good reasons. For example, as of June 30, 2016, General Motors and Ford accounted for 5.4% of the iShares Value ETF. We acknowledge that those stocks look cheap, as they are trading at around 7x earnings, but we worry that their profits may decline from here given U.S. auto sales are at all time high levels.

At Poplar Forest, we’re focused on delivering results that can’t be replicated by a computer algorithm. We spend our time investigating companies with the goal of distinguishing the “cheap for good reason” from the real bargains (like a red convertible on a cold winter day). We spend a great deal of our time evaluating businesses that have produced disappointing results – the proverbial car with a wheel in the ditch. Sometimes disappointing results signify a broken axle, but occasionally it’s just a blown tire that can be repaired. The share price of a good company suffering from weak short-term results may not look statistically cheap, but when the business is fixed and results improve, that out-of-favor purchase may end up looking like a real bargain in hindsight.

During the recent quarter, for example, we invested in Ralph Lauren, whose stock had declined 50% from its high in late 2014. In prior years, management had wanted the business to grow at what turned out to be a higher than prudent rate and, as a result, they introduced too many new products. An impressive new management team was recently hired to clean up the resulting mess. The new team quickly decided to simplify the product line which resulted in reduced sales this year. Profits declined as revenues fell. This company has enjoyed profit margins of 15% or more for years, but the repositioning of the business has resulted in currently depressed margins of just 10%. As this turnaround takes hold, we expect revenues to start growing again and margins to recover to prior levels. If we are right in our assessment of the company’s outlook, margin expansion alone seems sufficient to drive a mid-teens earnings growth rate over the next three years. Sales growth and the deployment of free cash flow will hopefully add to that growth rate. With a P/E ratio roughly in line with the S&P 500, the stock doesn’t look like a traditional “value” stock. In our view, the current valuation is misleading because earnings are depressed. We are excited that the margin recovery potential could allow us to earn a better than 20% annual return on our investment in the coming few years.

While many observers fret because the 500 stocks in the S&P collectively look a little pricey and their profit margins look high, our investment process has continued to identify individual companies, like the one described above, that appear to offer far different prospects than the stock market as a whole. The bottom up, research-intensive investment process we use can’t be replicated by computer. It takes a lot of time and effort by our six person investment team to find, analyze and stay current with our investments, but since we limit ourselves to high conviction portfolios of 25-35 individual stocks, it works. As a practical matter, once we’ve invested in a company, we tend to own it for about four years. With roughly 30 stocks and an average four year holding period, we need just 7-8 great new ideas a year to keep our funds running on all cylinders. I’m thrilled to work with a great group of patient, talented, and

experienced professionals who believe in what we do and who’ve all joined me in investing their own hard-earned money in our funds.

I started investing in stocks when I was in high school. In college, I dug into the work of Graham and Dodd (the original proponents of buying statistically cheap stocks) and John Neff, a legendary value investor. I also studied Warren Buffett who built on Graham and Dodd’s work by demonstrating that value is more than just buying statistically cheap stocks: a bargain can sometimes involve paying a little more for a good business with above average prospects – provided those prospects are under- appreciated by the market. This foundation combined with first hand exposure to great portfolio managers at the Capital Group/American Funds led me to develop an investment process I’ve now been using for more than 20 years. My goal: market-beating, long-term investment results.

Judging the success of an investment strategy isn’t as easy as you might believe. The biggest challenge is in distinguishing stock picking skill from general market movements. Sanford Bernstein, a Wall Street research and investment firm, recently tried to tackle this challenge in a newly published study entitled “What is Worth Paying For in an Asset Manager.” Their work systematically dissects a fund’s investment results into “factors” and “idiosyncratic alpha.” The “factors” (value, momentum, quality, and low volatility) can be cheaply replicated by a computer directed ETF. The “idiosyncratic” piece can’t be explained by an algorithm – it’s the piece of the puzzle that truly reflects human inputs. That’s what we do at Poplar Forest: we pick stocks based on more than numerical data by employing our own qualitative analysis and judgment.

We asked Bernstein to use their system to evaluate the Poplar Forest Partners Fund. Unsurprisingly, our historic results were highly correlated with the “value factor” – in other words, we are value investors. Beyond that, Bernstein found that, in their study period of March 2011 through June 2016, the fund demonstrated statistically significant “idiosyncratic alpha” (excess return relative to a benchmark) of roughly 3.6% per year (before fees) relative to an equal weighted basket of the four factor ETFs. For over 20 years, I’ve believed that my investment process would produce market beating returns and now Bernstein has produced statistically significant evidence that it has. For more details on their methodology, please see Bernstein’s report: “Fund Management Strategy: Examining Idiosyncratic Returns in the US Market.”

The Road Ahead

Bob Kirby, a former Capital Group colleague and an outstanding money manager, was also a passionate race car driver. He often noted that racing and investing are similar in that, as he put it, “You have to finish to win.” That mindset has long been a part of my investment process as expressed in self-imposed restrictions to build portfolios with at least 85% dividend paying and at least 85% investment grade rated companies. Focusing on sustainable free cash flow and on the price paid relative to the perceived value received are also factors that I believe help ensure we “finish the race.”

At this point in the economic cycle, and with the stock market near all-time high levels, protecting against downside risk is a growing factor in our investment process. As a first step, and as a measure of increased conservativism, we are building a 2018 recession into our base case financial forecasts. We don’t currently see the preconditions for a recession, but we want to make sure that we have our eyes open to the potential downside risks in the portfolio in case a recession develops unexpectedly. If the economy continues to grow as we expect, the results generated by the companies we invest in could be even better than forecast. In addition, we recently started a series of internal meetings focused solely on a systematic review of variables that could be early indicators of recession.

Our operating premise is that recessions occur when a sector (or sectors) of the economy is operating at an over safe speed. This was the case with housing in 2005-2007 and technology in 1997-1999. At this point in time, the auto business seems to be running a little hot, but a slowdown there wouldn’t seem sufficient to bring on a recession. More generally, we expect the economy to largely continue on its current path of moderate growth, slowly rising inflation and rolling corrections within particular industries (like energy and industrials recently) that keep the U.S. economic engine from over-heating. Provided the engine doesn’t get too hot, we are likely a long way from needing a recessionary pit stop.

We’ve also considered an environment in which the economy grows at such a slow speed that interest rates stay “lower for longer.” With financial services companies making up a large part of our portfolios, we sometimes get questions about how we’d fare in such an environment. Given the valuations on our core financial service investments, I think we are being more than adequately compensated for the risk of such an outcome. These stocks are valued at around 7-8x earnings and 70-80% of book value. If interest rates remain low, earnings growth will be low, but deployment of free cash flow should allow us to earn a roughly 10% rate of return. If interest rates move back to historic premiums relative to inflation, as we expect, we believe we’ll enjoy far better returns from these investments – in short, the risk/reward ratio seems skewed in our favor.

While we are spending a little more time looking for recessionary road signs, our focus remains on bottom-up stock selection. We continue to be drawn to prospective investments that hinge on “self-help” factors like those involved in the turnaround of Ralph Lauren that I discussed earlier. At a time when many advisors and investors seem understandably nervous about the market as a whole, we have a decidedly different outlook due to our selectivity; we don’t own 500 stocks, or 150 – we build portfolios of 25-35 stocks that we’ve carefully chosen. Our knowledge of the circumstances of company specific factors makes us enthused about the prospects for our portfolio. We’ve enjoyed strong results through the first nine months of this year, and we hope to generate more strong gains in the years to come.

The total return of an investment can be broken down into two key components: fundamentals and valuation changes. We break fundamentals down into organic sales growth, profitability and deployment of free cash flow. When looking at our portfolio relative to the broad market, we believe improved profitability will be the key driver of our results in coming years. We expect profitability improvements to contribute roughly 7% a year to the weighted average EPS growth of companies in the Partners portfolio in 2017-2020. On top of that, we assume revenue growth consistent with a slow growing economy and a modest contribution from the deployment of free cash flow. If we are correct in our assessment, the companies in our portfolio could produce double digit annual earnings growth in the next three years. This growth, combined with a reasonable dividend yield and a discounted valuation relative to the broad market, may be a recipe for market-beating results.

We appreciate the patience of our client partners who understand that even great investment processes don’t beat the market every year. So far, 2016 has been a year in which your patience has been rewarded. Of course, we’ve got many miles to go, but in my opinion, the outlook is bright. It’s a beautiful sunny day. The tank is full of gas and Waze (another technological marvel on which I rely) says traffic is light. I’ve got the top down and Tom Petty’s Runnin’ Down a Dream is playing at top volume. There is plenty of room in the car so I hope you’ll settle in and enjoy the ride. I look forward to sharing a long and successful road trip with all of you.

Thank you for your continued confidence in Poplar Forest.

J. Dale Harvey

October 3, 2016

Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.