Dear Partner,

Since my last letter to you, the market narrative hasn’t changed much. On the margin, investors are less worried than they were three months ago as evidenced by the S&P 500’s 9% gain in the fourth quarter. But growth stocks have, yet again, outperformed value investments (Russell Growth +11% vs. Russell Value +7%) and companies deemed “safe” continue to trade at historically wide price premiums to low P/E stocks. The environment continues to remind me of the late 1990s – the period that preceded an eight-year run of outperformance for value stocks. How value managers approach stock selection will impact their performance when the value cycle turns. Poplar Forest is not a typical value manager and we believe that our different than average approach will produce far better than average results when investor sentiment shifts in favor of value stocks.

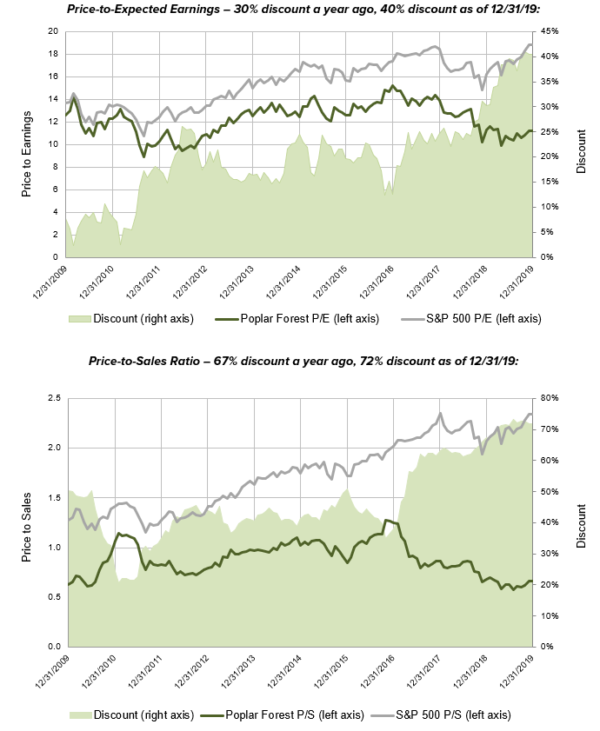

At roughly 11x estimated earnings and with a 3.2% dividend yield, the companies we own continue to be priced at attractive absolute levels and at historically wide discounts to the market despite offering market-like earnings growth prospects. Whether we compare ourselves to broad market indices (S&P at 18x, Russell Value at 15x) or to other value managers (Peer average 15x), we offer differentiated portfolios of what we believe are incredibly compelling investment opportunities.

While low P/E stocks are often expected to deliver below average earnings growth, that isn’t the case for our portfolios. The consensus opinion of Wall Street analysts is that S&P 500 earnings will grow by 7.3% next year while our companies are expected to grow at a much faster rate of 15.9%. Despite better short-term earnings growth and comparable long-term growth expectations, our investments are valued at an historically high 40% discount to the S&P 500. The catalyst needed to close this yawning gap in valuation could be actual earnings growth that meets or beats expectations. We continue to believe that a massive value cycle marked by such catalysts is coming.

Despite the market reaching new highs, we have continued to find new investments that we believe improve the already attractive risk/reward ratio of our portfolios. We liquidated a couple of investments in the fourth quarter and redeployed those funds into two new investments that are trading at or near record low valuations and that appear to offer compelling long-term appreciation potential. The companies have a track record of returning free cash flow to shareholders and both stocks offered dividend yields of at least 4% at the time of our initial investment. We ended the year with 30 investments and a cash reserve of roughly 5%.

More generally, the investing backdrop looks positive given the Federal Reserve’s three interest rate reductions and its massive increase in liquidity in support of money markets. Companies continue to hire workers at rates that exceed the growth of the labor force and the unemployment rate remains at an historic low. Trade war influenced softness in industrial activity seems to be dissipating and overall economic fundamentals look solid.

Issues that could threaten this positive outlook are trade policy and politics. While we remain optimistic about the investment environment, we will be carefully monitoring unemployment claims, the Conference Board’s Leading Economic Index as well as the poll numbers of the many presidential candidates. That said, we will remain focused on a bottom-up investment process that continues to seek stocks that we believe offer compelling absolute value and attractive ratios of reward as compared to risk.

Absolute Value versus Relative Value

In a world where investors continue to increase their exposure to index tracking strategies, I believe our differentiated approach to value investing will ultimately generate outsized rewards. At its core, our investment process focuses on identifying stocks that we believe have the potential to return at least 50% over three years (15%-a-year compounded). We buy stocks when they appear to be trading at undeservedly low valuations with the idea that we will sell them at fair value based on our assessment of normalized earnings and free cash flow. Not every stock we pick will work out, but I have used this approach for more than 22 years and continue to believe it is a compelling long-term wealth generator.

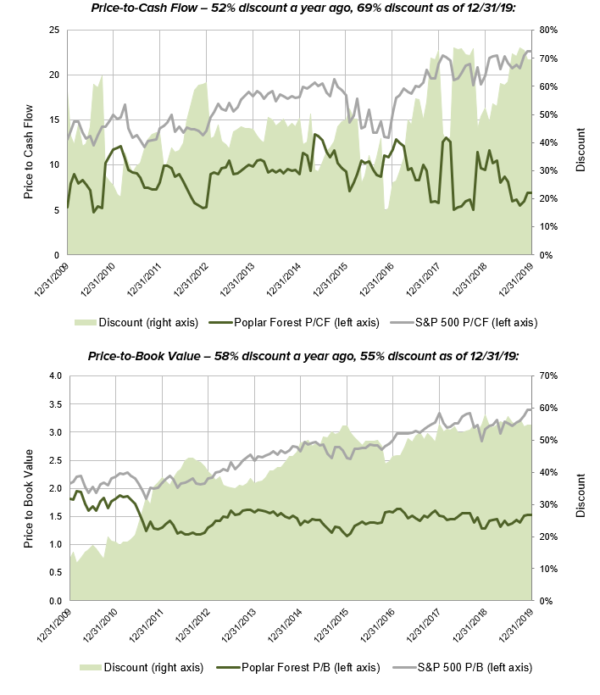

This investment process helps keep our feet firmly on the ground at times when others may let their emotions get the best of them. The following charts compare the valuations of our flagship Partners portfolio relative to the S&P 500. The historically high discounts offered by our portfolios aren’t caused by us doing anything differently; instead, they are driven by a market that has become increasingly expensive over time. Twelve months ago, our stocks traded at or near what were then record discounts to the market; most of those discounts grew even wider as 2019 progressed.

We Aren’t “Closet Indexers”

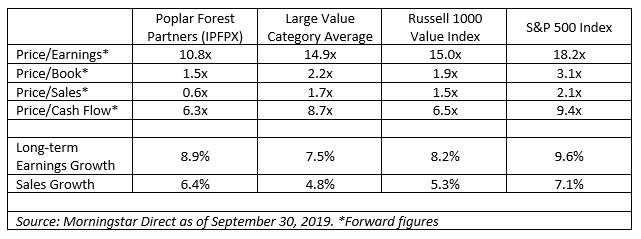

While many of our peers’ portfolios look quite similar to the Russell 1000 Value benchmark, our focus on absolute returns enables us to deliver a truly differentiated value opportunity. When we look at the constituents of Russell’s Value index, we see a lot of stocks that don’t look remotely cheap to us. Someone investing in index-linked or the index-like funds may well be exposed to stocks with outsized downside potential when the next bear market hits. Said another way, a relative value approach may help a manager keep his clients on board as investors chase a rising market, but, when conditions change, those very same clients may unhappily suffer the full brunt of a bear market decline. Our investment process seeks to identify stocks with attractive upside potential while at the same time being cognizant of bear market downside risk. We believe the current heavily discounted valuation of our portfolios offers above average upside potential and below average downside risk. We find a comparison of our portfolio to those of our “peers” to be particularly striking – we offer better growth at lower valuations, according to mutual fund research firm Morningstar:

Portfolio Changes

During the fourth quarter, we made two changes to the lineup of companies in our portfolios. First, we sold our position in natural gas producer Antero Resources and we made a new investment in oil production focused Murphy Oil. Second, we liquidated our investment in dialysis provider DaVita and used the proceeds to buy shares of cruise operator Carnival Corp.

Antero proved to be a disappointing investment as U.S. natural gas prices fell to lower levels than we anticipated. From our vantage point, Antero management is running the company well and volumes will continue to grow at attractive rates in the next couple years, but gas prices are beyond their control. Hedges will protect earnings and cash flow in 2020 and into 2021, but as we looked out beyond 2021, we had less confidence in the cash flow outlook. Given the company’s balance sheet, we thought it prudent to move to the sidelines.

As a replacement, Murphy Oil seems particularly attractive. Like Antero, the shares are trading at around 2.5x projected cash flow and at a substantial discount to book value (a relevant metric for asset-based businesses like energy producers). Unlike Antero, Murphy is currently generating free cash flow and is returning that free cash to shareholders through dividends that produced a yield of over 4% when we started acquiring the shares. Murphy has a differentiated operating strategy that focuses on offshore energy production and its core area of operation is the Gulf of Mexico, where it is now the fifth largest operator (behind Shell, BP, Chevron and Occidental Petroleum). We believe this differentiated strategy, at a time when many energy producers are focused on shale-based resources, will generate far better results than are reflected in the stock’s currently depressed price-to-cash flow valuation. Over the last 20 years, the stock has been valued at over 5.5x trailing cash flow.

DaVita was one of our best performing investments in 2019. When we originally invested, we viewed DaVita as an under-earning business. The problem was a collection of physician practices that the company had acquired. That part of the business wasn’t making money and we saw potential for improvement. In a somewhat unexpected, but positive development, DaVita decided to sell the under-performing business to United Health at what we considered a very full price. That transaction has closed and the proceeds were used to buy back stock such that the share count today is approximately 40% below where it stood just four years ago. At this point in time, we no longer see DaVita as particularly undervalued and we saw much better potential in Carnival.

Carnival, the world’s largest cruise operator, is currently in the midst of a substantial fleet expansion and modernization program which we believe will yield substantial benefits in coming years. Heavy investment in the business has crimped the company’s free cash flow in the short term, but we believe the capital spending will deliver returns well above the company’s cost of capital. Reduced short-term free cash flow and investor concerns about recession have dampened the stock’s valuation. Over the last 20 years, Carnival has been valued at about 15x forward-earnings estimates – today, the shares change hands at around 10x. We believe the company’s capital spending program will produce earnings growth comparable to the broad market, and while we wait for that to occur, we are getting paid a handsome 4.3% dividend yield. As investors grow comfortable with the outlook, we believe the stock can regain its historic valuation.

In Conclusion

Fundamentally, 2019 saw a continuation of recent market trends with growth stocks gaining more than value stocks that were burdened by weak global economic growth and trade war-induced softness in industrial activity. Weak global economies also led to a roughly 15% decline in oil and gas prices as compared to 2018. As a result of these headwinds, economically-sensitive value stocks generated earnings growth that lagged behind their growth company peers by about 9-10% — roughly the magnitude by which growth stocks outperformed value stocks in 2019.

The setup heading into 2020 feels very different. The Federal Reserve has taken an accommodating stance and the President is focused on re-election. While the trade war with China dampened activity in 2019, recent developments suggest the worst of the trade war may be behind us. A president who measures his success based on the level of the Dow Industrials will likely continue a market-friendly White House narrative, at least through Election Day. The ingredients are in place for improving economic activity.

If investors grow confident in a brightening outlook, they may begin to shift assets out of safe haven investments and into the value stocks that appear primed to benefit. As I noted earlier, the Wall Street consensus sees 15.9% EPS growth for the companies in which we are invested as compared to 7.3% for the S&P 500. If those expectations become reality, then our portfolio, at just 11x earnings, seems poised to close at least some of the value gap with the S&P 500’s current forward P/E of 18x. If our stocks were to converge on their 2007-2016 median P/E ratios, we could see 30-40% appreciation on top of a double-digit contribution from earnings growth and dividend yield.

The lagging phase of the value cycle that we’ve lived through over the last three years feels very similar to the one I witnessed as a new portfolio manager in 1997-1999. There are striking parallels in valuation spreads and in investor attitudes towards value investing. I don’t know if 2020 will see a value renaissance on par with what began in early 2000, but the ingredients are all there. I appreciate your patience and support in recent years as our portfolio has become what we believe is an ever more compressed spring primed for a monumental snapback.

Best wishes for what will surely be an interesting year!

Sincerely,

J. Dale Harvey

Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.