")

Few people were sad to see 2022 come to an end. From continued Covid challenges, especially in China, to Russia’s Ukrainian invasion, to central bankers’ aggressive response to rampant inflation to the crypto crash, the last 12 months were a tough slog for many around the world. Given these headwinds, it was almost a pleasant surprise to see the S&P 500 “only” fall 18%. To many investors, it felt as if there was no place to hide because both bonds and stocks fell; the last time investors lost money in both asset classes was in 1969. By being down less, Value stocks as measured by Russell’s indices out-performed their Growth siblings for a second year in a row. I think we are still in the earliest phase of a multi-year bull market in value stocks; opportunities seem particularly robust in the “deep” value part of the market — generally the cheapest 20% of stocks.

While the major indexes struggled, our focus on stocks with idiosyncratic characteristics allowed us to deliver a positive total return for the year. Importantly, we had positive contributions from 20 of the 30 stocks we owned at the end of calendar year 2022.

As we crack open our new 2023 calendars, of course, the economy is still dealing with a slight hangover from 2022. Yes, inflation is starting to moderate, but the economy appears not to be fully registering the effects of the Federal Reserve’s aggressive monetary stance. During December, normally the time of a “Santa Claus” rally, investors sold stocks in at least a partial acknowledgement of likely economic pressures coming in 2023. While we have no particular expertise in economic forecasting, we continue to think it prudent to plan for a recession in 2023. Practically speaking, while Wall Street analysts forecast growing earnings for the companies in the S&P 500 in 2023, we expect profits to fall. We are keeping our eye on a growing list of economically-sensitive stocks that we may want to buy if short-term oriented investors get overly focused on falling earnings.

Everyone knows that even the best businesses have good and bad years. We don’t pin our expectations to either extreme, but to our educated assessment of each company’s likely normalized earnings and free cash flows looking out three to four years. When investors become overly focused on either boom-time or recessionary results, our differentiated investment time horizon may allow us to sell into the euphoria evidenced by high prices or to buy into the pessimism of recessionary selloffs. We are patient and price sensitive in assessing new investments and believe that our absolute valuation paradigm helps counter cycles driven by investors’ emotional swings. While we made no new investments in the third quarter, during the fourth quarter, the market’s zigs and zags gave us the opportunity to initiate four new investments while liquidating three of our lower conviction holdings.

New Investments

Of the four new investments we made, we were able to build one of them – Dow Chemical – to a full position during the quarter. As you know, we build positions in “scoops” to help manage the risk of being too early. That means that even in the best of circumstances, it takes more than two months to build a full position.

Dow Chemical – In the 125 years that Dow Chemical has been in business, the company has seen tremendous change and transformation. While still a company impacted by cyclical commodity chemical markets, the company has been focused on higher-value end markets that should allow it to generate very compelling full-cycle returns on capital. After earning close to $6.50 in 2022, we expect a recession to drive earnings down to around $3.50 in 2023. At roughly $50 per share, the stock looks very attractive to us at roughly 14x depressed results while sporting a better than 5.5% dividend yield and an investment grade-rated balance sheet. The ability to generate free cash flow during a recession is a characteristic that gives us confidence that if the recession is deeper or longer than we have assumed, the company will have the financial strength to make it through the cycle in fine form.

Looking out a few years, Dow Chemical’s earnings should improve to levels that may substantially exceed 2022’s tally. While we are using a more conservative outlook in our assessment of the stock, if management delivers on its plans for the business, earnings could exceed $10 per share by 2026. In summary, the shares appear to offer prospective returns in excess of our absolute return hurdle while providing upside optionality and dividend support that may minimize downside potential. Said another way, the ratio of reward to risk seems decidedly skewed in our favor.

As long as we can continue to find what appear to be bargains like Dow, then the value cycle is likely far from over. We have identified at least a half a dozen potential investments that may offer prospective returns comparable to our new investments. I continue to be very excited about the prospects for our portfolio, not just based on valuation and the growth potential of the companies we own, but also on the potential opportunities to continue to improve the risk/reward ratio in coming months.

The Three Stages of a (Value) Bull Market

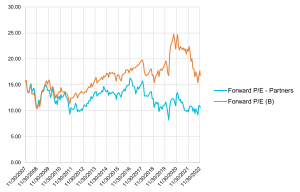

When it comes to Value stocks, I’ve recently heard some muttering along the lines of, “The stocks have been so great over the last couple years that the cycle is probably over. Too bad I missed it.” I couldn’t disagree more. Not only have the last two years of outperformance followed a decade of growth stock dominance, but, in my experience, investment cycles rarely end after just two years. I think cycles are best measured by valuation, investment opportunities, and investor attitudes. This Value Bull Market may well continue as long as we can continue to find cheap stocks and there is skepticism about the continued out-performance of Value. On the first point, our portfolio is currently valued at slightly more than 10x consensus 2023 earnings while the S&P 500 is trading at close to 17.5x. A gap of that magnitude remains historically wide. Not only are our stocks cheap in absolute terms, but the discount to the broad market remains substantial.

Source: Standard $ Poor’s/ Capital IQ

In addition to historically wide valuation differentials, investor skepticism remains high. In a recent podcast interview, Howard Marks, a great long-term investor and the founder and Co-chairman of Oaktree Capital, described market cycles in a way that I found to be quite apt. He talks about the three phases of a bull market and I believe his characterization applies perfectly to the Value Bull Market that I believe we recently entered.1

First, the setup according to Marks: “There has been a correction… stocks are down here and they’ve done terribly for some period of years and everybody has deserted them.”

Well, that certainly applies to value stocks, not just in the four terrible years of 2017-2020 when the Russell 1000 Growth Index produced a cumulative 142% while the Value Index returned just 36%, but more broadly in the entire post GFC period from 12/31/2008 through 12/31/2020 when Growth beat Value by almost 7% per year. Given these performance differentials, and with FAANG stocks in the headlines, some Value managers felt pressure to add at least a few growth stocks to their portfolio while also migrating closer to their benchmarks. Though the pressure was intense, at Poplar Forest, we stuck to our absolute value discipline, even though we sadly lost a few clients due to results that “lagged the benchmark.”

Marks continues: “The first stage of the bull market occurs when only a few, intelligent and unusually far-sighted people, hopefully mavericks, begin to believe that there could be improvement.”

This sounds like a good description of where we are now. During 2022, the Poplar Forest Partners fund had a net inflow of funds for the first time in six years, but at a level that is still a fraction of what we received prior to 2017.

Marks concludes: “The second stage occurs when most people accept that improvement is actually taking place. And the third stage is reached when everybody and his brother thinks that things can only get better. And clearly, if you buy in the first stage you make a lot of money as it transitions to the third stage, but if you buy in the third stage, you lose a lot of money when that optimism turns out to be unwarranted.”

I continue to think that, because we are in the first stage of a Value Bull Market, there is the potential for a lot of money to be made by investors who are willing to invest with us well before the market transitions to stages two and three. Another famous investor, Sir John Templeton, put it succinctly: “Bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria.”2 To me, it feels like we are right in the beginning of the transition from pessimism to skepticism.

I’ve seen a cycle like this before. My experience as a portfolio manager started in the late-1990s, another period of poor results and rampant pessimism about value investing. Warren Buffet was being labeled a dinosaur because he shied away from the tech stock enthusiasm that was driving the markets. I was in my early 30s and using the same investment process I use today. I had a portfolio of Value stocks that traded at wide differentials to the broad market and I didn’t own any tech stocks. My peers kept telling me that I was taking too much risk by not owning a least a few tech stocks, but I just couldn’t stomach the idea of buying something at 40x earnings because it was relatively cheaper than a competitor trading at 80x. I thought they were all too expensive, so I stayed away.

When sentiment turned in Value’s favor, the cheapest stocks in the market out-performed their more-expensive, higher-growth siblings for seven years in a row. That experience solidified my commitment to the contrarian, absolute approach to value investing that I continue to believe can deliver market-beating, full-cycle investment results. Yes, the period from 2017-2020 was bracing, but we didn’t deviate from our process. Now, once again, our discipline and patience has begun to be rewarded and I believe the future is very bright.

The Year Ahead – Volatility Likely to Continue

I continue to be optimistic about the return potential of our portfolio, not because I have a strong opinion about the outlook for the economy or the stock market as a whole, but because of the growth potential of the companies we own and their valuation metrics. Beyond that, we believe that short-term recessionary concerns may give us opportunities to further improve the risk/reward ratios in the portfolio. That said, we believe selectivity will again be the watchword for 2023.

Our bottom-up research process is identifying an increasing number of opportunities in economically-sensitive businesses. In some cases, the stock prices of these businesses are coming close to reflecting recessionary downside. Given the number of opportunities we are seeing in the cyclical side of the market, we are looking for those businesses that appear to offer idiosyncratic opportunity in addition to cyclical recovery potential. In an environment where it seems that stock market commentators are increasingly arguing over who is most bearish, it may soon be time to start looking at the glass as half full.

As I think about the future, a handful of observations suggest room for optimism. First, there has been a dramatic reduction of speculative fervor: the meme stock craze has come and gone, ditto the SPAC fad, and finally, the crypto bubble has lost an awful lot of air. Meanwhile, while the Fed’s balance sheet is still far too big for my liking, their bond portfolio is now slowly shrinking and the days of seemingly “free money” have likely passed. Inflation is starting to come down and I suspect we’ll see the Fed back away from hawkish behavior sometime during 2023. We do have to get through a cycle of negative earnings revisions, but the bulk of that could occur in the first few months of the year. After that, bluer skies could be ahead.

Historically, the stock market bottoms during recession and I would not be surprised to see that happen in the first half of 2023. I am hopeful that by this time next year, we’ll have been through the worst of the down cycle and that we may in for more rewarding times.

Many of you reading this letter have been Poplar Forest clients for years and we greatly appreciate the support you showed us during Value’s dark days of 2017-2020. If past is prologue, we won’t have to live through something like that again for another 15 to 20 years. In the meantime, we continue to build our portfolio from the bottom up, by looking for stocks that meet our absolute return criteria and that we believe offer modest downside. To me, it feels like the Value Bull Market has just begun and we are excited about the opportunities in front of us.

Sincerely,

J. Dale Harvey

Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.