Dear Partners,

I have to start by saying that I have not been this frustrated in twenty years. In 2018, a negative turn in investor sentiment swamped the strong underlying business fundamentals of many of our portfolio investments. We have conviction in the companies we own, so it’s been hard to watch them get marked down to what we believe are absurdly low valuations given their outlooks. That said, the market-wide disconnect between prices and fundamentals has created wonderful buying opportunities. I used the selloff to add to my already substantial investments in the funds we manage. With this letter, I’d like to tell you why we think this is not the first chapter of a debilitating bear market decline. I’ve called on some well-known characters to help set the stage while hopefully infusing a little levity into an otherwise humorless fourth quarter.

—–

On a beautiful autumn morning, an acorn fell on Chicken Little’s head as he walked through the woods. “The sky is falling! I must go warn Henny Penny! But first I’ll call my bank and buy some Treasury bonds for protection – that’s the only safe place to hide.” And off he went to find Henny Penny.

When Chicken Little found Henny Penny he repeated, “The sky is falling! The sky is falling!” She replied, “Oh dear, this couldn’t come at a worse time! Someone is buying Treasury bonds (pushing down yields) at the same time the reckless Federal Reserve is raising rates. The yield curve is flattening; if it inverts, there will surely be a recession! We must go tell Ducky Lucky! But first I need to call my broker – with the yield curve flattening, the only safe thing to do is to sell all my bank stocks and to buy utility stocks.” And off they went to find Ducky Lucky.

When Chicken Little and Henny Penny found Ducky Lucky, they exclaimed, “The yield curve is flattening – it might soon invert!” Ducky Lucky replied, “Oh dear, this couldn’t come at a worse time! The unpredictable President has started a trade war with China. He’s even had the CFO of Huawei arrested in Canada, imposed tariffs and threatened many more. If he follows through, U.S. GDP could be 1% lower than forecast next year. We must go tell Honey Bunny! But first I need to tell my financial advisor to liquidate my oil and industrial investments and to put the proceeds into drug stocks – that’s a sure way to protect myself.” And off the threesome went to find Honey Bunny.

When they found Honey Bunny, she was worriedly reading the Financial Times. The Chicken Little posse cried out, “Bank stocks are falling while utility stocks climb! Oil prices are crashing and drug stocks are soaring!” She replied, “Oh dear, this couldn’t come at a worse time! Chinese growth is slowing, the UK is coming unglued over their divorce from the EU, and there is rioting in France! We must go warn everyone. But first I’ve got to sell those value stocks I own. I know they’ve done great in the long run, but they’ve been horrible in recent years. I give up!” And off they went.

Foxy Loxy was hungrily searching Open Table for a dinner reservation when the animated quartet came running into town, shrieking about calamity. He suggested they come to his house for dinner to discuss the dreadful turn of events. But just then, Honey Bunny had a better idea. “Let’s stop by Poplar Forest first; I’d love to hear what they think of all this.” And this is what we told them:

Bull Markets Die from Excessive Optimism – They Don’t Worry Themselves to Death

The last year has been a confounding one for value investors who focus on investing from the bottom up. Business fundamentals have been good, but multiple contraction has more than erased the growth in earnings. The macroeconomic fears expressed by Chicken Little and his friends have led to a fundamental repricing of risk. Or to put it another way, a rise in the equity risk premium has swamped all other contributors to return, such as earnings growth or dividend yield. The equity risk premium can be thought of as the compensation investors demand for holding “risky” equities over “risk-free” Treasury bonds. When the environment is perceived to be riskier, investors want more return which is accomplished by driving down the price of economically exposed businesses like financial services, industrials and energy while driving up the prices of “defensive” businesses like utilities and consumer staples. While we hear what Chicken Little is saying, we disagree with his investment conclusion.

Investors know there will be small ups and downs in the stock market over time – that’s just the way it works. The real fear is a debilitating bear market like 2007-2009 when stocks fell 57% and then didn’t recover for more than five years. The bursting of the tech bubble was similar – down 49% with over six years required before losses were recouped.

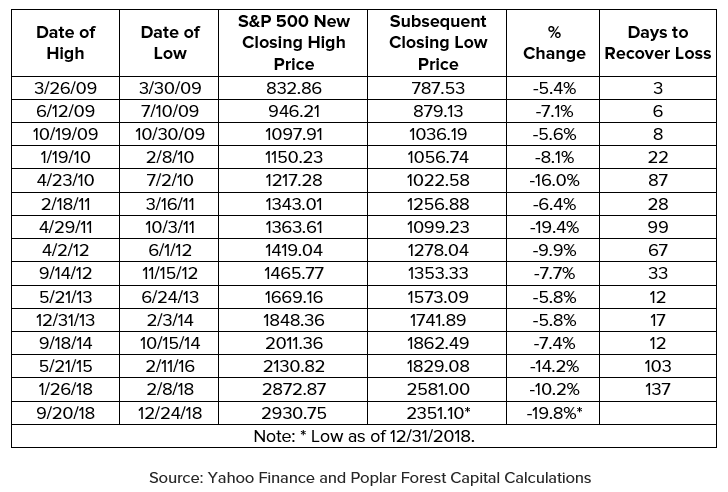

While the recent decline is of bear market magnitude, I think it is more akin to the three biggest corrections we’ve lived through since the market bottomed in 2009. In this case, year end tax loss harvesting and algorithmic trading seems to have exaggerated what would have been a more routine market drawdown. As in the biggest prior corrections of the last decade, I suspect losses will be recouped in a few months, not over several years.

- 2010 – 16% decline in S&P 500 – losses were recouped in 87 trading days

- 2011 – 19% decline in S&P 500 – losses were recouped in 99 trading days

- 2015 – 14% decline in S&P 500 – losses were recouped in 103 trading days

In my experience, debilitating bear markets occur when the Federal Reserve is trying to cool an overheated economy. That is NOT the case today. The economy isn’t overheated and the Fed isn’t trying to put out a fire. As the economy moved onto a sustainable path, the Fed set out to normalize monetary policy after a years-long experiment with free/easy money. Interest rates have moved back to more neutral levels this year and the Fed’s balance sheet is shrinking, thus creating dry powder for the next recession (That, Chicken Little, should be good news, not bad!).

History suggests the Fed has a long way to go before it risks creating a problem. With inflation around 2%, the Fed’s December increase to a 2.25-2.50% target pushed the “Real” (inflation adjusted) Fed Funds rate to 0.25-0.50%. The Fed isn’t trying to spray a fire extinguisher on an overheated economy, they are merely turning off the gas given that growth is self-sustaining. The dreaded fire extinguisher scenario would see a “Real” Fed Funds rate of 2.50% more than core inflation or a target of 4.25-4.50% given recent price readings. We’re far from fire extinguisher territory! And even if we get there, the economy would probably continue to grow, if history is any guide. For example, Real Rates hit 2.50% in December 1994 and the recession-driven bear market didn’t hit for another five years. The Real Rate hit 2.50% again in March 2006 and the stock market didn’t peak until 18 months later.

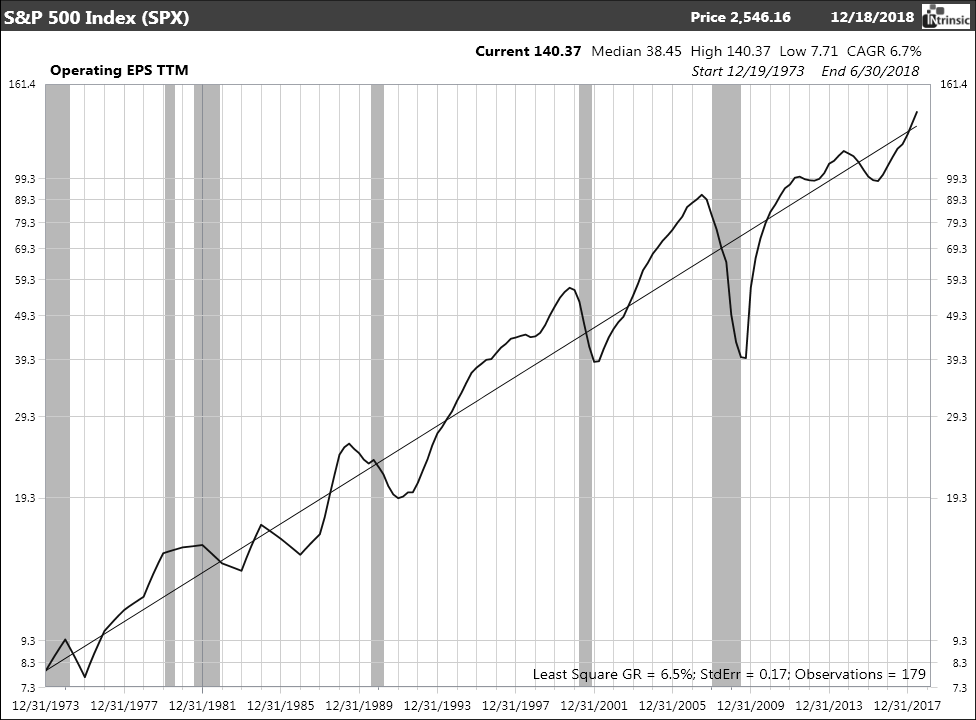

I think the Fed can be patient because we don’t see signs of excess, though we do have some worries about corporate credit and leveraged lending, particularly in the shadow banking system. That said, as market action this year demonstrates, so called “animal spirits” seem lacking – if anything, the animals seem dispirited and risk averse. Perhaps the fear is that stocks have simply appreciated too much in the period after the Trump administration started on a path of lower regulation and reduced taxes. As the economy improved, trailing earnings for the S&P 500 increased from below 45-year trend levels to 8-10% above. By comparison, earnings were 30-40% above trend in 2006-2007 and 20-25% above trend in 1998-1999.

While the risk of a recession-driven debilitating bear market seems low, investors are worried that something will go wrong. As a result of those worries, they are demanding more compensation for owning risky assets while being willing to accept more muted returns for investments they deem safe. For now, we’re living in a “Risk Off” world.

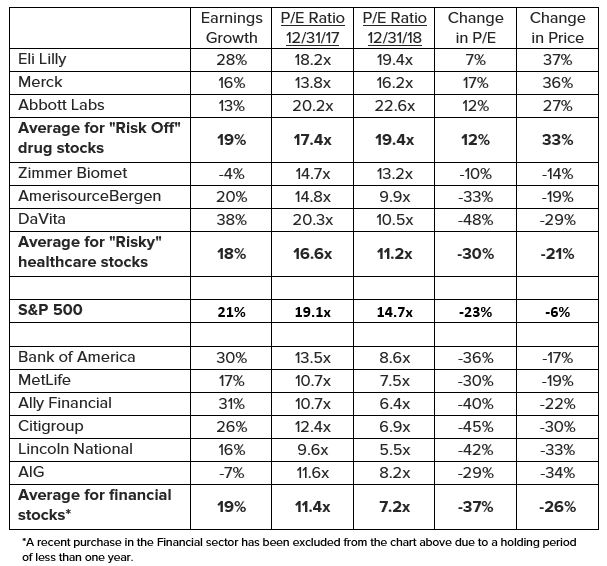

It has been 20 years since I remember seeing such disparity between loved and unloved stocks. In the late 1990s, it wasn’t “Risk Off” versus “Risk On,” it was “New Economy” versus “Old Economy.” In that environment, companies deemed capable of delivering strong growth were awarded ever higher valuations while shunned companies saw their P/E ratios contract. Today, “Defensive Growth” (e.g. pharmaceutical companies) is in favor while value (e.g. banks and oil stocks) suffers declining valuations due to a perception that they carry unacceptably above average risk.

On balance, the repricing of perceived risk had a detrimental effect on our results this year. You can see it on an inter- and intra-sectoral basis. Healthcare and financial services are our two largest sector exposures and earnings growth has been similar for both groups. However, P/E ratios expanded for the big, “safe” drug companies while declining for other businesses that investors deem “risky.” This suggests worries that the future will look far worse than the past. In essence, Chicken Little believes the outlook is weak and that EPS estimates are too high meaning value stocks aren’t as cheap as they appear.

A similar pattern of valuation contraction can be seen in the energy, materials, industrial and consumer cyclical sectors. Roughly two-thirds of the companies we owned this year saw their P/E ratios contract by 30% or more from levels that we thought were attractive. Our cheap stocks got cheaper. Our disappointing results haven’t been driven by poor business fundamentals, but by a re-pricing of perceived risk. We think this re-pricing has gone too far – and that it will eventually be reversed.

Markets Climb Walls of Worry

It has been said that markets climb walls of worry. If that’s the case, then there is a big wall for this market to climb. Investors’ biggest fears appear to be interest rates, trade and slowing global growth, but the worry list might also include:

- Oil prices (WTI) – down more than 40% since early October.

- Weakness in the automotive and housing sectors.

- A polarized electorate and divided Congress with potential for legislative dysfunction.

- Government shutdown due to presidential demands for border wall funding.

- The Mueller probe.

- Fading tax cut benefits that will likely be a headwind to economic growth in 2019.

- A tight labor market putting pressure on wages, and, in turn, corporate profits.

- Leveraged loans – are they a ticking time bomb?

- Falling liquidity as the Fed shrinks its balance sheet and as the U.S. Treasury increases borrowing to support an expanding budget deficit.

But Not all the News is Negative

- The manufacturing side of the economy remains robust.

- Consumer confidence remains high.

- Holiday spending was strong.

- Credit quality is outstanding.

- Unemployment is low.

- Job openings exceed job seekers.

- Inflation remains contained.

- Wages are growing faster than inflation – good news for consumers.

- Gasoline prices are down – also good news for consumers.

The latest reading put core inflation (ex-food and energy) at just 2.2% on a year/year basis. As long as inflation remains in the Fed’s +/- 2% range, they don’t need to douse the economy’s fire.

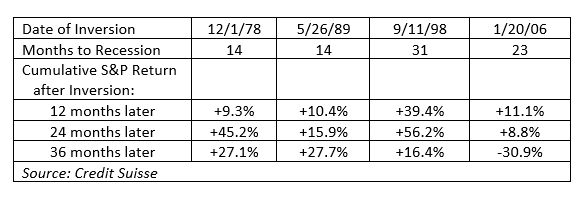

The yield curve, as measured by the difference between 10-year rates and 3-month T-bills, has flattened considerably (to 0.24% as of 12/31/18), but the curve hasn’t inverted (meaning short rates aren’t higher than long rates). Depending on the course of action pursued by the Fed and the reaction of markets to those actions, inversion could be months or even years away. And once the curve inverts, investors typically have ample time to react and, thus, good reason to be patient:

Of course, this time could be different. And there are certainly risks to which we need to be attentive. But the investment backdrop seems balanced, not cataclysmic. The companies we talk to aren’t seeing signs of impending recession and the measures we watch suggest we have ample time to prepare for the next recessionary-driven bear market.

Earnings seem likely to grow 5-10% in 2019 – admittedly less than the 20-25% tally we’ll likely see when the final numbers come in for 2018 – but at least in line with the historic average of 6-7% enjoyed by companies in the S&P 500 index over the last 45 years.

Valuations are also reasonable – certainly not low, but not challengingly high either. Compared to expected earnings of $170 in 2019, the 2507 closing price of the S&P 500 on 12/31/18 equated to a P/E ratio of just 14.7x earnings. In late 1999, stocks were valued at over 30x expected earnings – and those earnings were already 25% above trend. In late 2006, a year before trouble started, stocks also didn’t look expensive, but the multiple was deceptively low because earnings were 30% above normal.

Within the market, the re-pricing of risk by the Chicken Little crowd has created real opportunities. Just as the late ‘90s battle between “New Economy” and “Old Economy” stocks occurred on the doorstep of a seven-year run for value investing, the skewed performance of “Risk Off” versus “Risk On” seems to be setting up another huge opportunity for those of us who like cheap stocks. The analyst team at Poplar Forest has a rich set of opportunities to investigate. There simply isn’t room in the portfolio for all the good ideas we see in the research pipeline. We will continue to be very selective.

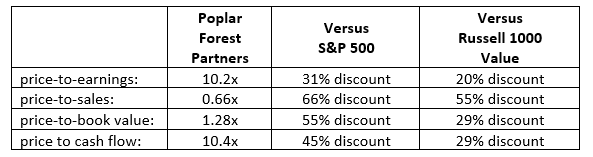

We believe our portfolios are particularly compelling on a long-term basis given expected growth and the prices we are paying for individual stocks. While we tend to be more optimistic about the companies we own, the consensus opinion is that these companies could generate long-term earnings growth of more than 11% a year. Even if the more conservative consensus is right, we should enjoy 11% earnings growth plus a ~3.0% dividend yield. Despite these seemingly attractive components to total return, the Poplar Forest Partners portfolio trades at a huge discount to the market:

In Conclusion

I’m not perpetually bullish. In the late 1990s, I built cash positions of 20% or more as I thought the market backdrop looked excessively risky. Managing both risk and reward is key to long-term investment success and we will stay on the lookout for signs of excessive optimism and yield curve inversion. We would expect to take a defensive posture if conditions warrant, but we don’t see cause for concern at the moment. We entered 2019 fully invested (roughly 1% cash.) We love the companies we own and we believe their stock prices are overly discounted by the market.

From a results perspective, this was the most maddening year I’ve had since 1998-1999. Despite fundamentals that were largely consistent with our expectations, valuations collapsed in a way we simply didn’t expect. Buying good companies when their stocks are on sale has proved a market-beating strategy over the long-term, but sometimes good deals get even better. That’s our take on 2018.

We don’t know how long Chicken Little will control the market narrative, but when calmer voices emerge, we could be in for tremendous gains. My best advice for the New Year is to head the other way when Chicken Little, Henny Penny and Ducky Lucky come running your way with proclamations that the sky is falling!

Sincerely,

J. Dale Harvey

Appendix – Market Corrections

Standardized Performance and Top Ten Holdings: Partners Fund, Cornerstone Fund

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 877-522-8860.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Holdings and allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Index performance is not indicative of a fund’s performance. Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.